FCPO: Crude Palm Oil Futures Trading in Malaysia Explained

The development of the global edible oil market over the past four decades cannot be separated from the rise of palm oil as the most widely used and traded vegetable oil in the world. At the heart of this development lies a financial instrument that serves as the backbone of the industry - Crude Palm Oil Futures (FCPO).

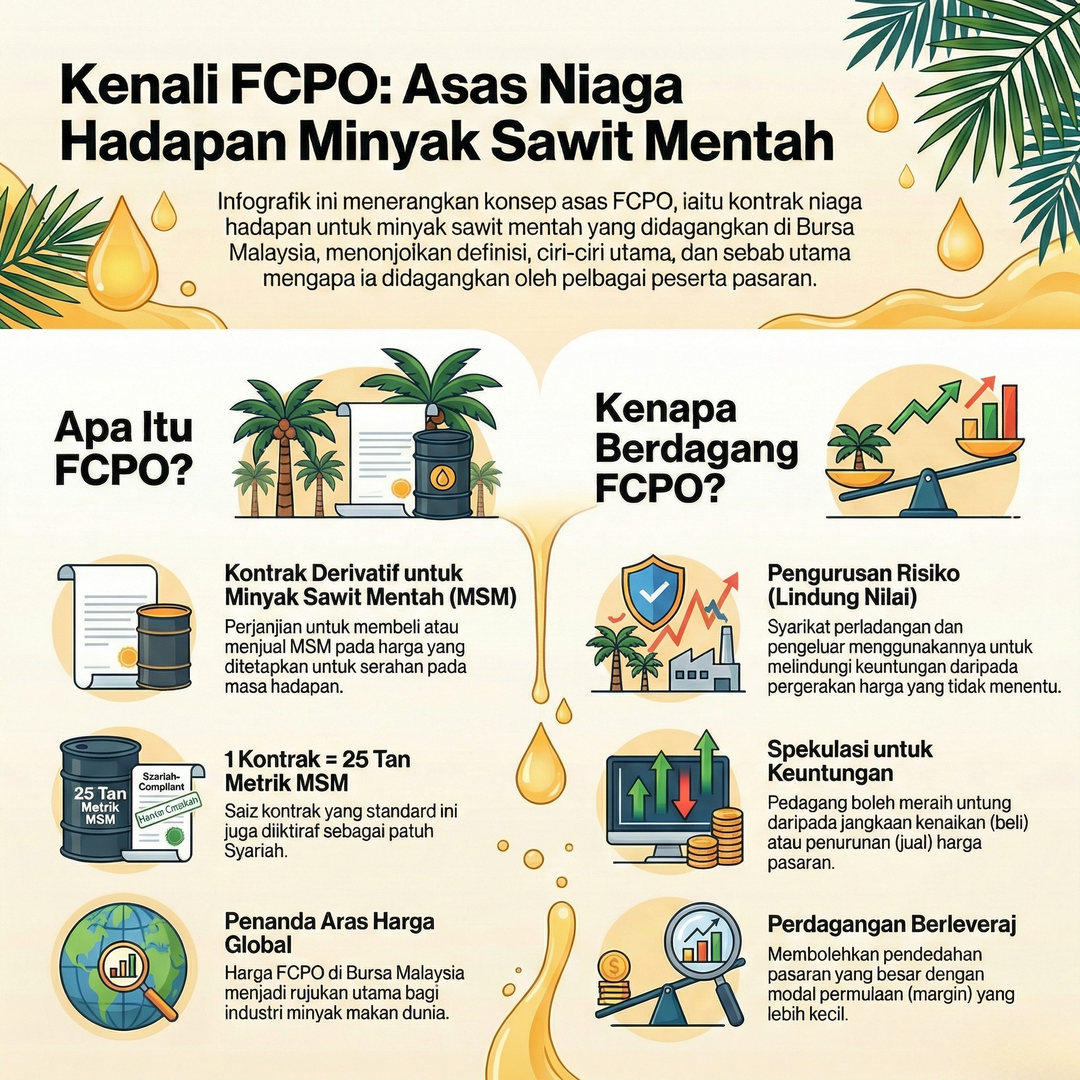

FCPO is a derivatives contract traded in Malaysian Ringgit (MYR) on Bursa Malaysia Derivatives (BMD). Since its official launch in October 1980, FCPO has evolved from a mere local hedging tool into a global price benchmark for the palm oil industry, facilitating price discovery and risk management functions for a global network of stakeholders.[1][2][3]

