How ASB Dividends Are Calculated: Complete Formula, Examples & Latest Rates

Every year-end, millions of Amanah Saham Bumiputera (ASB) unitholders wonder — how much dividend will they actually receive? Many know the dividend rate is announced by ASNB, but few understand how the actual calculation works behind the scenes. This article breaks down the ASB dividend calculation formula in detail, complete with practical examples so you can estimate your own ASB investment returns.

Quick Answer

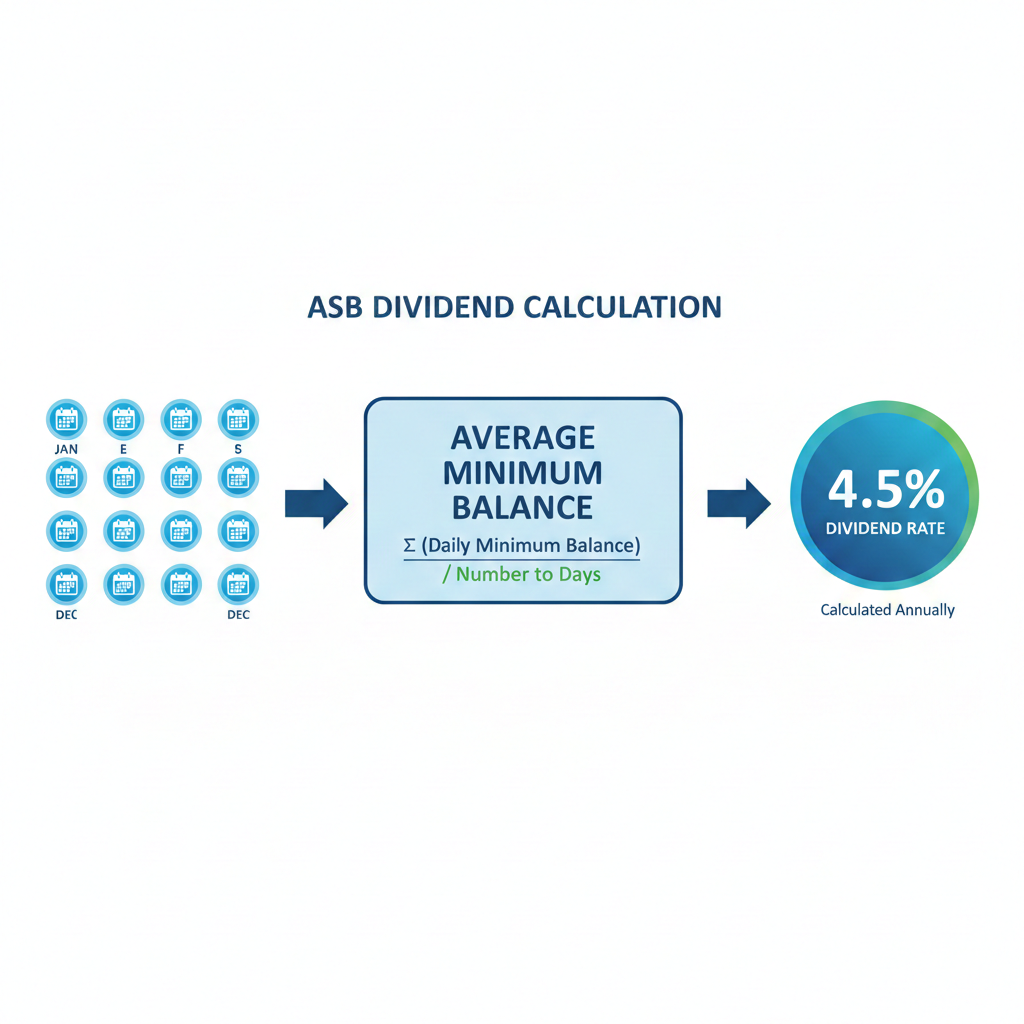

ASB dividends are calculated based on the average minimum monthly balance across 12 months. ASNB takes the lowest balance recorded in your account each month, sums up all 12 months, divides by 12, and multiplies by the declared dividend rate. The more consistently you maintain a high balance without withdrawals, the higher your dividend.

What Is an ASB Dividend?

ASB dividends actually consist of two main components that many investors confuse:

1. Income Distribution (Dividend) — this is the return from ASB's investment portfolio managed by Permodalan Nasional Berhad (PNB). The ASB portfolio includes stocks listed on Bursa Malaysia, government bonds, and money market instruments.

2. Bonus — an additional distribution given by ASNB as a reward to unitholders. In certain years, there is also a special bonus limited to the first 30,000 units only.

For example, for financial year 2025, PNB announced a total distribution of 5.75 sen per unit — comprising 5.20 sen income distribution and 0.55 sen bonus. ASNB's total distribution in 2025 reached RM15.3 billion, the highest ever recorded.

A major advantage of ASB is that dividends received are fully exempt from income tax — you don't need to declare them in your LHDN e-Filing form.

