EPF Monthly Housing Loan Instalment Withdrawal

EPF introduces ''monthly housing loan instalment'' withdrawal

Everyone has commitments or obligations to pay monthly housing loan instalments.

Various expenses need to be paid including car and house payments, children''s daily expenses, food, clothing and many more.

All these costs are increasing day by day.

Therefore, EPF has introduced the Monthly Housing Loan Instalment Withdrawal to reduce this burden.

Applicants can make withdrawals from Account 2 to help pay monthly instalments for a minimum of six months or until your financial difficulties are resolved.

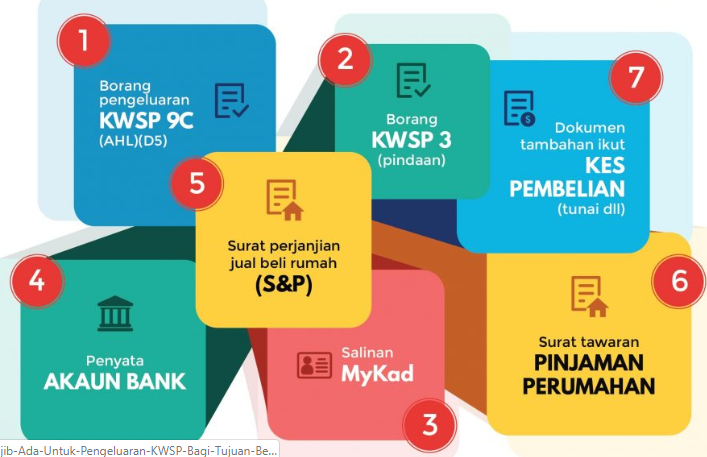

Requirements

Citizens and Non-Citizens

Below 55 years of age

A minimum of RM600 in Account 2

Purchasing/building a residential property*

Still has outstanding housing loan balance with a lender recognised by EPF**

Monthly instalments have commenced

Terms and Conditions

- Withdrawal is limited to one property per member. Subsequent withdrawals are only for the same property.

- If the property is refinanced, the loan balance is calculated based on the original loan payment from the first lender OR the current loan balance, whichever is lower. If more than one lender is involved, the redemption letter will be compared with the current balance to determine the eligible withdrawal amount. You are not eligible to apply if the original loan has been fully settled.

- You may make withdrawals to reduce monthly instalments and the Loan Balance Settlement Withdrawal simultaneously.

- EPF reserves the right to cancel the monthly payment withdrawal if the loan has been settled, the property has been sold/auctioned/ownership transferred, or if you are found guilty of fraud by submitting false information/documents.

- Housing loans in arrears with NPL status are allowed to apply for this withdrawal, provided that the monthly payments will be made directly to the housing loan account.

- The instalment period must not exceed the age of 55 years.

- You may make a withdrawal within 30 days before the instalment start date. However, the withdrawal payment will only commence after the actual instalment date takes effect.

- For subsequent withdrawals, you may apply as early as 30 days before the previous monthly instalment payment date ends.

- The withdrawal amount from Account 2 will be segregated into a special account for monthly instalment payments and will be paid dividends credited to Account 2 as soon as dividends are declared the following year.

- The maximum monthly payment period must not exceed the remaining housing loan tenure.

- If at the time of application there is an existing monthly housing loan instalment withdrawal from another borrower still in effect, the member is only eligible to withdraw the difference between the other borrower''s withdrawal amount.

Enhance Your Investment Knowledge

Successful investing begins with solid knowledge.

Investment Basics:

Download our free ebook for a comprehensive guide.

Open a CDS Account:

Ready to start? Open a CDS account now.

Frequently Asked Questions (FAQ)

What is the EPF monthly housing loan instalment scheme?

This scheme allows EPF members to withdraw funds from Account 2 to automatically pay monthly housing loan instalments, reducing the monthly financial burden.

Who is eligible to apply for EPF withdrawal for housing instalments?

EPF members who have an active housing loan and sufficient balance in Account 2 are eligible to apply. The instalment period must not exceed the age of 55 years.

Can the EPF withdrawal be used for housing loans in arrears?

Yes, housing loans in arrears with NPL status are allowed to apply for this withdrawal, provided that payments will be made directly to the housing loan account.

What are the advantages of using EPF to pay housing instalments?

Key advantages include reducing monthly cash flow burden, the segregated funds still earning EPF dividends, and enabling you to utilise your income for other investments.

With wise financial management including optimising EPF withdrawals, you can allocate surplus funds for stock investments that have the potential to deliver higher returns.

Open a CDS account today to start investing in stocks on Bursa Malaysia and build your long-term investment portfolio.

Download the free stock basics ebook to understand the fundamentals of stock investing and how to start investing wisely.

Further reading: