Elections & Bursa Stocks: The Real KLCI Pattern Before and After Malaysian General Elections

Every time a General Election (GE) approaches, the same question crosses the minds of Bursa Malaysia investors: "Should I sell my stocks before voting? Or wait for the result?" The popular myth says elections are always bad for the market - uncertainty, foreign funds fleeing, prices falling.

But when we look at the actual data of FBM KLCI performance around the three most recent elections - GE13 (2013), GE14 (2018), and GE15 (2022) - the pattern is far more nuanced than the myth. The short truth: an election is not automatically good or bad for the market. What moves the KLCI is whether the election result reduces or increases uncertainty.

In this article, we unpack:

- The real KLCI pattern before and after GE13, GE14, and GE15

- Myth vs reality about the effect of elections on stocks

- Why the market "overreacts" after an election result

- Foreign fund behaviour around the election period

- Sectors most affected by the political cycle

- Investor strategies to navigate election season wisely

The Myth: "Elections Are Always Bad for the Stock Market"

The most common narrative is that elections bring uncertainty, and uncertainty is bad for stocks. There's a partial truth here - the market does dislike uncertainty. But it oversimplifies reality.

Academic research examining the KLCI's reaction around Malaysian elections from GE5 (1978) to GE14 (2018) found an interesting pattern: the KLCI tends to "overreact" after an election, regardless of which coalition wins, according to a study published in an academic journal.

This means the big moves after an election are not necessarily reflecting changed fundamental value - they are often emotional reactions (either euphoria or panic) that subsequently revert to reasonable levels (mean reversion) within weeks to months.

The Real Pattern: KLCI Around the Last 3 Elections

Let's look at the actual data of the three most recent elections - each tells a different story.

GE13 (5 May 2013): A Classic Relief Rally

GE13 saw Barisan Nasional (BN) retain power, albeit with a lower popular vote. From a market standpoint, this result was "expected" by the majority of institutional investors - no major surprise.

The reaction: a classic relief rally. When uncertainty is resolved with an expected result, previously cautious investors quickly return to the market. The FBM KLCI surged significantly on the first trading day after the result - at one point the index rose more than 60 points in a day.

Lesson: a result that removes uncertainty (even a status quo) often triggers a short-term rise. But this euphoric rise typically partly fades in the following weeks.

GE14 (9 May 2018): A Historic Shock, the Market Rattled

GE14 was a historic event - for the first time in Malaysian history, the ruling party was toppled. Pakatan Harapan won, an outcome not anticipated by most investors and institutions.

Even though the power transition happened peacefully and democratically, the market reacted with fear of the unknown. What would the new government's economic policies be? What about existing mega projects? GST would be abolished - what was the impact on national revenue?

The result: the FBM KLCI fell about 6% a month after GE14. Not because economic fundamentals collapsed, but because the market dislikes surprises and was repricing policy risk.

Lesson: a result that is surprising and increases policy uncertainty can trigger significant selling - even if the democratic process itself is healthy.

GE15 (19 November 2022): Hung Parliament, Maximum Ambiguity

GE15 produced a hung parliament for the first time in Malaysian history - no coalition reached a simple majority. This was a scenario of maximum uncertainty: not only did investors not know the new government's policies, they didn't know who would form the government.

The market reacted negatively. Analysts cut their end-2022 FBM KLCI target to as low as 1,450 points in the absence of any coalition able to form a stable government, according to a Bernama report.

But - and this is the important part - when the unity government was formed and Anwar Ibrahim was appointed Prime Minister, the uncertainty began to ease. The market then stabilised as clarity returned.

Lesson: the market hates ambiguity over who governs more than it dislikes any particular party. Once clarity returns, the market recovers.