The importance of this contract structure is highlighted by Malaysia's role as the world's second-largest producer and exporter of palm oil, contributing significantly to the global supply chain.[4]

In 2024, this market demonstrated its resilience and depth, with FCPO contributing more than 83% of total trading volume on the exchange, representing a record high of 18.95 million contracts.[5] This dominance illustrates the contract's liquidity and its critical function within the broader agricultural and energy complex.

Evolution of the Derivatives Market in Southeast Asia

The emergence of FCPO as a global benchmark was not an isolated event, but the result of strategic initiatives to centralise price discovery in the region that physically produces the commodity.

Before the 1980s, palm oil trading was largely fragmented, characterised by over-the-counter (OTC) transactions lacking transparency and standardised quality assurance. The establishment of the Kuala Lumpur Commodities Exchange (KLCE), which later became Bursa Malaysia Derivatives, provided a regulated platform for standardised trading.[1][3]

The transition from the "open outcry" trading system to a fully electronic platform in 2001 marked a pivotal moment, enhancing market efficiency and attracting a broader spectrum of international participants.[6]

The integration of BMD products with the CME Globex electronic trading platform further expanded access, enabling institutional fund managers, commodity trading advisors (CTAs), and professional traders from every time zone to participate in the Malaysian market.[1][2][7] This global interconnectedness ensures that FCPO prices reflect collective global expectations of supply and demand, not merely local market conditions.[5][8]

As the market evolved into the 21st century, the focus shifted towards financial protection and sustainability, culminating in the 2021 mandate for Malaysian Sustainable Palm Oil (MSPO) certification for all physical deliveries, thereby aligning the financial benchmark with global Environmental, Social, and Governance (ESG) standards.[2][5]

Mechanics of the FCPO Contract Structure

The efficiency of any futures market depends on the absolute standardisation of its underlying contract. The FCPO contract is meticulously defined to ensure that every lot traded is identical in terms of quality, quantity, and delivery terms, thereby eliminating the need for physical inspection before a trade is executed.[1][6][9]

It is this standardisation that enables high-speed electronic trading and ensures that price is the sole variable in the negotiation process.

Core Contract Specifications

Contract Feature | Specification Details |

|---|---|

Contract Code | FCPO [10][11][14] |

Underlying Asset | Crude Palm Oil (CPO) [1][10][12] |

Contract Unit | 25 Metric Tonnes (MT) [1][2][10][11] |

Price Quotation | Malaysian Ringgit (MYR) per Metric Tonne [2][10][14] |

Minimum Tick Size | RM 1.00 per MT (Value: RM 25.00) [4][6][14][15] |

Contract Months | Current month + 11 consecutive months; then alternate months up to 36 months forward [2][10][11] |

Trading Hours (Morning) | 10:30 AM to 12:30 PM (MYT) [2][10][11][14] |

Trading Hours (Afternoon) | 2:30 PM to 6:00 PM (MYT) [2][10][11][14] |

After-Hours Trading (T+1) | 9:00 PM to 11:30 PM (Monday-Thursday) [2][10][14][16] |

Settlement Type | Physical Delivery at approved PTIs [1][10][17][18] |

Understanding the "Tick" Concept

The concept of a "tick" is fundamental to profit and loss (P&L) calculation in FCPO trading. Since one tick represents RM 1.00 per metric tonne and one contract covers 25 metric tonnes, a one-point movement in the market price results in a RM 25.00 change in position value.[6][12][15]

Example profit calculation:

Enter long position at: RM 4,200

Price rises to: RM 4,250

Profit = (4,250 - 4,200) x 25 MT x 1 Contract = RM 1,250

This linear relationship enables precise risk management and the application of technical analysis for setting profit targets and stop-loss levels.[3][15]

Trading Sessions and Global Integration

The trading schedule for FCPO is designed to maximise overlap with other major global financial centres and commodity markets. The main sessions - morning and afternoon - capture peak activity during the opening of Asian and European markets.[10][11]

However, the most significant development in the operational framework is the introduction and extension of the After-Hours (T+1) trading session. This session, running from 9:00 PM to 11:30 PM, enables Malaysian market participants to react to price-moving events in the United States, such as the release of USDA (United States Department of Agriculture) reports or changes in CBOT (Chicago Board of Trade) soybean oil futures.[2][10][16]

All trades executed during the T+1 session are cleared and settled as part of the following business day's activity.[16] This extension has drastically reduced "gap risk" - the risk of the market opening significantly higher or lower than the previous day's close due to overnight news - by providing a continuous window for price adjustment.[16]

Biological and Agronomic Determinants of Supply

Unlike industrial commodities, the supply of crude palm oil is governed by complex biological cycles and environmental conditions. The oil palm tree (Elaeis guineensis) is a perennial crop that begins fruiting approximately 30 months after planting and can remain productive for 25 to 30 years.[19][20] However, its yield is highly sensitive to external factors, creating seasonal and cyclical patterns that traders must navigate.

Seasonality and Production Cycles

Palm oil production in Malaysia follows well-documented seasonal trends. Analysis of historical data reveals four key components: trend, cycle, seasonality, and irregular fluctuations.[19]

The "biological rest phase" is a critical phenomenon whereby, following a period of exceptionally high yields, trees experience a physiological slowdown to replenish nutrients.[21][22]

Peak Season (July to October):

During this period, favourable rainfall and peak sunlight hours often produce maximum fruit maturity

In October 2025, Malaysia witnessed production surge by 11% to reach the highest monthly output in a decade, largely driven by recovery in Sabah and Sarawak[21]

High production often leads to stock accumulation, which can exert downward pressure on FCPO prices unless offset by strong export demand[21][23]

Low Season (December to March):

Yields generally decline during these months

This period coincides with the Northeast Monsoon in Malaysia, which often brings heavy rainfall and flooding to major plantation areas in Johor, Pahang, and East Malaysia[21][24]

Flooding not only hinders biological fruit development but also creates significant logistical obstacles, preventing workers from harvesting Fresh Fruit Bunches (FFB) and disrupting transportation of FFB to mills[21][25][26]

In January 2026, production is forecast to decline by 15% to 17%, a sharper-than-usual seasonal drop that supports a "structural floor" for prices around the RM 4,000 to RM 4,300 range.[24][25][27]

Meteorological Impact: Rainfall and Fertilisation

Oil palm yields correlate directly with rainfall patterns observed 12 to 24 months previously. While trees require consistent hydration (ideally 2,000mm to 2,500mm of well-distributed annual rainfall), excessive drought or severe dry spells - often associated with the El Nino weather phenomenon - can severely impair fruit development.[19][21]

Conversely, late monsoon arrivals can enable extended harvesting periods, as observed in late 2024 and early 2025, leading to sustained output levels exceeding historical averages.[21][22]

Furthermore, fertiliser application plays a critical role in determining future yields. When CPO prices are low, smallholders may reduce fertiliser usage to preserve cash flow, which in turn affects production 18 to 24 months later.[19][21] Traders monitor these agronomic variables closely through reports from the Malaysian Palm Oil Board (MPOB) to forecast long-term supply shifts.[15][22]

Macroeconomic Interactions and Global Correlations

Palm oil does not exist in isolation; it is part of the broader global "Vegetable Oil Complex" that is interconnected with energy markets and macroeconomic indicators.[28][29][30]

Substitutability and Soybean Oil Correlation

Soybean oil and palm oil are the two most widely produced edible oils in the world, together accounting for approximately 64% of global production.[30] Because both are largely interchangeable in the food processing industry, their prices exhibit a strong statistical correlation, typically between 70% and 85%.[28][31]

Historically, soybean oil has traded at a premium to palm oil (typically USD 100 to USD 250 per metric tonne) as it is perceived as a higher-quality product with better health attributes.[28][30] However, short-term supply disruptions can cause this spread to narrow or even reverse.

