Sharpe Ratio Explained: Risk-Adjusted Returns for Investors

Picture two investors. The first earns a 20% annual return, the second earns 12%. Who is the better investor? Most people answer "the one with 20%" right away. But that answer could be wrong.

The reason is simple: high returns usually come with high risk. If the first investor had to endure wildly volatile swings (up 8% one day, down 10% the next) to capture that 20%, while the second earned 12% on a far smoother ride, then the second investor's performance is actually better once you judge it fairly.

This is exactly the question the Sharpe Ratio answers: is the return you earn truly worth the risk you take? In this guide you will learn what the Sharpe Ratio is, the formula and how to calculate it step by step, a worked example with Malaysian market context, how to read the value, and the limitations many investors overlook.

What Is the Sharpe Ratio?

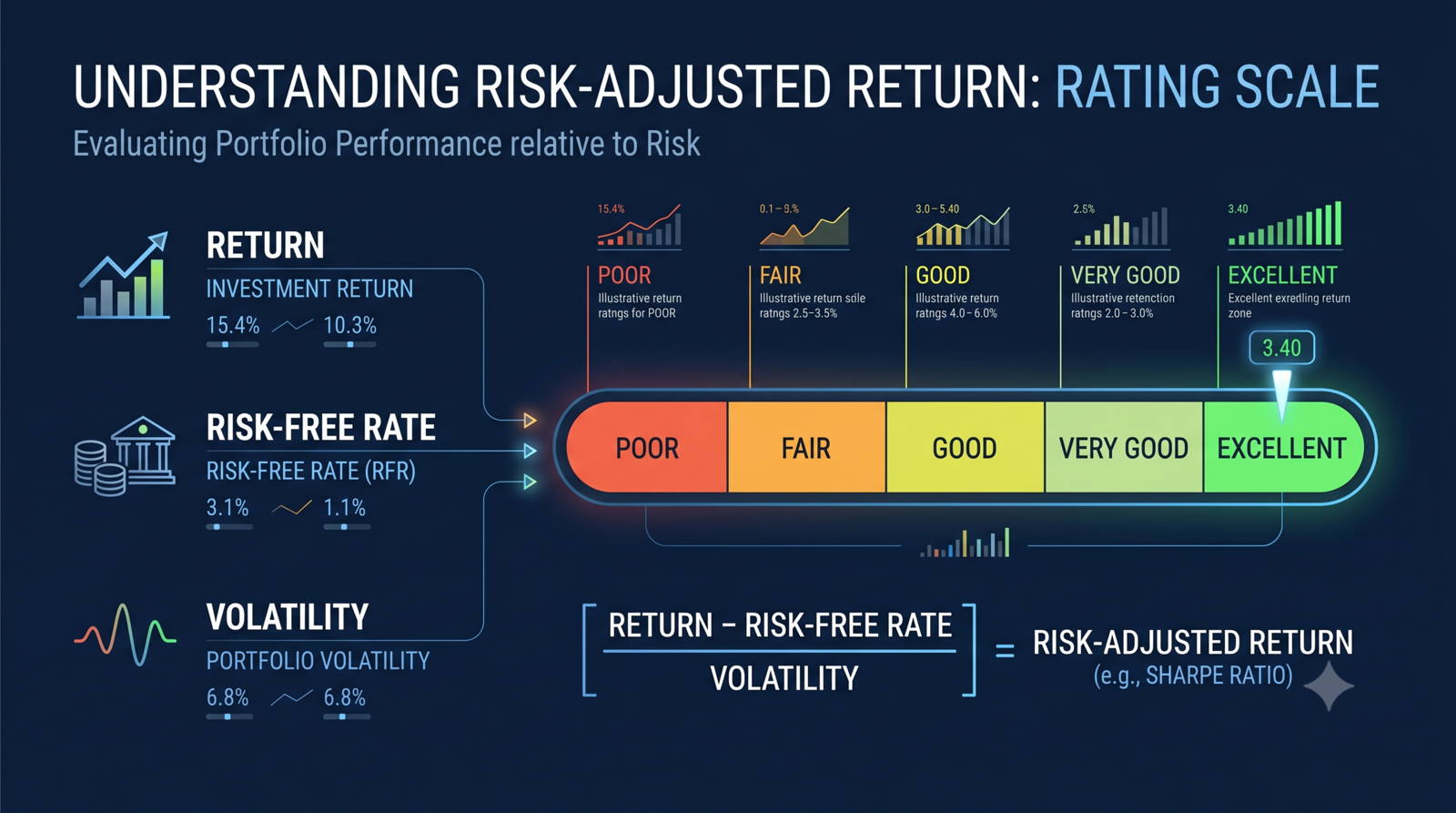

The Sharpe Ratio is a metric that measures risk-adjusted return. In plain terms, it tells you how much extra return you earn for every unit of risk you take on.

The ratio was created by William F. Sharpe, an American economist who won the Nobel Prize in Economics in 1990 for his contributions to modern financial theory. Since then, the Sharpe Ratio has become one of the most widely used tools by fund managers, analysts, and individual investors around the world to assess investment performance fairly.

The core idea is this: anyone can earn high returns by taking big risks (for example, buying penny stocks or highly volatile crypto). The more important question is whether that return is worth the stress and probability of loss it carries. The Sharpe Ratio turns this fuzzy question into a single, comparable number.

Quick Answer: The Sharpe Ratio Formula

The Sharpe Ratio formula is:

Sharpe Ratio = (Rp - Rf) / SDp

Where:

- Rp = Portfolio or investment return

- Rf = Risk-free rate of return

- SDp = Standard deviation of portfolio returns (a measure of volatility)

In short: take your investment return, subtract the risk-free rate (what you could earn without any risk), then divide by volatility. The higher the resulting number, the better your return relative to the risk taken.

Understanding the Three Components

To use the Sharpe Ratio correctly, you need to understand each component.

1. Portfolio Return (Rp)

This is the total return of your investment over a period, typically one year. It includes capital gains and dividends received. For example, if your portfolio starts at RM10,000 and grows to RM11,500 including dividends in a year, your return is 15%.

2. Risk-Free Rate (Rf)

The risk-free rate is the return you can earn without taking any risk. In Malaysia, the common proxy is the short-term Malaysian Treasury Bill rate or the Overnight Policy Rate (OPR).

As of 2026, the OPR set by Bank Negara Malaysia stands at 2.75%, while short-term treasury bill rates hover around 3%. For the calculations in this article, we use Rf = 3% as a reasonable estimate. The logic is simple: if you can earn 3% without risk, your investment return must first clear that 3% before it counts as a true "risky" return.

3. Standard Deviation (SDp)

Standard deviation measures how far your investment returns swing away from the average. This is the measure of volatility, or risk, in the formula. Stable investments (such as bond funds) have a low standard deviation, while technology stocks or crypto have a high standard deviation. The higher the standard deviation, the bigger the "penalty" in the Sharpe Ratio formula.

A Worked Sharpe Ratio Example

Let's look at a concrete example to understand the power of this metric. Suppose you are evaluating two portfolios:

Portfolio A (Aggressive):

- Return (Rp): 18%

- Standard deviation (SDp): 20%

Portfolio B (Balanced):

- Return (Rp): 12%

- Standard deviation (SDp): 8%

With a risk-free rate of Rf = 3%, let's calculate:

Portfolio A Sharpe Ratio = (18% - 3%) / 20% = 15 / 20 = 0.75

Portfolio B Sharpe Ratio = (12% - 3%) / 8% = 9 / 8 = 1.13

The result surprises many people. Even though Portfolio A delivers a higher return (18% versus 12%), Portfolio B is actually more efficient because its Sharpe Ratio is higher (1.13 versus 0.75). This means Portfolio B delivers more return for every unit of risk taken.

This is the key lesson of the Sharpe Ratio: the highest return is not necessarily the best investment. What matters is return that is efficient relative to risk.

How to Read the Sharpe Ratio Value

After calculating, how do you interpret the number? Here is the general guide used by the finance industry:

| Sharpe Ratio | Interpretation |

|---|---|

| Below 1.0 | Sub-par - return is not worth the risk |

| 1.0 - 1.99 | Good - return and risk are balanced |

| 2.0 - 2.99 | Very good - efficient return relative to risk |

| 3.0 and above | Excellent - rarely achieved consistently |

Note that a negative value (below 0) means your investment return is lower than the risk-free rate. In this case, you would actually be better off putting your money in a risk-free instrument such as ASB or treasury bills, because you are taking risk without a worthwhile reward.

One important caveat: a consistently very high Sharpe Ratio (say 3 and above) should raise questions. It may signal a data period that is too short, or a strategy that hides large but rare tail risk.

Why the Sharpe Ratio Matters for Investors

Many new investors focus on a single number: how much profit, in percent. But experienced investors know that how you earn that return is just as important as the amount.

The Sharpe Ratio matters for several reasons. First, it enables fair comparison between investments with different risk profiles, such as comparing an aggressive equity fund with a balanced fund. Second, it helps you identify whether a fund manager's outstanding performance comes from skill, or simply from taking excessive risk that happened to pay off.

Third, and most practically, the Sharpe Ratio helps you sleep at night. A portfolio with a high Sharpe Ratio gives a smoother investment journey, reducing the temptation to panic-sell when markets fall. To understand more about evaluating overall performance, read our guide on how to measure your own portfolio performance.

Using the Sharpe Ratio to Compare Stocks, ETFs & Unit Trusts

One of the most practical uses of the Sharpe Ratio is comparing different investment instruments. You can calculate the Sharpe Ratio for:

- Individual stocks on Bursa Malaysia - compare a stable blue chip with a volatile growth stock

- ETFs - for example, comparing a Gold ETF with an index ETF

- Unit trusts - many fund fact sheets already list the Sharpe Ratio

- Your entire portfolio - to assess whether your mix of investments is efficient

When comparing two unit trusts with nearly identical returns, the one with the higher Sharpe Ratio is the smarter choice because it achieves that return with lower risk. This is why many fund award winners such as the Lipper Fund Awards are judged not only on returns, but also on the consistency of risk-adjusted returns.

Weaknesses & Limitations of the Sharpe Ratio

Useful as it is, the Sharpe Ratio is not a perfect tool. You need to be aware of its limitations:

1. It penalises all volatility, including the positive kind. The Sharpe Ratio treats upside swings (surging profits) as "risk" the same way it treats downside swings (losses). Yet most investors do not mind if their portfolio spikes upward. This is the metric's main weakness.

2. It assumes a normal distribution. The formula assumes returns follow a normal distribution (a bell curve). In reality, financial markets frequently experience extreme moves (black swans) more often than a normal distribution would predict.

3. It is sensitive to the time period. A Sharpe Ratio calculated from one year of data can differ greatly from five years of data. Short periods can give a misleading picture.

4. It can be manipulated. Certain strategies such as selling options can produce an attractive-looking high Sharpe Ratio that actually hides large, rare losses. To understand the real types of risk in the market, read 7 charts that reveal the real risk in the stock market.

Sharpe Ratio vs Sortino vs Treynor

Because of the limitations above, there are several alternative metrics that complement the Sharpe Ratio:

- Sortino Ratio - similar to Sharpe, but only penalises downside volatility (downside risk). Many consider it fairer because investors really only fear losses, not sudden gains.

- Treynor Ratio - uses beta (systematic risk relative to the market) as the risk measure, rather than total standard deviation. Suitable for well-diversified portfolios.

- Information Ratio - measures excess return relative to a benchmark such as the FBM KLCI.

In practice, use the Sharpe Ratio as a starting point, then refer to the Sortino Ratio if you want a more precise picture of downside risk alone. No single metric is perfect - combining several gives a more complete view.

How to Use the Sharpe Ratio for Your Portfolio

Here are practical steps to use the Sharpe Ratio in your own investing:

- Gather return data - record your portfolio's monthly or annual returns including dividends.

- Calculate average return and standard deviation - most broker platforms or spreadsheets can compute standard deviation automatically using the STDEV function.

- Use the current risk-free rate - refer to the latest OPR or treasury bill rate from Bank Negara.

- Compare, do not judge in isolation - a single Sharpe Ratio value does not mean much. Compare it with a benchmark such as the FBM KLCI, or with your alternative portfolios.

- Review periodically - recalculate each quarter or year to monitor whether your strategy remains efficient.

Remember, the Sharpe Ratio is a decision-making tool, not a forecast. It tells you past risk-adjusted performance, but does not guarantee future performance. Use it alongside fundamental analysis and a thorough understanding of risk. For investors who want to structure a portfolio by risk level appropriate to their age, our guide on building a stock portfolio by age offers a useful framework.

Frequently Asked Questions (FAQ)

1. What is a good Sharpe Ratio?

Generally, a Sharpe Ratio above 1.0 is considered good, above 2.0 very good, and above 3.0 excellent. However, this depends on market context and time period. Compare with an appropriate benchmark before drawing conclusions.

2. Can the Sharpe Ratio be negative?

Yes. A negative Sharpe Ratio means your investment return is lower than the risk-free rate. It shows you are taking risk but not getting a worthwhile reward - you would be better off in a risk-free instrument.

3. What is the difference between the Sharpe Ratio and the Sortino Ratio?

The Sharpe Ratio penalises all volatility (up and down), while the Sortino Ratio only penalises downside volatility (loss risk). Many investors consider Sortino fairer because sudden gains are not real "risk".

4. What is the risk-free rate for Malaysian investors?

The common proxy is the short-term Malaysian treasury bill rate or Bank Negara's OPR. As of 2026, the OPR stands at 2.75% and short-term treasury bills hover around 3%. You can use around 3% as a reasonable estimate.

5. Can I calculate the Sharpe Ratio for a single stock?

Yes. The Sharpe Ratio can be calculated for individual stocks, ETFs, unit trusts, or an entire portfolio. However, for individual stocks the standard deviation is usually high, so the Sharpe Ratio tends to be lower than a diversified portfolio.

6. Does a high Sharpe Ratio always mean a safe investment?

Not necessarily. A consistently very high Sharpe Ratio can hide large but rare tail risk. Always understand the strategy behind the number.

7. Where can I get standard deviation data for the calculation?

Many broker platforms, unit trust fact sheets, and finance websites provide this data. You can also calculate it yourself by recording periodic returns in Excel and using the STDEV function.

Conclusion

The Sharpe Ratio teaches a fundamental lesson investors often forget: a high return means nothing if you have to bear disproportionate risk to achieve it. By turning the question of "is it worth it" into a single comparable number, this metric helps you make smarter, more rational investment decisions.

While it is not a perfect tool, the Sharpe Ratio remains a very useful starting point for fairly evaluating the performance of any investment. Use it alongside other metrics such as the Sortino Ratio, and always understand the context behind the number.

Understanding metrics like the Sharpe Ratio is an important step toward becoming a more mature and disciplined investor. But knowledge alone is not enough - you need the right platform to start investing and to measure your portfolio's real performance.

To start investing on Bursa Malaysia as well as foreign markets such as the US and Hong Kong, you can open a CDS and trading account with us through a simple, fully supported process.

If you are still new and want to understand the basics of stock investing from scratch, get our free stock investing basics ebook as a starting point.

Further Reading

- How to Measure Your Own Portfolio Performance: 5 Basic Metrics

- The PEG Ratio: How to Spot Cheap Growth Stocks on Bursa Malaysia

- How Many Stocks Should Be in a Portfolio? Optimal Size & 'Diworsification' Risk

- Defensive vs Growth Stocks: Why a Smart Portfolio Needs Both

- Stock Portfolio by Age: Structuring Investments in Your 20s, 30s & 40s