ASB Dividend Calculation Formula

ASB dividend calculation uses the Minimum Monthly Balance (MMB) method. Here are the detailed steps:

Step 1: Identify the Minimum Monthly Balance (MMB)

MMB is the lowest balance recorded in your ASB account from the 1st to the last day of each month. This means if you withdraw money at any point during a month, the post-withdrawal balance becomes your MMB for that month — even if you deposit the money back later.

Step 2: Calculate the Average Minimum Monthly Balance

Sum up all 12 MMBs (January through December), then divide by 12:

Average MMB = (MMB Jan + MMB Feb + ... + MMB Dec) ÷ 12

Step 3: Multiply by the Dividend Rate

Dividend = Average MMB × Income Distribution Rate

Bonus = Average MMB × Bonus Rate

Total Return = Dividend + Bonus

Important note: For years with a special bonus (limited to the first 30,000 units), the special bonus calculation uses the lesser of the average MMB or 30,000 units.

ASB Dividend Calculation Examples

Let's look at three different scenarios using the 2025 dividend rate (5.20 sen distribution + 0.55 sen bonus = 5.75 sen total):

Example 1: Fixed Balance of RM50,000 (No Withdrawals)

The simplest situation — you keep RM50,000 from January to December without any transactions.

| Month | MMB (RM) |

|---|---|

| Jan–Dec | 50,000 each month |

- Average MMB = (50,000 × 12) ÷ 12 = RM50,000

- Income Distribution = 50,000 × 5.20% = RM2,600

- Bonus = 50,000 × 0.55% = RM275

- Total Dividend = RM2,875

Example 2: Variable Balance (With Deposits & Withdrawals)

A more realistic scenario — Ali starts with RM30,000 and makes several transactions throughout the year:

| Month | Transaction | Ending Balance | MMB (RM) |

|---|---|---|---|

| Jan | None | 30,000 | 30,000 |

| Feb | Deposit RM10,000 (15th) | 40,000 | 30,000 |

| Mar | None | 40,000 | 40,000 |

| Apr | Withdraw RM5,000 (10th) | 35,000 | 35,000 |

| May | None | 35,000 | 35,000 |

| Jun | Deposit RM15,000 (1st) | 50,000 | 50,000 |

| Jul–Dec | None | 50,000 | 50,000 each month |

- Total MMB = 30,000 + 30,000 + 40,000 + 35,000 + 35,000 + 50,000 + (50,000 × 6) = 520,000

- Average MMB = 520,000 ÷ 12 = RM43,333.33

- Income Distribution = 43,333.33 × 5.20% = RM2,253.33

- Bonus = 43,333.33 × 0.55% = RM238.33

- Total Dividend = RM2,491.67

Notice: even though Ali's year-end balance is RM50,000, the dividend received is lower than Example 1 because several months early in the year had lower MMBs. Timing of deposits matters greatly — the earlier you deposit, the higher your dividend.

Example 3: Maximum Investment of RM200,000

The individual ASB investment limit for Bumiputera citizens is RM200,000. If you maintain the maximum balance throughout the year:

- Average MMB = RM200,000

- Income Distribution = 200,000 × 5.20% = RM10,400

- Bonus = 200,000 × 0.55% = RM1,100

- Total Dividend = RM11,500

RM11,500 per year equals approximately RM958 per month in passive income — completely tax-free.

ASB Dividend Rate History (2015–2025)

Understanding ASB dividend trends helps you set realistic expectations. Here is the 11-year record based on data from ASNB:

| Year | Distribution (sen) | Bonus (sen) | Total (sen) |

|---|---|---|---|

| 2025 | 5.20 | 0.55 | 5.75 |

| 2024 | 5.50 | 0.25 | 5.75 |

| 2023 | 4.25 | 1.00 | 5.25 |

| 2022 | 3.35 | 1.25 + 0.50* | 5.10 |

| 2021 | 4.25 | 0.75 | 5.00 |

| 2020 | 3.50 | 0.75 + 0.75* | 5.00 |

| 2019 | 5.00 | 0.50 | 5.50 |

| 2018 | 6.50 | 0.50 | 7.00 |

| 2017 | 7.00 | 0.25 + 1.00* | 8.25 |

| 2016 | 6.75 | 0.50 | 7.25 |

| 2015 | 7.25 | 0.50 | 7.75 |

*Special bonus limited to the first 30,000 units only

ASB dividend rates show a declining trend from the 7–8 sen range in 2015–2018 to 5–5.75 sen in recent years. This reflects changes in stock market performance and PNB's overall investment portfolio. However, the 5.75 sen rate in 2024 and 2025 signals a positive recovery.

Factors Affecting ASB Dividend Rates

Many wonder — why do ASB dividend rates change every year? Here are the main factors:

1. Stock Market Performance — The majority of ASB's portfolio is invested in stocks listed on Bursa Malaysia. When the stock market rises, portfolio returns increase accordingly.

2. Interest Rates & Bonds — Part of ASB's portfolio is invested in government bonds and fixed-income instruments. Changes in Bank Negara Malaysia's OPR rate affect returns from this component.