In late 2024 and early 2025, palm oil was observed trading at a rare premium to soybean oil, an anomaly driven by tight palm oil stocks and aggressive Indonesian biodiesel mandates.[21][31]

Traders use the price spread as a leading indicator for market direction:

Widening Spread: If soybean oil becomes too expensive relative to palm oil, major importers such as India and China will switch their purchases to palm oil, ultimately driving FCPO prices higher.[28][30]

Spread Reversal: When the spread reaches extreme levels (distribution tails), arbitrageurs and spread traders often take positions for a reversion to the historical mean.[28][31]

Energy Nexus: Crude Oil and Biodiesel

The relationship between crude oil and palm oil has strengthened significantly since the early 2000s due to the rise of the biofuel industry. When mineral crude oil prices increase, palm oil becomes more attractive as a feedstock for biodiesel, boosting industrial demand.[3][29][32]

The key policy driver in this space is Indonesia's biodiesel mandate. As the world's largest palm oil producer, Indonesia's decisions regarding B35, B45, or B50 (referring to the percentage of palm-oil-based biodiesel blended with petroleum diesel) are a "major swing factor" that determines the exportable surplus available for the global market.[21][25][27][31]

Higher mandates consume more CPO domestically, tightening global supply and acting as a bullish catalyst for FCPO prices.[21]

Currency Dynamics and the USD/MYR Relationship

Because palm oil is an export-oriented commodity priced in Malaysian Ringgit (MYR), the exchange rate with the US Dollar (USD) is a critical determinant of international competitiveness.[4][33]

Currency Movement | Impact on FCPO [27][33][34] |

|---|---|

Ringgit Weakens (USD/MYR rises) | Makes FCPO cheaper for international buyers; increases export demand and domestic prices |

Ringgit Strengthens (USD/MYR falls) | Makes FCPO more expensive for foreign importers; may dampen demand and domestic prices |

Quantitative research indicates that exchange rates and interest rates have a significant negative impact on FCPO prices in the long run.[33][34]

Specifically, an increase in interest rates (e.g. a 100 basis point hike) is associated with a decrease in FCPO prices (approximately 0.18%), as it raises the cost of carry for inventory holders and may divert capital from commodities towards fixed-income assets.[33]

Risk Management and Settlement Framework

Derivatives markets are inherently leveraged, necessitating robust financial safeguard systems to ensure market integrity. Every trade on Bursa Malaysia Derivatives is cleared by Bursa Malaysia Derivatives Clearing (BMDC), which acts as the Central Counterparty (CCP).[5][35]

By acting as an intermediary between every buyer and seller, the clearing house eliminates "counterparty risk" - the risk that one party defaults on their obligations.[5][36]

The SPAN Margining System

BMDC employs the Standard Portfolio Analysis of Risk (SPAN) system, a portfolio-based margining methodology developed by the Chicago Mercantile Exchange (CME). Unlike traditional systems that impose a fixed margin per contract, SPAN evaluates the total risk of a trader's entire portfolio, including futures and options.[5][35]

The SPAN system generates "risk arrays" that simulate how a portfolio would perform under 16 different market scenarios, ranging from extreme price increases to significant volatility changes.[35] Margin requirements are set based on the "worst case" loss scenario to ensure adequate collateral is always available.[35]

Margin Type | Purpose |

|---|---|

Initial Margin | Minimum deposit required to initiate a new trade [1][12][35][36] |

Maintenance Margin | Minimum level that the account balance must reach before a margin call is triggered |

Variation Margin | Daily cash adjustments based on the "mark-to-market" value of positions [1][36][37] |

Intraday Margin | Reduced margin offered by some brokers (e.g. 50%) for positions closed within the same day [36][38] |

As of January 2026, the standard outright margin for one FCPO contract has been revised to RM 6,000.[39][40]

For a trader holding a position at RM 4,200 (notional value RM 105,000), this represents a leverage ratio of approximately 17.5:1.[12][13]

Margin Offsets and Spread Credits

One of the key benefits of the SPAN system is the provision of "spread credits" for related positions. If a trader has a long position in one contract month and a short position in another, the risk largely offsets.

