LPPSA Housing Loan: Pros, Cons & Smart Strategies for Civil Servants

What Is LPPSA?

LPPSA, or Lembaga Pembiayaan Perumahan Sektor Awam (Public Sector Home Financing Board), is a statutory body established on 1 March 2016 under the Public Sector Home Financing Board Act 2015 (Act 767). It replaced the Housing Loans Division (BPP) previously managed by the Treasury under the Ministry of Finance.

LPPSA's primary mission is to provide efficient, transparent, and affordable housing financing to civil servants across Malaysia. Unlike commercial bank loans, LPPSA operates not for profit - but for the welfare of government employees.

Since its establishment, LPPSA has managed over RM200 billion in housing financing portfolio, making it one of the largest housing financing institutions in the country.

Who Is Eligible for LPPSA?

Not everyone can apply for LPPSA financing. It is exclusively available to those serving in the public sector. Here is the full list of eligible applicants:

Eligible Categories

- Federal civil servants - permanent officers who have been confirmed in their position

- State civil servants - subject to respective state government approval

- Royal Malaysia Police (PDRM) members

- Malaysian Armed Forces (ATM) members

- Administration members - including Prime Minister, Ministers, Deputy Ministers

- Judges - High Court judges and above

- Members of Parliament and State Assembly members

- Speaker of the House of Representatives and Senate President

- Statutory body and local authority (PBT) employees

Basic Eligibility Requirements

In addition to falling under the categories above, applicants must also meet the following criteria:

- Malaysian citizen

- Permanent officer who has been confirmed in position

- Minimum 1 year of service

- Not bankrupt or facing serious financial issues

- Not under disciplinary action for dismissal

- Net salary minimum 20% of gross income after all deductions

Types of Financing Offered by LPPSA

LPPSA is not just for buying completed homes. It offers various types of flexible financing to meet different civil servant needs:

1. Purchase of Completed Homes

For buying homes that are already built - whether terrace houses, apartments, condominiums, or bungalows. This is the most popular application type.

2. Purchase of Homes Under Construction

For homes still being built by developers. Fund disbursement is done in stages according to construction progress.

3. Building a Home on Own Land

Civil servants who already own land can apply for financing to build a house. This includes construction materials and contractor costs.

4. Land Purchase and Home Construction

A combined financing for both land purchase and home construction in one package.

5. Home Renovation and Repairs

For renovating existing homes - adding rooms, replacing roofing, kitchen renovation, and more.

6. Settlement of Existing Financing (Take Over)

If you have a housing loan with a bank, LPPSA can "take over" that debt. This allows you to enjoy the 4% fixed interest rate, which is lower than most bank rates.

LPPSA Loan Eligibility Calculation

This is the section most people want to know about - how much can you actually borrow? LPPSA uses a different formula from commercial banks.

LPPSA DSR Calculation Formula

According to LPPSA MyFinancing's official page, eligibility is calculated based on two key criteria:

For first financing:

- Monthly instalment must not exceed 60% of basic salary and fixed allowances

- Total debt must not exceed 80% of net income

For second financing:

- Monthly instalment must not exceed 50% of basic salary and fixed allowances

- Total debt must not exceed 80% of net income

Fixed Allowances Included

Not all allowances are taken into account. Only two fixed allowances are included in the calculation:

- Fixed Housing Allowance (ITP)

- Fixed Civil Service Allowance (ITKA)

Sample Eligibility Calculation

Consider a teacher at Grade DG41 with the following details:

- Basic salary: RM3,500

- ITP: RM300

- ITKA: RM190

- Total salary + fixed allowances: RM3,990

Calculation for first financing:

- 60% x RM3,990 = RM2,394 (maximum monthly instalment)

- Minus existing commitments (e.g.: car RM800, PTPTN RM200) = RM1,000

- Balance for housing instalment: RM1,394 per month

With a fixed interest rate of 4% and a 35-year tenure, a monthly instalment of RM1,394 allows financing of approximately RM300,000 - RM320,000.

Approved Financing Amount

According to LPPSA FAQ, the approved financing amount is based on the lowest value among:

- Property price

- JPPH valuation (Department of Valuation and Property Services)

- Amount applied for

- Applicant's maximum eligibility

LPPSA vs Bank Calculation Advantage

One important thing many people don't know - mandatory deductions such as EPF (KWSP), SOCSO, and income tax are NOT counted as commitments in LPPSA's eligibility calculation. This means your eligibility is usually higher compared to bank calculations.