3. Global & Local Economy — Economic crises like the COVID-19 pandemic (2020–2021) caused dividend rates to drop to the 5.00 sen level.

4. Fund Size — With the total number of ASB units in circulation growing larger, PNB needs to generate higher returns to maintain competitive dividend rates.

5. PNB's Investment Decisions — As the fund manager, PNB makes strategic asset allocation decisions that directly impact overall returns.

5 Tips to Maximize Your ASB Dividends

1. Deposit Money As Early As Possible

Since dividends are calculated based on MMB, money deposited at the beginning of the month gives a higher MMB compared to end-of-month deposits. Ideally, deposit on the 1st of every month.

2. Avoid Mid-Year Withdrawals

Every withdrawal lowers that month's MMB. If you must withdraw, do it at the end of the month (after the 28th) so the MMB for that month remains at the pre-withdrawal balance.

3. Use Auto Debit / myASNB Auto Invest

Set up monthly auto debit through myASNB for consistent investing without having to remember each month. Even RM100 monthly builds discipline and increases your average MMB.

4. Target the Maximum RM200,000 Limit

At a rate of 5.75%, the maximum RM200,000 investment generates RM11,500 per year tax-free. This equals a 5.75% return — far higher than most bank savings accounts offering only 2–3%.

5. Consider ASB Financing (With Caution)

ASB Financing allows you to invest larger amounts through bank loans. However, ensure the spread between the ASB dividend rate and loan interest rate is positive. Understand the risks and do the ASB Financing calculation carefully before deciding.

5 Common Mistakes in ASB Dividend Calculations

1. Using year-end balance to calculate dividends — Many assume the December 31 balance multiplied by the dividend rate gives the answer. In reality, it uses the 12-month average MMB.

2. Not understanding withdrawal impact — Withdrawing RM10,000 on the 5th means that month's MMB drops to the post-withdrawal balance, even if you redeposit the money on the 6th.

3. Forgetting to calculate bonus separately — Income distribution and bonus have different rates. In certain years, the special bonus is also limited to the first 30,000 units.

4. Assuming ASB dividends are guaranteed — ASB dividend rates are not guaranteed and depend on investment performance. While the track record shows consistent returns since 1990, rates change every year.

5. Not accounting for zakat on ASB investments — As Muslims, ASB dividends are subject to zakat. Make sure you calculate and pay zakat on your ASB investments and returns.

FAQ: ASB Dividend Calculation

What is the latest ASB dividend rate?

For financial year 2025, the ASB dividend rate is 5.75 sen per unit — comprising 5.20 sen income distribution and 0.55 sen bonus. This is the highest rate in five years, signalling a recovery in PNB's portfolio performance.

When are ASB dividends credited to accounts?

ASB dividends are automatically credited to unitholders' accounts on January 1 of the following year. You can check via the myASNB portal or mobile app starting midnight on January 1.

Are ASB dividends taxable?

No. ASB dividends are fully exempt from income tax in Malaysia. You do not need to declare them in your LHDN e-Filing tax form.

What is the maximum ASB investment limit?

The individual ASB investment limit is RM200,000 per unit for Bumiputera citizens. There are also ASB accounts for children (under 18) with the same limit.

What is the difference between ASB dividends and stock dividends?

ASB dividends are returns from a unit trust managed by PNB, paid once a year. Stock dividends are paid by companies listed on Bursa Malaysia — usually twice a year — and the rate depends on each company's performance and dividend policy.

Is ASB Shariah-compliant?

ASB is not categorized as a Shariah-compliant fund by the Securities Commission Malaysia. However, the National Fatwa Council has ruled that investing in ASB is permissible (harus) for Muslims.

Can I withdraw ASB money anytime?

Yes, ASB is an open-ended fund that allows withdrawals at any time via ASNB counters, myASNB, or ATMs that support ASB withdrawals. However, remember that withdrawals will affect that month's MMB and consequently your year-end dividend.

What is the difference between ASB and ASB2?

ASB2 (Amanah Saham Bumiputera 2) also has a RM200,000 investment limit, but it is a separate fund with its own dividend rate. For 2025, ASB2's dividend is 5.50 sen per unit. Investors who have reached the ASB limit can continue investing through ASB2.

Conclusion

Calculating ASB dividends is not complicated once you understand the Minimum Monthly Balance (MMB) concept. The key is maintaining a consistent balance, avoiding unnecessary withdrawals, and depositing money as early as possible each month. With a rate of 5.75 sen per unit in 2025, ASB remains one of the most attractive investment instruments for Bumiputera in Malaysia.

Diversify Your Investments, Strengthen Your Portfolio

Beyond ASB, building a diversified investment portfolio including stocks listed on Bursa Malaysia is a wise step to strengthen your long-term finances.

Open a CDS Trading Account today to start investing in Shariah-compliant stocks and build a more comprehensive investment portfolio beyond ASB.

Download the Free Stock Market Basics Ebook to understand stock investment fundamentals from a Malaysian Muslim investor's perspective.