Plantation Stocks: The CPO Price Cycle & When Investors Should Enter

The plantation sector on Bursa Malaysia is one of the most cyclical in the local market. The earnings of companies like SD Guthrie (5285), Kuala Lumpur Kepong (2445), IOI Corporation (1961), Genting Plantations (2291), and United Plantations (2089) move almost in lockstep with one commodity: crude palm oil (CPO) prices.

Translation: if you want to invest in the plantation sector, you're NOT really investing in the company. You're investing in CPO prices. And CPO prices have their own cycle that's very different from bank, telco, or retail stocks.

For retail investors, this raises two questions: - What drives the CPO price cycle? - When is the best time to enter plantation stocks?

This article unpacks both with a clear analytical framework. Not a buy call for any stock, but a structural understanding to help you make better-informed decisions.

Why Are Plantation Stocks Cyclical?

Before talking about timing, understand why plantations are cyclical:

1. Plantation Revenue = Volume × Price - Volume (CPO produced) is relatively stable - oil palm trees take 4-5 years to mature, and yield declines slowly - But CPO prices are very volatile - can swing from RM2,000/MT to RM7,000/MT in 2-3 years

2. Cost Structure Is Largely Fixed - Labour, fertiliser, machinery, depreciation - mostly fixed costs - When CPO prices rise, every dollar above production cost flows directly into profit (operating leverage) - When prices fall, losses come fast

3. High Operating Leverage A simple example: if a plantation player's production cost is RM2,500/MT: - CPO price RM3,500/MT = margin RM1,000/MT - CPO price RM4,500/MT = margin RM2,000/MT (margin 2x even though price rose just 28%) - CPO price RM5,500/MT = margin RM3,000/MT (margin 3x)

This is why plantation company earnings can double or triple when CPO rallies - and conversely collapse when it falls.

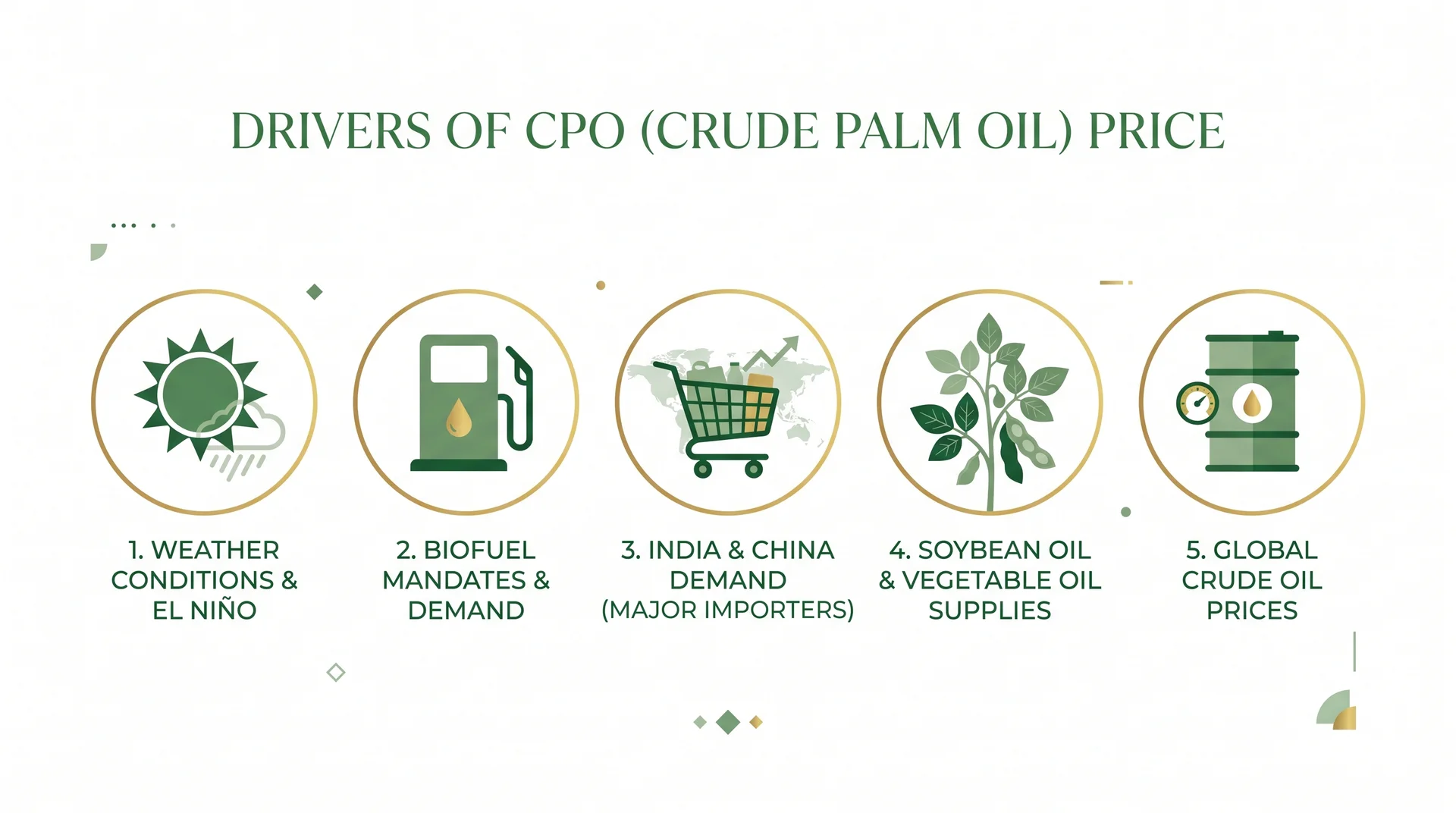

5 Key Drivers of CPO Prices

To understand when CPO will rise or fall, monitor 5 key drivers:

Driver #1: Weather - El Niño and La Niña

Indonesia and Malaysia together produce ~85% of global palm oil supply. Both countries are exposed to tropical weather.

- El Niño (hot, dry weather): Palm trees become stressed, fruit yields drop, and drought can cause water shortages reducing FFB (fresh fruit bunch) yields. Production impact typically appears 6-12 months after El Niño because palm trees take time to recover.

- La Niña (wetter weather): Brings heavy rain and flooding. While it might appear good, sustained flooding actually disrupts harvesting and can damage estates.

According to UOB Kay Hian, not all La Niñas are the same - the impact on CPO depends on severity and duration.

What Investors Should Watch: - NOAA Climate Prediction Center (El Niño/La Niña forecasts) - MPOB (Malaysian Palm Oil Board) reports on monthly FFB yields - Extreme weather news from Indonesia/Malaysia

Driver #2: Biofuel Mandates (Indonesia & Malaysia)

This is the most structural demand driver in recent years.

- Indonesia: B40 biodiesel mandate since January 2025, with plans for B50 in 2026. Each blend ratio increase means millions of tonnes of CPO are pulled from exports for domestic absorption

- Malaysia: B15 programme expected to start June 2026 - mandating 15% palm oil blend in diesel. This will draw an additional ~1 million tonnes of CPO into local market

When biofuel mandates rise, exports drop → CPO prices rise.

Driver #3: India and China Demand

These two countries are the largest CPO importers in the world. Their demand can swing global prices significantly.

India: - #1 importer, ~9 million tonnes annually - Demand concentrated around festival season (Diwali October-November) - Highly sensitive to import duty and price differential with soybean oil

China: - #2 importer, ~6 million tonnes annually - More stable demand but can shift with US-China trade tensions (which affect US soybean oil supply)

What Investors Should Watch: - India stockpile (monthly) - CPO vs soybean oil import ratio in India and China - Festival demand cycles (Diwali, Hari Raya, Lunar New Year)

Driver #4: Soybean Oil Prices (Substitute Vegetable Oil)

Palm oil and soybean oil are substitutes in the global cooking oil market. When soybean oil prices rise, buyers shift to CPO. When soybean oil prices fall, CPO becomes less attractive.

CPO-SBO Spread (Crude Palm Oil to Soybean Oil): - CPO typically trades at a discount to soybean oil (soybean oil is considered more premium) - Wider spread (CPO cheaper) = CPO more competitive → demand rises - Narrower spread (CPO close to SBO) = buyers switch to SBO → CPO demand drops

Watch CBOT Soybean Oil futures and Bursa Malaysia FCPO futures for early signals. For FCPO trading basics, see our article: FCPO: Panduan Lengkap Dagangan Minyak Sawit Mentah di Malaysia.

Driver #5: Crude Oil Prices

When crude oil prices are high, biofuels become more economical and demand for CPO as a biofuel feedstock rises. Many countries raise biodiesel mandates when crude prices are high.

As a rule of thumb: Brent crude above USD90/barrel = bullish for CPO, because this opens price space for biofuel to be competitive.

CPO Cycle History: What History Tells Us

Let's review the CPO cycle of the past 15 years (a general overview, not specific prices):

2008-2009 (Bull-Bust): CPO peaked ~RM4,500/MT mid-2008, then crashed ~50% within 6 months (global financial crisis)

2010-2012 (Multi-year Bull): Recovery and prolonged rally driven by global biofuel demand and supply scarcity

2013-2018 (Range-bound Bear): Long sideways/bear period, CPO traded between RM2,000-2,800/MT

2019-2020 (La Niña Rally): Drought followed by La Niña triggered a significant rally

2021-2022 (All-time High): CPO hit all-time highs amid supply collisions (Indonesia temporary export ban) + high demand

2023-2024 (Cooling Off): Sideways to bear as supply recovered and global economy slowed

2025-2026: Range-bound, Maybank forecasts RM4,100/MT for 2026, MARC forecasts RM3,850-4,250/MT

Lessons from History: - The CPO cycle typically lasts 3-5 years from peak to peak - Bull cycles are driven by supply shocks (weather) or demand shifts (new biofuel mandates) - Bear cycles occur as supply recovers and demand stabilises - Patient investors who enter at bear bottoms often see strong returns

Major Plantation Stocks on Bursa Malaysia

Below are the major players retail investors should know. This isn't a buy recommendation - just a list for further research:

Big Players (Diversified, Liquid)

SD Guthrie Berhad (SDG, 5285) - formerly Sime Darby Plantation - Largest palm oil producer in Malaysia by land bank - Diversified operations: Malaysia, Indonesia, PNG, Liberia - Fertiliser costs locked for the year - considered a preferred pick by CIMB

Kuala Lumpur Kepong Berhad (KLK, 2445) - Major integrated player with upstream + downstream (oleochemicals) - Land bank in Malaysia, Indonesia, and Liberia - Stock research: Kuala Lumpur Kepong (KLK, 2445)

IOI Corporation Berhad (1961) - Integrated player upstream + refining - Europe market exposure through specialty fats - Structurally separate from IOI Properties (5249)

Genting Plantations Berhad (GENP, 2291) - Subsidiary of Genting Group - Significant Indonesia exposure - Has biotech and downstream segments

United Plantations Berhad (UTDPLT, 2089) - Consistent dividend track record - Family management with strong reputation - Smaller but quality

Pure Upstream (More Sensitive to CPO Prices)

Johor Plantations Group Berhad (JPG) - Recent IPO (Q3 2024) - Pure upstream - most sensitive to CPO movements - Stock research: Johor Plantations Group (JPG)

TA Ann Holdings Berhad (TAANN, 5012) - Sarawak-based producer - Diversified into timber & wooden products - Stock research: TA Ann Holdings (TAANN, 5012)

TSH Resources Berhad (TSH, 9059) - Sabah + Indonesia exposure - Mid-size operations - Stock research: TSH Resources (TSH, 9059)

Hap Seng Plantations (HSPLANT), Boustead Plantations (BPLANT), Kim Loong Resources (KMLOONG) - smaller-mid cap players that also move with the CPO cycle

When Should Investors Enter Plantation Stocks? (Signal Indicators)

Here's the most practical part. The following are signal indicators that history shows are the best times to consider entering the plantation sector:

Signal #1: CPO Near/At Cost of Production

- Average Malaysian production cost: ~RM2,200-2,800/MT (varies by player, age of trees)

- When CPO approaches these levels, plantation players are losing or breaking even

- History shows this is often a capitulation bottom before recovery

- Risk: prices can fall further below cost (short term) but seldom for long

Signal #2: High Malaysia/Indonesia Stockpile

- MPOB monthly reports on end-month CPO stockpile in Malaysia

- High stockpile (>3 million tonnes) = oversupply, price pressure

- Progressive stockpile decline = supply tightening, bullish signal

- Monitor at the MPOB website

Signal #3: Confirmed Strong/Severe El Niño

- NOAA issues monthly ENSO advisories

- "Strong El Niño" or "Severe El Niño" is often followed 6-12 months later by a CPO supply shock

- Investors can position early before signals reach prices

Signal #4: New Biofuel Mandate Announced

- Announcements of B40 → B50 by Indonesia, or B15 → B20 by Malaysia

- Forward-looking impact: pulls supply from export markets, raises prices

- Governments typically give 6-12 months advance notice

Signal #5: Very Wide CPO-SBO Spread

- When CPO trades at a discount >USD200/MT vs soybean oil

- Substitution effect: soybean oil buyers switch to CPO

- Demand rises, CPO prices supported upward

Signal #6: Very Bearish Sentiment (Contrarian Indicator)

- Mass analyst downgrades to "Neutral" or "Underweight"

- News about "plantation sector struggling" in mainstream media

- Bottom often forms when sentiment is at extremes

When Investors Should NOT Enter

Conversely, several signals indicate not the best time to enter:

1. Very High Stockpile & Weak Demand: indicates structural oversupply, prices struggle to hold

2. Very Bullish Sentiment (Contrarian): when analysts collectively upgrade to "Buy", peak sometimes near

3. Sharp Crude Oil Drop: reduces biofuel competitiveness, downward pressure on CPO

4. Indonesia Lifts Export Restrictions: more supply enters the market

5. Indonesia/Malaysia Region Has Excellent Weather: meaning high FFB yields - supply rises

Cyclical Strategies for Retail Investors

Below is a practical framework for retail investors approaching plantation:

Strategy 1: Wait for Cycle Bottom (Patient Approach)

- Plan: Wait until 3-4 of the 6 signal indicators above give buy signals

- Action: Open positions gradually (DCA) over 3-6 months

- Holding period: 18-36 months (ride the cycle up)

- Exit: When signals start turning bearish (sentiment peak, low stockpile, etc.)

Strategy 2: Pair Trade Within Sector

- Plan: When confident on the sector but unsure which player

- Action: Buy a portfolio of 3-4 plantation stocks (mix big-cap + pure upstream)

- Hedging: Big-cap (SDG, KLK) for stability, pure upstream (JPG, smaller players) for upside leverage

Strategy 3: Dividend Income During Bear

- Plan: Patient dividend investors can enter plantation during bear period

- Action: Choose quality players with dividend track records (UTDPLT, KLK)

- Holding period: Indefinite, dividend stream while waiting for cycle

Strategy 4: Avoid During Late Cycle

- Plan: When CPO is far above historical average and the rally has gone on for months

- Action: Trim exposure, don't add

- Reasoning: Mean reversion almost always happens - just a matter of when

Strategy 5: Use FCPO Futures (Advanced)

- For more sophisticated investors

- Direct CPO price exposure without single stock risk

- Requires special futures account and margin

- Risk: high leverage, not for beginners

Risks & Important Considerations

1. Cycle Isn't Always Predictable

Even if you follow all signals, exact timing is very difficult. There are always false signals and prolonged bears/bulls.

2. Company-Specific Risks

Beyond CPO, other factors matter: - Land bank quality (tree age, location) - Operational efficiency (FFB yield per hectare) - Cost discipline (input costs vs selling prices) - ESG concerns (especially for Indonesia, Liberia operations)

3. Geopolitical & Regulatory Risk

- Indonesia export policies (can change quickly)

- EU Deforestation Regulation (EUDR) implications for European exports

- Tariffs from major buyers

- Land rights issues (especially Indonesia)

4. Long-Term Climate Change Risk

- World Bank's 2026 forecast shows 8.3% potential GDP loss for Malaysia by 2050 from climate - the agriculture sector including plantations is most exposed

- For full context, see our article on Malaysia's climate impact on Bursa

5. Diversification Remains Key

Even with strong plantation thesis, don't put more than 15-20% of your portfolio in one sector. Banking, telco, healthcare all need exposure too.

