Property Investment Malaysia: Complete Beginner Guide

Property investment is often cited as one of the safest ways to build long-term wealth. In Malaysia, property is not just a place to live — it is an asset that can generate passive income through rental, and its value tends to increase over time.

But for beginner investors, the world of property can seem complex and intimidating. How much capital is needed? What type of property is suitable? What risks need to be considered? This article will answer all these questions comprehensively.

Whether you're a stock investor looking to diversify your portfolio, or a young professional planning your first property purchase, this guide will help you understand the basics of property investment in Malaysia.

What Is Property Investment?

Property investment means buying property (land, houses, apartments, commercial premises) with the aim of generating profit — either through capital appreciation or rental income.

Unlike living in your own home, property investors see property as an asset that works for them. For example:

- Buy a house at RM300,000, sell it 5 years later at RM400,000 — that's capital appreciation

- Buy an apartment, rent it out at RM1,500 per month — that's rental income

- Or a combination of both: rent it out for several years, then sell at a higher price

According to data from the National Property Information Centre (NAPIC), the house price index in Malaysia has on average increased annually over the long term, making property one of the most stable assets for investment.

5 Advantages of Property Investment in Malaysia

1. Tangible Asset

Unlike stocks or crypto that exist digitally, property is a physical asset you can see and touch. You own something real — land, buildings, and space. This gives many investors a high sense of psychological security.

2. Passive Income Through Rental

Rented property generates consistent monthly income. In major urban areas like Kuala Lumpur, Petaling Jaya, and Penang, rental demand remains high especially from workers, students, and expatriates. Average rental yield in Malaysia ranges between 3-5% per annum depending on location and property type.

3. Leverage Through Bank Financing

This is a unique advantage of property absent in most other investments. Banks allow you to buy property by paying only 10% deposit (or less for first homes), while the remaining 90% is financed through a housing loan.

4. Long-Term Value Appreciation

History shows that property prices in Malaysia tend to increase over the long term, especially in areas experiencing infrastructure development. Projects like MRT, LRT, and new highways directly increase property values in their vicinity.

5. Inflation Protection

When prices rise (inflation), property values and rental rates also increase. This means property acts as a hedge against inflation — your money doesn't lose purchasing power.

5 Types of Property Investment in Malaysia

1. Residential Property

The most popular investment type — including terrace houses, semi-Ds, bungalows, apartments, and condominiums. Suitable for beginners as they're easy to rent out and demand is always present. Starting capital: RM50,000 - RM150,000 (deposit + ancillary costs).

2. Commercial Property

Includes shops, offices, retail lots, and business premises. Rental returns are usually higher (5-8%) compared to residential, but starting capital is also larger and vacancy risk is higher.

3. Vacant Land

Buying land and waiting for value to increase. Advantage: low maintenance costs. Disadvantage: no rental income, and land cannot be financed as easily as completed property. Most suitable for long-term investors.

4. REIT (Real Estate Investment Trust)

For those who don't want to buy physical property, REITs on Bursa Malaysia allow you to invest in property indirectly. You buy REIT units like buying stocks, and receive dividends from the rental income of properties in the REIT portfolio. Starting capital: as low as RM100.

5. Subsale Property (Secondary Market)

Buying existing property from previous owners (not developers). Advantages: can inspect the actual unit, mature location, and sometimes below market price.

How Much Capital Do You Really Need?

This is the most important question — and the answer might surprise many people. Buying property isn't just about paying the deposit. Here's a breakdown of the actual costs:

Purchase Costs for RM400,000 Property (Example)

| Item | Estimated Cost |

|---|---|

| Deposit (10%) | RM40,000 |

| Legal fees (S&P) | RM5,000 - RM8,000 |

| Stamp Duty | RM5,500 |

| Valuation Fee | RM1,500 - RM2,000 |

| Loan legal fees | RM3,000 - RM5,000 |

| MRTA/MLTA Insurance | RM5,000 - RM15,000 |

| Total estimate | RM60,000 - RM75,500 |

Stamp Duty Rates 2026

According to the Inland Revenue Board (LHDN), stamp duty rates for property transfers are:

- First RM100,000: 1%

- RM100,001 - RM500,000: 2%

- RM500,001 - RM1,000,000: 3%

- Above RM1,000,000: 4%

RPGT (Real Property Gains Tax)

According to the Real Property Gains Tax Act, RPGT rates for Malaysian citizens in 2026 are:

- Disposal within years 1-3: 30%

- Disposal in year 4: 20%

- Disposal in year 5: 15%

- Disposal after year 5: 0% (no tax)

This means if you plan to invest long-term (more than 5 years), you won't need to pay any RPGT — another incentive for long-term property investment.

7 Steps to Start Property Investment

Step 1: Assess Your Financial Capability

Before anything, calculate your net income and ensure monthly loan instalments don't exceed 30-35% of your income. Bank Negara Malaysia advises Malaysians not to overburden themselves with debt.

Step 2: Determine Your Investment Strategy

Do you want to:

- Buy & hold (rent): Buy, rent out, collect long-term passive income

- Buy & flip: Buy below market price, renovate, sell at a higher price

- Buy & wait: Buy land/property, wait for area development, sell later

Step 3: Choose a Strategic Location

Location is the most critical factor in property investment. Look for areas with new infrastructure development, population and employment growth, amenities like schools, hospitals, shopping centres, and low rental vacancy rates.

Step 4: Do Market Research

Compare at least 5 properties before making a decision. Use platforms like PropertyGuru, iProperty, and EdgeProp to check market prices, past transactions, and area trends.

Step 5: Check Loan Eligibility

Visit a bank or use a mortgage broker to check your housing loan eligibility. Factors considered: monthly income, existing debt commitments (DSR), CCRIS/CTOS credit score, and employment tenure.

Step 6: Perform Due Diligence

Before signing any documents: check the land title and property status, visit the property physically (for subsale), check developer track record (for new properties) through KPKT, and read the Sale & Purchase Agreement carefully.

Step 7: Diversify Your Portfolio

Don't put all your money into one property. Ideally, combine property investment with other assets like stocks, REITs, or fixed deposits to reduce overall risk.

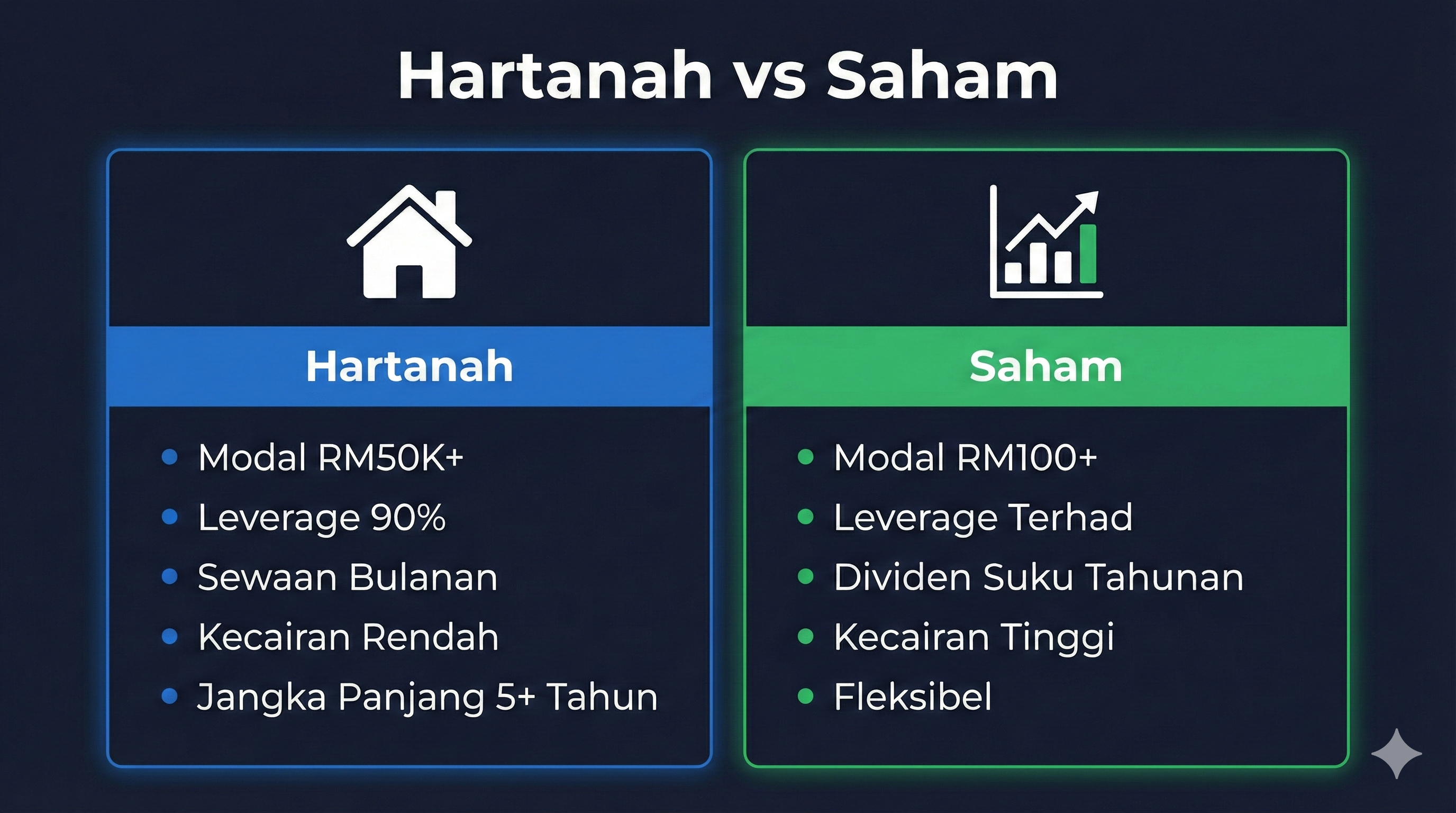

Property vs Stocks: Which Is Better?

