Personal Financial Management in Malaysia: Smart Ways to Manage Your Money

Introduction: Why Personal Financial Management Matters

Malaysian household debt has reached RM1.65 trillion as of March 2025 — equivalent to 84.3% of Gross Domestic Product (GDP). Even more alarming, nearly half of the 35,714 bankruptcy cases recorded since 2019 were caused by personal loans — not housing or car loans, but borrowings that could have been avoided.

These statistics are not just numbers. They represent real stories of Malaysians trapped in a debt cycle due to a lack of money management skills. The good news? Personal financial management is not rocket science. With discipline and the right guidance, anyone can take control of their finances — regardless of how much you earn.

In this article, you will learn 6 practical steps to manage your personal finances effectively, complete with examples using real Malaysian salaries. If you have ever wondered why your paycheck runs out before the end of the month, this guide is for you.

What Is Personal Financial Management?

Personal financial management refers to the process of planning, controlling, and monitoring your money inflows and outflows systematically. It differs from corporate or institutional finance because it focuses on individual and family finances.

The five pillars of personal financial management:

- Income — Maximising your sources of earnings

- Expenses — Controlling spending and reducing waste

- Savings — Saving consistently for the future

- Investments — Growing your money beyond the inflation rate

- Protection — Shielding yourself and your family from financial risks

Many people assume financial management is only for high-income earners. In reality, it is even more important for those with moderate incomes because the margin for error is smaller. A single financial misstep can trigger a domino effect that is hard to recover from.

If you are just starting out, also read the guide on 5 Financial Basics for Individuals as a starting point.

Malaysian Financial Statistics You Need to Know

Before we dive into the practical steps, let us look at the financial reality facing Malaysians based on the latest data:

| Statistic | Figure | Source |

|---|---|---|

| Household debt (March 2025) | RM1.65 trillion (84.3% of GDP) | data.gov.my |

| Household financial assets | RM3.44 trillion (2.1x debt) | Bank Negara Malaysia |

| Bankruptcy cases since 2019 | 35,714 cases | Malaysia Department of Insolvency |

| Main cause of bankruptcy | Personal loans (49.14%) | Department of Insolvency |

| Civil servants bankrupt (2020–2025) | 4,194 cases | Ministry of Finance |

| Median DSR of Malaysians | 34% | Bank Negara Malaysia |

A study by Sun Life Malaysia found that 64% of Malaysians may have to continue working past the age of 60 due to insufficient retirement savings.

However, there is good news — Malaysian household financial assets are actually 2.1 times greater than debt. This means that overall, Malaysians have solid financial capacity. The problem is not a lack of money, but a lack of management.