FAQ: Common Questions About Plantation Stocks

1. How long is a typical CPO cycle?

Full cycles peak-to-peak typically last 3-5 years. But certain cycles can be longer (6-7 years) when there's a structural shift like changing biofuel mandates or prolonged drought.

2. What is the cost of production for Malaysian CPO?

Depending on company and tree age, but average RM2,200-2,800/MT. Players with older land banks have higher costs (yields decline). Sabah/Sarawak players have lower labour costs than Peninsular Malaysia.

3. Are plantation stocks Shariah-compliant?

Most major players are Shariah-compliant: - Shariah-compliant: SD Guthrie, KLK, IOI Corp, Genting Plantations, United Plantations, JPG, TA Ann, TSH - The Shariah-compliant list is updated by the Securities Commission (SC) every 6 months

4. Which plantation stock is most CPO-sensitive?

Pure upstream players are most sensitive: - JPG, TSH, TA Ann (more upstream-focused) - Smaller mid-caps like Hap Seng Plantations, Boustead Plantations

Integrated players (KLK, IOI Corp) have downstream segments that partly cushion against CPO volatility.

5. Should I avoid plantation stocks because of ESG concerns?

Depends on your investor profile: - Strict ESG: may need to avoid or pick players with RSPO certification and no deforestation practices - Pragmatic: Malaysian players generally have higher standards than Indonesian - Each company differs - check ESG ratings and sustainability reports

6. What's the right plantation exposure in a portfolio?

Rule of thumb: 5-10% portfolio in plantation sector, with diversification across 2-3 different names. More bullish investors can go up to 15%, but >20% is too high a concentration.

7. What's the difference between FCPO and plantation stocks?

- FCPO (Futures Crude Palm Oil): futures contracts on CPO directly. Most pure exposure but leveraged and short-term focused

- Plantation stocks: equity ownership in companies. Exposure to CPO + company operational factors

For deeper FCPO understanding: FCPO: Panduan Lengkap Dagangan Minyak Sawit Mentah.

8. How do I monitor MPOB announcements and the latest CPO data?

Key sources: - MPOB (Malaysian Palm Oil Board) - monthly stockpile, export, production data - Bursa Malaysia FCPO - real-time futures prices - The Edge Malaysia, BernamaBiz - plantation sector news - CIMB, Maybank IB, Hong Leong - analyst reports (typically as broker clients)

Conclusion

The plantation sector on Bursa Malaysia is one of the most cyclical sectors - earnings and stock prices move almost in lockstep with CPO prices. For retail investors, this means timing matters more than stock picking. Understanding the 5 key drivers of CPO prices (weather, biofuel mandates, India/China demand, soybean spread, crude oil) and using 6 signal indicators for cycle bottoms offers a more disciplined framework than just buying because "plantation stocks are popular".

But remember: cycles don't always behave as expected. Diversification across sectors, patience with holding periods, and discipline with risk management matter more than perfect timing.

Before making any investment decision, ensure you have an active trading account and a strong grasp of investing fundamentals.

To start investing in Bursa Malaysia and overseas markets like the US and Hong Kong, you need a CDS account - register your CDS account with Mahersaham here.

For investing fundamentals including how to read financial statements, valuing cyclical companies, and thematic investment strategies, get our free stock investing basics ebook.

Further Reading

- FCPO: Panduan Lengkap Dagangan Minyak Sawit Mentah di Malaysia - CPO futures trading basics

- Minyak Sawit Dan Keluaran Dalam Negara Kasar - Palm oil's role in Malaysia's economy

- Iklim Boleh Telan 8.3% KDNK Malaysia: Saham Bursa Mana Untung, Mana Rugi? - Climate risk context for plantation sector

- Kuala Lumpur Kepong (KLK, 2445) - Deep stock research on integrated plantation player

- Johor Plantations Group (JPG) - Stock research on pure upstream player