This is a frequently asked question — and the answer depends on your situation.

| Criteria | Property | Stocks |

|---|---|---|

| Starting capital | RM50,000+ | As low as RM100 |

| Liquidity | Low (takes time to sell) | High (sell anytime) |

| Passive income | Monthly rental | Dividends (usually quarterly) |

| Leverage | Yes (90% bank loan) | Limited (margin account) |

| Management costs | High (maintenance, taxes, insurance) | Low (broker fees only) |

| Risk | Moderate | Depends on stock |

| Ideal timeframe | 5+ years | Flexible |

The truth is, both have a place in a healthy portfolio. Smart investors don't choose just one — they diversify between property, stocks, and other assets.

5 Property Investment Risks You Must Know

1. Vacancy Risk

Property that can't be rented means you're bearing loan instalments without rental income. This can become a heavy financial burden.

2. Interest Rate Risk

When the OPR (Overnight Policy Rate) increases, housing loan interest rates also rise. In 2026, the OPR stands at 3.00%, and any increase will directly impact your borrowing costs.

3. Liquidity Risk

Unlike stocks that can be sold in minutes, property requires weeks or months to sell. If you need cash urgently, property isn't an asset that can be liquidated quickly.

4. Hidden Costs

Many beginner investors are surprised by unexpected costs — maintenance, repairs, assessment rates, quit rent, insurance, and renovation costs.

5. Market Risk

Although property is generally stable, there are periods when property prices don't increase or even decline — especially for properties in less strategic locations or oversupplied areas.

Frequently Asked Questions (FAQ)

What is the minimum capital to start property investment in Malaysia?

For physical property, you need at least RM50,000 - RM100,000 for deposit and ancillary costs for property priced RM300,000 - RM500,000. However, if you want property exposure with small capital, REITs on Bursa Malaysia allow you to start with as low as RM100.

Is property investment suitable for young people?

Yes, in fact the earlier you start, the better. Young investors have the advantage of longer loan tenures (up to 35 years) and more time for property to appreciate in value.

First home: to live in or for investment?

This depends on your situation. If you're still renting, buying a home to live in usually makes more sense as you're "paying" for your own asset rather than paying rent to a landlord.

What is rental yield and what's considered good?

Rental yield is the percentage of annual rental returns compared to property price. Formula: (Annual Rental / Property Price) x 100%. In Malaysia, rental yield of 4-6% is considered good.

Is REIT the same as buying property?

Not entirely. REITs allow you to invest in property portfolios indirectly through purchasing units on Bursa Malaysia. You get property exposure without managing tenants or maintenance.

Do I need to pay RPGT if I sell after 5 years?

No. For Malaysian citizens, disposal of property after the 5th year of ownership is not subject to RPGT (0%).

How does property investment compare to stock investment?

Both have their respective advantages. Property offers high leverage and stable rental income, while stocks offer high liquidity and low starting capital. An ideal investment portfolio usually contains a combination of both.

What are the most common mistakes beginner property investors make?

Key mistakes include: not doing thorough location research, taking loans beyond affordability, not accounting for hidden costs, buying based on emotions, and not having a financial backup plan if the property fails to rent out.

Conclusion

Property investment in Malaysia remains one of the best choices for building long-term wealth. With the right understanding of property types, actual costs, and risks involved, you can make smarter and more measured investment decisions.

The key is — start with knowledge, not emotion. Do your research, calculate your affordability, and take the first step with confidence.

If you're also interested in diversifying your investments into the stock market beyond property, you can open a CDS account through Mplus to start owning your first stocks on Bursa Malaysia. And to build a solid foundation in stock investing, download the Free Stock Basics Ebook here — over 100 pages of comprehensive guides for beginner investors.

Further Reading

- Complete Guide: How to Start Investing in Stocks 2026 — Step-by-step guide if you also want to invest in stocks

- Gold Investment Malaysia 2026: Complete Guide — Another investment alternative besides property

- EPF Dividends 2026: Latest Rates & How to Check — Your retirement savings and how it relates to investment

- Stocks for Beginners 2026: 7 Criteria for Picking Your First Stock — How to choose your first stock market investment

- 5 Key Mistakes Beginners Make in the Stock Market — Avoid common investment mistakes