Consequently, the margin required for intra-commodity spreads is significantly lower - often only RM 600 to RM 1,800 depending on the proximity of months - compared to the RM 6,000 required for an "outright" directional bet.[35][38][39][41]

This capital efficiency makes spread trading a popular strategy for both speculators and hedgers.[13][28]

Physical Settlement, Quality Assurance, and Sustainability Mandate

Although only a small fraction of FCPO contracts (typically less than 5%) result in physical delivery, the possibility of delivery is what anchors futures prices to the real-world value of palm oil.[1][18][42] This convergence is fundamental to a functioning hedging market.

The Tender and Delivery Process

The physical delivery process is tightly regulated by the exchange's "Post-Trade" rules. When the "spot month" commences, the contract enters its delivery period, spanning from the 1st to the 20th of the month.[1][14][17][18]

Steps:

Notification: Sellers holding a short position must submit a "Tender Notice" to the clearing house by 12:00 noon on the day they wish to initiate delivery.[1][14][18]

Storage and Logistics: The oil must be stored in bulk and unbleached form at exchange-approved Port Tank Installations (PTIs). These installations are located at key ports including Port Klang, Penang/Butterworth, and Pasir Gudang (Johor).[1][17][18]

e-NSR System: Ownership of the oil is transferred digitally through the e-Negotiable Storage Receipt (e-NSR) system. Each e-NSR represents one lot of 25 metric tonnes.[1][14]

Payment and Title: The buyer (holder of the long position) must pay the full contract value (not just the margin) to receive the e-NSR. This transaction follows a T+2 cycle, where the seller receives payment two business days after the tender is processed.[1][43]

Quality Standards for Merchantable Oil

To ensure that the CPO delivered is of "good merchantable quality," the exchange mandates rigorous testing by approved surveyors. If the oil fails to meet these specifications, it cannot be used to settle an FCPO contract.[14][17][18]

Chemical/Physical Property | Accepted Range (Entry PTI) | Accepted Range (Exit PTI) |

|---|---|---|

Free Fatty Acid (as Palmitic) | Maximum 4.0% | Maximum 5.0% |

Moisture and Impurities | Maximum 0.25% | Maximum 0.25% |

DOBI (Deterioration of Bleachability Index) | Minimum 2.5 | Minimum 2.31 |

The difference between the "Entry PTI" and "Exit PTI" limits accounts for the natural deterioration of the oil during storage. For example, Free Fatty Acid (FFA) naturally increases over time as the oil oxidises.[14][17][18]

The MSPO Sustainability Mandate

In April 2021, Bursa Malaysia Derivatives became the first exchange globally to mandate sustainability certification for physically-delivered commodity futures contracts.[2][5]

This requires all CPO delivered under FCPO contracts to be sourced from mills that meet the Oil Palm Management Certification (OPMC) under the Malaysian Sustainable Palm Oil (MSPO) scheme.[2][5][8][11]

This initiative has repositioned FCPO not merely as a financial benchmark, but as a "green" benchmark, ensuring the global price of palm oil incorporates the costs of sustainable production practices.[5][8][11]

FEPO - East Malaysia Crude Palm Oil Futures

In October 2021, BMD launched the East Malaysia Crude Palm Oil Futures (FEPO) to address the specific needs of the industry in Sabah and Sarawak, which together contribute nearly half of Malaysia's palm oil production.[20][44][45][46]

Comparison of FCPO and FEPO

FEPO was designed to eliminate "basis risk" for East Malaysian producers, who previously had to hedge using FCPO (based on Peninsular Malaysia delivery points) despite having different local logistics and supply dynamics.[37][44]