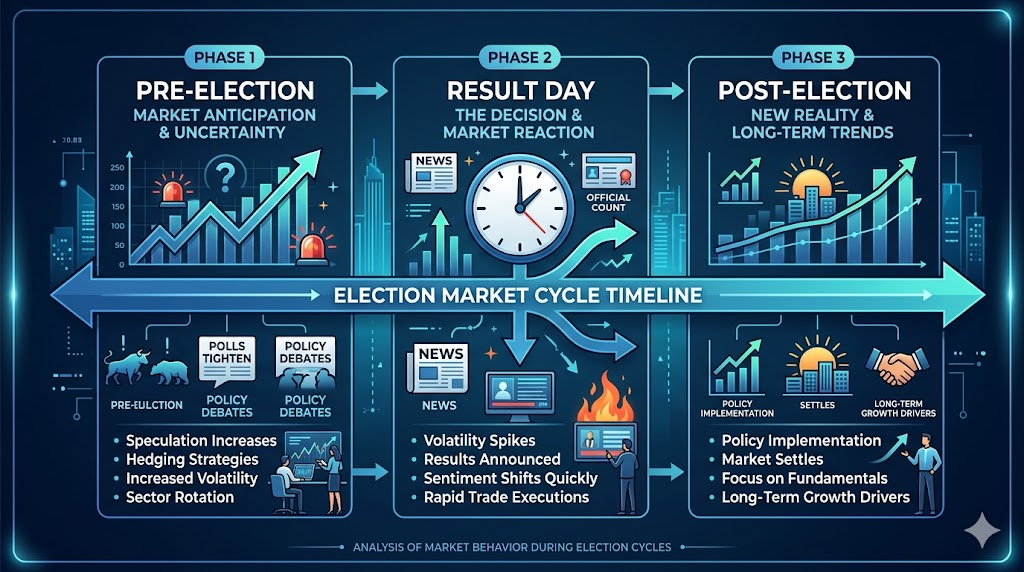

The Key Pattern: 3 Phases of the Election Cycle

From the data of three elections, a framework emerges - the political market cycle divides into three phases.

Phase 1: Pre-Election (Building Uncertainty)

In the months before the election date is announced and held:

- The market tends to trade sideways (range-bound) or slowly

- Foreign funds reduce exposure - they don't like carrying unpredictable political risk

- Trading volume may decline - investors "wait and see"

- Volatility increases as the election date approaches

Phase 2: Result Day (Sharp Reaction)

On the day and week the result is announced:

- A sharp reaction in one direction - the direction depends on whether the result reduces or increases uncertainty

- An expected result → relief rally (e.g., GE13)

- A surprising result → selloff (e.g., GE14)

- An unclear / hung result → selloff with high volatility (e.g., GE15)

Phase 3: Post-Election (Overreaction & Mean Reversion)

In the 1-3 months after the result:

- The initial reaction is often excessive (overreaction) - either euphoria or panic

- The market then reverts to fundamentally-driven levels

- When the new government clarifies policy, uncertainty eases and the market adjusts

- This is the phase where fundamental investors often find opportunities - buying quality stocks sold too cheap during the panic

Foreign Fund Behaviour Around Elections

One of the main drivers of KLCI movement around elections is foreign fund flows. Foreign institutional investors hold a large portion of KLCI component stocks, and they are highly sensitive to political risk.

The typical pattern:

- Before the election: foreign funds tend to reduce positions or stop buying - they don't want exposure to an unpredictable outcome

- After a clear result: if a stable government is formed, foreign funds can return gradually

- If uncertainty persists: outflows can continue until policy clarity emerges

This is why local institutional investors (such as EPF, PNB, KWAP) often play a stabilising role during election season - they buy when foreign funds sell, cushioning sharp declines.

Sectors Most Affected by the Political Cycle

Not all stocks react the same way to an election. Some sectors are more politically sensitive:

Highly Sensitive Sectors

- Construction & infrastructure - dependent on government projects and contracts. A change of government can mean projects are reviewed

- Utilities & energy - subject to subsidy and tariff policies set by the government

- Plantation & commodities - export policies, taxes, and subsidies can change

- Government-linked companies (GLCs) - sensitive to leadership changes and direction

Relatively Defensive Sectors

- Consumer staples - people keep buying food and necessities, regardless of who governs

- Healthcare - demand is inelastic to politics

- Globally-oriented exporters (e.g., gloves, semiconductors) - their revenue comes from abroad, less exposed to domestic policy

For investors worried about election volatility, tilting the portfolio towards defensive sectors during the pre-election period is a risk-reduction strategy.

Investor Strategies to Navigate Election Season

Based on the real pattern discussed, here are practical strategies:

1. Don't Try to "Time the Election"

Trying to predict the election result and time the market based on political forecasts is speculation, not investing. Many tried and failed at GE14 - no one predicted the power transition. For long-term investors, staying invested through the election cycle is usually the wisest choice.

2. Understand Your Own Recency Bias

After the market falls hard post-election, your brain will say "it will keep falling." After a relief rally, the brain says "it will keep rising." Both are recency bias - read more in Investor Psychology: 7 Mental Biases That Make You Lose Money on Bursa Malaysia.