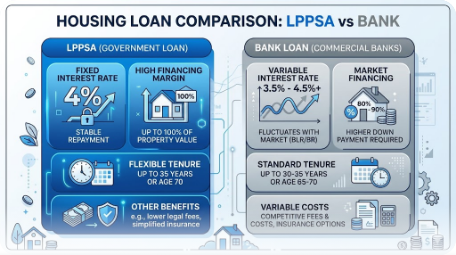

6 Key Advantages of LPPSA Loans

1. 100% Financing Margin

LPPSA offers financing up to 100% of the property price. You don't need to prepare a 10% deposit like regular bank loans. In fact, ancillary costs such as insurance/takaful (MRTT/MRTA) and stamp duty can also be included in the loan amount.

2. Fixed Interest Rate of 4% Per Year

This is LPPSA's biggest advantage. The interest rate remains at 4% throughout the loan tenure - regardless of how many times Bank Negara raises or lowers the OPR. Compared to bank loans that typically start at 3.5-4.5% but can rise to 5-6% when OPR increases, LPPSA provides invaluable monthly instalment stability.

3. Repayment Period Up to 35 Years

Civil servants can choose a repayment period between 5 to 35 years, or until mandatory retirement age (whichever is earlier). A longer period means lower monthly instalments, providing more financial breathing room.

4. No Early Settlement Penalty

Want to settle your loan early? No problem. LPPSA does not impose any penalty for additional payments or early settlement. Banks usually charge a 2-3% penalty if you settle the loan within the lock-in period (typically the first 3-5 years).

5. Second Financing Allowed

LPPSA allows a second financing for purchasing another property, home renovation, or refinancing. Starting Q4 2026, second financing requirements will be relaxed - applicants will not need to fully settle the first financing before applying for the second.

6. Online Application Process

Through the LPPSA MyFinancing portal, applications can be made entirely online. This saves time and makes it easy to track application status.

5 Disadvantages of LPPSA Loans You Should Know

1. Slower Approval Process

Compared to banks that typically approve loans within 1-2 weeks, LPPSA can take 1-3 months due to government bureaucracy. Fund disbursement is also slower, which can be problematic if the seller needs money urgently.

2. 4% Rate Isn't Always Cheaper

While the fixed 4% rate looks attractive, it can actually be more expensive in certain scenarios. When OPR is low, banks offer rates as low as 3.0-3.5%. In such conditions, bank loans are actually more cost-effective. However, when OPR is high (like in 2023-2024 when OPR reached 3.0%), LPPSA's fixed 4% rate becomes very competitive.

3. Maximum Two Times Lifetime Limit

LPPSA only allows a maximum of two financings throughout your service career. Banks don't have such a limit - as long as your DSR allows it, you can apply for housing loans multiple times.

4. Less Flexible

LPPSA doesn't offer various packages like banks. There's no floating rate option, no cash-back, no flexi loan, and no overdraft facility. Commercial banks offer various attractive packages that give borrowers more flexibility.

5. Only for Civil Servants

This is obvious - if you're not a civil servant, you can't apply. And if you leave public service before the loan is settled, you need to settle the outstanding balance or apply for a take over to a bank.

LPPSA vs Bank: Detailed Comparison

To make comparison easier, here's a summary table between LPPSA and bank housing loans:

| Aspect | LPPSA | Commercial Bank |

|---|---|---|

| Interest rate | Fixed 4% | Starting 3.0-4.5% (varies with OPR) |

| Financing margin | Up to 100% + ancillary costs | 90% (first home), 70% (third home) |

| Maximum tenure | 35 years / retirement age | 35 years / age 70 |

| Early settlement penalty | None | 2-3% during lock-in period |

| Approval process | 1-3 months | 1-2 weeks |

| Eligibility | Civil servants only | All citizens |

| Financing limit | 2 times lifetime | No limit |

| Additional packages | None | Flexi loan, cash-back, overdraft |

In summary, if you're a civil servant planning to buy your first home - LPPSA is almost always the better choice due to 100% margin, no deposit, and interest rate stability.