Feature | FCPO | FEPO |

|---|---|---|

Delivery Ports | Port Klang, Pasir Gudang, Butterworth [17][37] | Lahad Datu, Sandakan, Bintulu [44][46] |

Trading Start Time | 10:30 AM (MYT) [10][37] | 9:00 AM (MYT) [37][44] |

Speculative Limit (Spot) | 1,500 Contracts [10][17][37] | 1,500 Contracts [37] |

Speculative Limit (Single Month) | 20,000 Contracts [10][17][37] | 10,000 Contracts [37] |

Global Alignment | European/US markets (via T+1) [2][16] | China market (DCE Olein) [44][46] |

The 9:00 AM start time for FEPO is specifically aligned with the opening of the Dalian Commodity Exchange (DCE) in China. This allows arbitrageurs to trade the price differential between China's RBD Palm Olein and East Malaysian CPO in real time, enhancing price discovery and attracting liquidity from Chinese commodity desks.[44][46]

Operational Landscape: Trading, Rollover, and Portfolio Management

Account Opening and Management

Trading derivatives in Malaysia is a tightly regulated activity. Individual and corporate investors must open a "Futures Trading Account" through licensed Trading Participants (brokers).[3][7][13][36]

Requirements:

Verification: Malaysian citizens are required to provide their Blue Identity Card and income documents (pay slips or bank statements). Foreign nationals must submit a valid passport and work permit.[47]

Regulation: Brokers are supervised by the Securities Commission Malaysia (SC) and the exchange to ensure compliance with the Capital Markets and Services Act (CMSA).[7][36][48][49]

Financial Stability: Industry practitioners emphasise that trading is high-risk and should only be undertaken by those with 6-12 months of emergency savings.[13]

Order Execution: Orders can be placed electronically via proprietary platforms such as Phillip Nova or KDF TradeActive, or by phone to a licensed Futures Broker Representative (FBR).[4][15][47]

Strategic Rollover Mechanics

Because futures contracts have a limited lifespan, long-term investors must "roll" their positions forward to maintain exposure.[42][50][51]

Rollover involves closing the expiring contract (e.g. selling back a long July position) and simultaneously opening a new position in the next active month (e.g. buying a long August position).[50][51][52]

Three important metrics for rollover:

Volume and Open Interest: Most traders roll over when the "back month" trading volume surpasses the "front month" - typically 5-7 days before the spot month commences.[50][53]

Spread Cost: The price difference between the two months. In a "Contango" market, rolling a long position incurs a cost. In a "Backwardation" market, rolling a long position captures a premium.[51][52]

Liquidity Migration: Waiting until the last trading day can lead to "slippage" - where the bid-ask spread widens as participants exit the expiring contract.[50][51][52]

Warning for retail investors:

Failure to roll or close a position before "First Notice Day" can trigger physical delivery assignment, requiring the trader to provide or accept 25 metric tonnes of oil - an expensive and logistically impossible task for most individuals.[42][51][52]

Quantitative Forecasting and Strategic Outlook 2026

As the market looks towards the 2026 production year, the convergence of technological advances and changing climate patterns is reshaping the forecasting landscape. Analysts are increasingly relying on hybrid ARIMA-GARCH and SVM (Support Vector Machine) models to capture the non-linear volatility of FCPO prices.[20]

Forecast 2025-2026

The Malaysian Palm Oil Council (MPOC) and various industry analysts anticipate a robust pricing environment for the first half of 2026.[21][22]

Forecast Period | Expected Range (MYR/MT) | Strategic Drivers [21][22][25][26][27] |

|---|---|---|

Q1 2026 | RM 4,000 - RM 4,300 | Seasonal supply decline; tree biological rest phase; Chinese New Year demand |

Q2 2026 | RM 4,200 - RM 4,500 | Depleting stocks from Q1; Ramadan/Hari Raya Aidilfitri demand surge; uncertainty over Indonesia B45 mandate |

H2 2026 | RM 3,800 - RM 4,100 | Seasonal peak production in Malaysia and Indonesia; stock replenishment; normalisation of global spreads |

Uncertainties for 2026

The European Union Deforestation Regulation (EUDR) and other global trade policies remain key uncertainties.