3. Capitalise on the Overreaction

If you're a fundamental investor with a long-term thesis, the post-election overreaction phase often provides opportunities. When the market panic-sells quality stocks at cheap prices due to political fear (not business deterioration), that can be an attractive entry point.

4. Prepare a Cash Buffer Before the Election

Rather than selling all your stocks before the election (which means you're trying to time the market), consider keeping a little extra cash heading into the election. This isn't to avoid losses, but to have "ammunition" if an overreaction creates buying opportunities.

5. Focus on Fundamentals, Not Politics

Ultimately, long-term stock prices are driven by company profits, not who governs. A company that generates consistent profits will keep growing across multiple governments. For the basics of picking quality stocks, refer to Stocks for Beginners 2026: 7 Criteria to Pick Your First Stock at Bursa Malaysia.

Frequently Asked Questions (FAQ)

Does the KLCI always fall before an election?

Not always falls, but it tends to trade sideways or slowly in the pre-election period due to uncertainty. Foreign funds usually reduce exposure, causing weak momentum. But this isn't an automatic decline - it depends on overall market conditions and result expectations.

Should I sell my stocks before an election?

For long-term investors, selling all your stocks before an election means you're trying to "time the market" - a strategy that rarely works. GE14 history shows no one can predict the result accurately. Wiser: stay invested, perhaps keep a small cash buffer to capitalise on opportunities if there's an overreaction.

Why did the market fall after GE14 even though the power transition was peaceful?

The market isn't afraid of the democratic process - it's afraid of policy uncertainty. GE14 produced a new government whose economic policy was unclear (GST abolition, mega project reviews). The market sold while repricing risk, causing the KLCI to fall about 6% a month after GE14.

What does it mean when the market "overreacts" after an election?

Overreaction means the price movement after an election is often larger than justified by the actual change in fundamentals. Academic research found the KLCI tends to overreact after elections, then "mean revert" - returning to reasonable levels within weeks to months as emotions subside.

Which sectors are most affected by elections?

Highly politically-sensitive sectors include construction/infrastructure (dependent on government projects), utilities (subsidy/tariff policy), plantation, and government-linked companies (GLCs). Defensive sectors like consumer staples, healthcare, and globally-oriented exporters are relatively less affected.

Is an "expected" election result good for the market?

Generally, yes - in the short term. An expected result (like GE13) removes uncertainty, triggering a relief rally as cautious investors return to the market. But this relief rally usually partly fades after a few weeks - it's not a permanent rise.

How do foreign funds behave around Malaysian elections?

Foreign funds usually reduce positions before an election because they are sensitive to unpredictable political risk. After a clear result and a stable government forms, they can return gradually. Local institutions (EPF, PNB) often act as stabilisers by buying when foreign funds sell.

What's the best strategy for long-term investors during election season?

Stay invested and focus on fundamentals. Don't try to time the election. If possible, keep a small cash buffer to capitalise on a post-election overreaction. Consider tilting the portfolio towards defensive sectors if you're worried about volatility, but don't exit the market entirely - you risk missing the recovery.

Conclusion

The real pattern of KLCI performance around elections is far more nuanced than the "elections are always bad" myth. The data of the last three elections shows one consistent truth: what moves the market is not the election itself, but whether the result reduces or increases uncertainty. GE13 triggered a relief rally (expected result), GE14 triggered a selloff (policy shock), and GE15 triggered ambiguity (hung parliament) that subsequently eased.

For investors, the biggest lesson is don't try to predict politics. Focus on company fundamentals, understand your own cognitive biases, and treat the overreaction as an opportunity - not a threat.

Election season or not, investing in quality companies consistently is a winning strategy across multiple political cycles.

To start investing on Bursa Malaysia with a fundamentals-focused approach, you'll need a suitable trading account.

A CDS account lets you invest in Bursa Malaysia and overseas markets like US and Hong Kong, giving you diversification across multiple markets and political cycles - open your CDS account here.

For the basics of understanding the stock market and how to evaluate quality companies without being swayed by political noise, download the free Stock Market Basics Ebook.

Further Reading

- Politics and the Malaysian Stock Market: Reality, Risks, and Investor Opportunities

- What Is FBM KLCI

- Investor Psychology: 7 Mental Biases That Make You Lose Money on Bursa Malaysia

- Geopolitics as a Catalyst in Stock Trading: An Analysis

- FBM KLCI Upside Potential: Is Bursa Malaysia Returning to a Bull Market Era?