5 Smart Strategies for Using LPPSA Financing

Strategy 1: Leverage 100% Margin for Your First Home

Many young civil servants struggle to save a 10% deposit for their first home. With LPPSA, you can buy a home with zero deposit. This strategy allows you to enter the property market earlier and start building equity now.

Tip: Use the money that would have been your deposit for an emergency fund or other investments.

Strategy 2: Take Over Bank Loan to LPPSA

If you're a civil servant with an existing bank housing loan, consider taking it over to LPPSA. This is especially beneficial if your bank rate exceeds 4%. According to Asco Law, refinancing to LPPSA can save tens of thousands of ringgit in interest over the long term.

Savings example: Outstanding loan of RM300,000 at bank rate 4.5% vs LPPSA 4.0% - this 0.5% difference can save RM30,000-50,000 over the remaining loan tenure.

Strategy 3: Plan Your Second Financing Carefully

Since LPPSA only allows two financings in a lifetime, plan wisely. Don't "waste" your first financing on a small house if you can wait a little longer for a more suitable home.

Tip: Use your first financing for a family home (long-term) and save the second financing for property investment or an upgrade later on.

Strategy 4: Make Consistent Extra Payments

Since there's no early settlement penalty, take the opportunity to make additional payments whenever you have surplus money - annual bonuses, promotions, or EPF withdrawals. Every extra RM100 per month can shorten your loan tenure by years and save thousands in interest.

Strategy 5: Combine with Government Housing Schemes

Civil servants are also eligible for various government housing schemes like PR1MA, Rumah Mampu Milik, and Residensi Wilayah. Combine your LPPSA eligibility with these schemes to get lower house prices with full financing.

Latest LPPSA Developments in 2026

Several important developments that civil servants should know:

- Second financing requirements relaxed: Starting Q4 2026, applicants will not need to fully settle their first financing before applying for a second one. This opens opportunities for civil servants looking to invest in a second property.

- MyFinancing portal upgraded: The online application process has been streamlined with real-time tracking and digital documentation.

- Collaboration with developers: LPPSA is increasingly working with housing developers to expedite fund disbursement processes.

Frequently Asked Questions (FAQ) About LPPSA

How long does the LPPSA loan approval process take?

The approval process typically takes 1-3 months from the date the complete application is received. This includes document verification, JPPH valuation, and internal approval. Ensure all documents are complete to avoid delays.

Can LPPSA financing be used for property in any state?

Yes, LPPSA financing can be used to purchase property in any state within Malaysia. There are no location restrictions as long as the property meets the stipulated requirements.

What happens if I leave government service before the loan is settled?

If you leave public service, you will need to settle the outstanding loan in full or apply for a take over to a commercial bank. LPPSA will provide a specific period for settlement.

Can husband and wife apply for LPPSA together?

Yes, couples who are both civil servants can make a joint application. This increases financing eligibility as both parties' combined income is taken into account.

Are contract civil servants eligible for LPPSA?

No. LPPSA is only open to civil servants who have been permanently appointed and confirmed in their position. Contract, part-time, or temporary workers are not eligible.

How many times can I apply for LPPSA financing?

You can apply for a maximum of two LPPSA financings throughout your service career. After two times, you will need to use bank financing for subsequent properties.

Can I check LPPSA eligibility online?

Yes, you can use the eligibility calculator on the official LPPSA MyFinancing portal to estimate your financing eligibility based on your salary and current commitments.

Does LPPSA offer Islamic financing?

Yes, LPPSA offers both conventional and Islamic financing schemes. Applicants can choose the scheme that best suits their needs.

Conclusion

LPPSA is an incredibly valuable benefit for civil servants planning to own a home. With 100% financing margin, a fixed 4% interest rate, and no early settlement penalty, it offers advantages that are hard to match by any commercial bank. However, also understand its drawbacks - slower process, two-time lifetime limit, and less flexibility - so you can make the right decision.

Owning a home is a major step in financial planning. Besides property, investing in the stock market can also help you build long-term wealth.

Open a CDS trading account to start investing on Bursa Malaysia as well as international stocks including US and Hong Kong markets - diversify your portfolio beyond property.

Download our free stock market basics ebook to learn the fundamentals of stock investing from scratch.