If these regulations lead to a bifurcated market - where "certified sustainable" oil trades at a significant premium to conventional oil - the FCPO benchmark may experience heightened volatility as the market adjusts to these new structural costs.[22][25]

The Role of Technology in Price Forecasting

The shift towards data-driven trading is evident in the increasing participation of algorithmic and high-frequency traders, who now account for a significant portion of "Foreign Institutional" volume (64% in H1 2025).[36]

These participants utilise:

Real-time satellite imagery to track plantation greenness (NDVI) and rainfall patterns

Enabling them to anticipate MPOB production figures before they are officially released[19][22]

For professional participants, the integration of "Alternative Data" sets into traditional Fundamental and Technical Analysis is no longer optional but a prerequisite for maintaining a competitive edge.[15][20][48]

Synthesis and Strategic Conclusion

The Crude Palm Oil Futures (FCPO) market represents the intersection of agricultural tradition and modern financial engineering. Its role as a global benchmark is sustained by deep liquidity, a transparent regulatory framework, and its ability to adapt to global imperatives such as sustainability.[1][2][3][5]

For various types of participants:

For Hedgers: Provides the necessary protection against the biological and meteorological volatility of the palm oil industry, enabling stable cash flows and protected margins.[3][4][54]

For Speculators: Offers high leverage and near-24-hour access to one of the most volatile and trending commodity markets in the world.[3][8][48]

For the Global Industry: Serves as a transparent "North Star" for pricing physical transactions, from Indonesian plantations to Indian refineries and European consumer goods factories.[5][8][31]

Outlook 2025-2026:

The market will likely be defined by "policy-driven volatility" - where government mandates on biofuels and trade regulations become as influential as the weather itself.[21][22][25]

In this environment, the standardised margin, clearing, and delivery mechanisms of FCPO will remain the bedrock of global price discovery and financial stability in the edible oil complex.

Participants must remain vigilant - combining traditional agronomic insights with sophisticated macroeconomic analysis and a disciplined approach to risk management to succeed in this high-stakes arena.

References

1. Global Price Benchmark for Crude Palm Oil - Bursa Malaysia

2. Crude Palm Oil Futures (FCPO) - Bursa Malaysia

3. The Global Price Benchmark for Crude Palm Oil - Bursa Malaysia

4. How to Trade FCPO on Bursa Malaysia - Phillip Capital

5. A Complete Guide to Commodities & Derivatives Trading in Malaysia

6. Modul Completed - Technical Analysis - Scribd

7. Options on Crude Palm Oil Futures (OCPO) - Bursa Malaysia

8. Trade Bursa Malaysia Futures - Interactive Brokers LLC

10. Bursa Malaysia FCPO Contract Specifications - KGI Securities

11. Crude Palm Oil Futures (FCPO) - Bursa Malaysia (BM)

12. Crude Palm Oil Futures (FCPO) Structured Warrants - Bursa Marketplace

13. The Beginner's Guide to FCPO Trading in Malaysia

14. Schedule 1 Agriculture Contracts - Bursa Malaysia

15. 5 Steps To Start Trading FCPO - Kenanga Futures

16. After-Hours Trading - Bursa Malaysia

17. FCPO Contract Specifications - Bursa Malaysia

18. FCPO Physical Delivery FAQ - Bursa Malaysia

19. An Analysis of Crude Palm Oil Production in Malaysia - OPIEJ

20. Malaysian Palm Oil Price Prediction Using ARIMA-ARCH Model - ResearchGate

21. CPO Prices to Rebound Toward RM4,500 - MPOC

22. Palm Oil Price Forecast and Production Outlook 2026 - Fastmarkets

23. Palm Oil Monthly Market Outlook - Bursa Malaysia

24. Palm Oil Supply and Demand is Shrinking - UkrAgroConsult

25. Crude Palm Oil Prices Seen Range-bound - Xinhua

26. Crude Palm Oil Prices Seen Range-bound - Xinhua Asia Pacific

27. Palm Oil Price Chart and Historical Data - Trading Economics

28. Intercommodity Spread Trading with FSOY and FCPO - MyBURSA

29. Impact of Soybean Futures and Crude Oil Futures on Palm Oil - MDPI

30. Spread Trading in CBOT Soybean Oil and BMD Crude Palm Oil - CME Group

31. A New Era for Soybean Oil and Palm Oil? - MyBURSA

32. Introduction to Crude Palm Oil Futures (FCPO) - YouTube

33. Impact of Macroeconomic Variables on FCPO - ResearchGate

34. Impact of Macroeconomic Variables on FCPO - IIUM Repository

35. Understanding the SPAN Methodology - MyBURSA

36. Complete Guide to Derivatives Trading in Malaysia - StashAway

37. East Malaysia Palm Oil Price Gateway - Bursa Malaysia

38. BMD Half FKLI FCPO Margin Agreement 2021 - Scribd

39. BMDC Margin Circular 2026 - Bursa Malaysia

40. FCPO Quotes and News - MyBURSA

41. BMDC Margin Circular 2025 - Bursa Malaysia

42. Understanding Futures Contract Rollovers - Investopedia

43. Settlement Process Malaysia - Clearstream

44. East Malaysia Crude Palm Oil Futures (FEPO) - Bursa Malaysia

45. FCPO Trading Volume at Bursa Malaysia - Bernama

46. Bursa Malaysia Derivatives Launches FEPO

47. Futures FAQ - UOB Kay Hian

48. Best Futures Brokers in Malaysia - Investing.com

49. List of Licensed Intermediaries - Securities Commission Malaysia

50. Futures Rollover Explained - QuantVPS

51. How to Roll Over Futures - Ventura Securities

52. How Futures Expiry and Rollover Work - Hola Prime

53. Futures Rollover Trading Tips - YouTube

54. Hedging Effectiveness of CPO Futures Market - IDOSI

Start Your Investment Journey

Investment knowledge is the first step. But without action, knowledge will not yield results.

Learn the Basics:

Get our free ebook for a comprehensive guide.

Start Investing:

To invest on Bursa Malaysia, open a CDS account now.

FAQ - FCPO Crude Palm Oil Futures Malaysia

What is FCPO and how does it work?

FCPO (Futures Crude Palm Oil) is a standardised derivatives contract traded on Bursa Malaysia Derivatives. Each contract represents 25 metric tonnes of crude palm oil, priced in MYR per metric tonne. Traders can take long (buy) or short (sell) positions to speculate on or hedge against palm oil price movements.

What is the minimum capital required to trade FCPO?

As of January 2026, the standard initial margin for one FCPO contract is RM 6,000. However, brokers may offer reduced intraday margins (e.g. 50%) for positions closed within the same trading day. Industry practitioners recommend having at least 6-12 months of emergency savings before trading.

What are the trading hours for FCPO?

FCPO trades in three sessions: Morning (10:30 AM - 12:30 PM MYT), Afternoon (2:30 PM - 6:00 PM MYT), and After-Hours T+1 (9:00 PM - 11:30 PM, Monday to Thursday). The T+1 session allows traders to respond to overnight developments in US and European markets.

How do I open a futures trading account in Malaysia?

You must open a Futures Trading Account through a licensed Trading Participant (broker) regulated by the Securities Commission Malaysia. Requirements include your Blue IC (for Malaysians) or passport with work permit (for foreigners), plus income documentation. Open a CDS account here.

What factors influence FCPO prices?

Key factors include: seasonal production cycles (peak July-October, low December-March), weather patterns and El Nino events, soybean oil price correlation, Indonesia biodiesel mandates (B35/B45/B50), USD/MYR exchange rates, global crude oil prices, and MPOB monthly stock and production data.