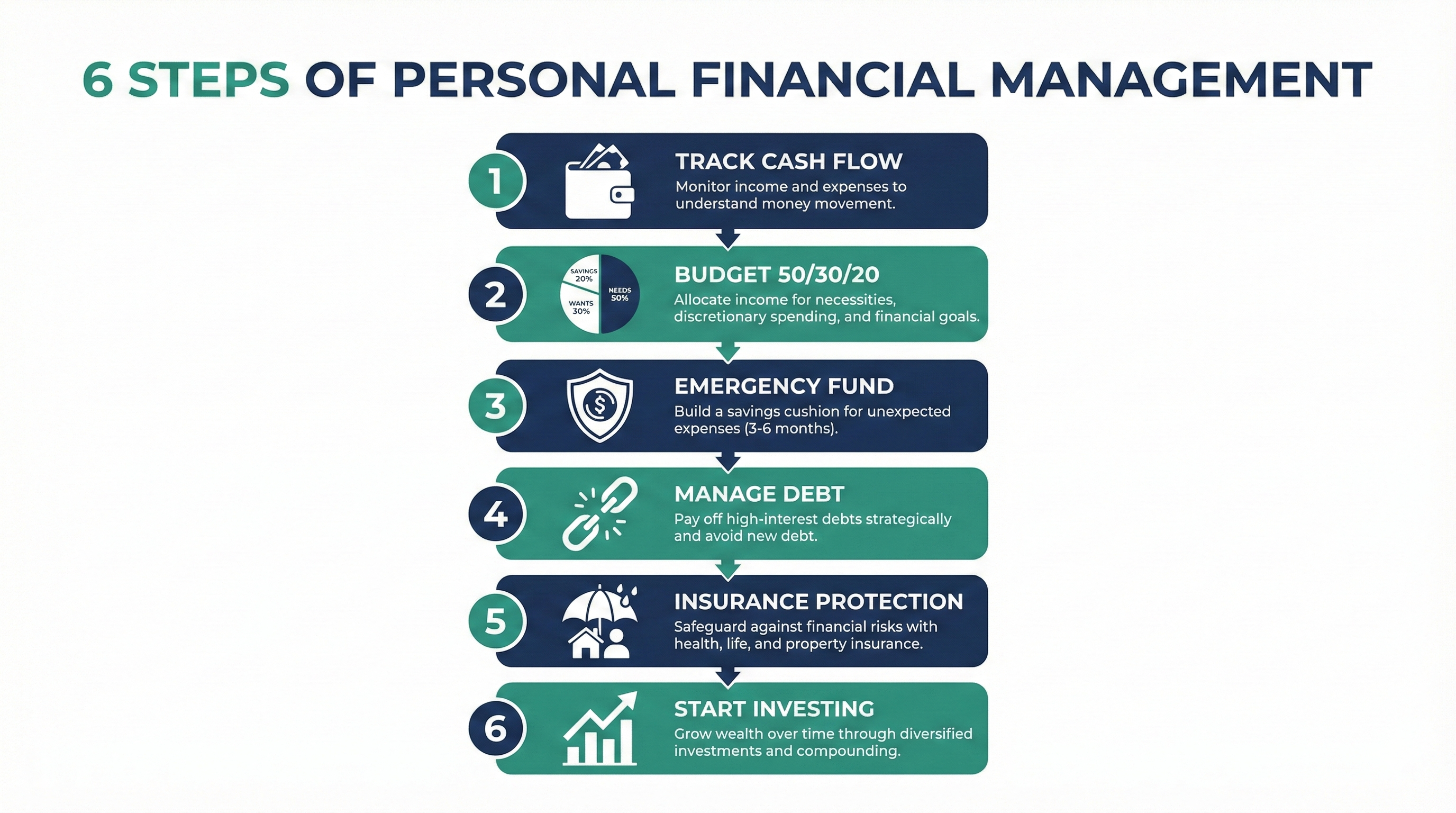

Step 1: Know Your Cash Flow

The first and most important step in personal financial management is understanding where your money goes. Many people know how much they earn but have no idea exactly how much they spend each month.

How to Track Your Cash Flow

- Record all income — net salary (after KWSP/EPF, SOCSO, and PCB deductions), side income, dividends

- Record all expenses — rent/mortgage, car payments, food, utilities, subscriptions, entertainment

- Categorise expenses into 3 groups:

- Needs: rent, food, transport, utility bills, insurance

- Wants: dining out, entertainment, shopping, streaming subscriptions

- Savings & Debt: emergency fund, ASB, extra debt repayments

Tools You Can Use

- Spreadsheet (Google Sheets / Excel) — free and customisable

- Finance apps: BigPay, Money Lover, Wallet by BudgetBakers

- Manual method: a small notebook or phone notes

Spend 1–2 months tracking your expenses without changing your habits. After that, you will clearly see where money leaks are occurring — forgotten subscriptions, RM15 coffees every day, or dining out that could be reduced.

Step 2: Build a Monthly Budget — The 50/30/20 Method

Once you know where your money goes, it is time to plan where your money should go. The most popular method, recommended by KWSP/EPF itself, is the 50/30/20 rule.

The 50/30/20 Breakdown

| Category | Percentage | Example (Salary RM4,500) |

|---|---|---|

| Needs | 50% | RM2,250 |

| Wants | 30% | RM1,350 |

| Savings & Debt Repayment | 20% | RM900 |

Practical Examples by Salary

Salary RM3,000 (net):

- Needs: RM1,500 (rent RM700, food RM400, transport RM200, utilities RM200)

- Wants: RM900 (dining out RM300, entertainment RM200, shopping RM200, miscellaneous RM200)

- Savings: RM600 (ASB RM300, emergency fund RM300)

Salary RM6,000 (net):

- Needs: RM3,000 (mortgage RM1,200, car RM600, food RM500, utilities RM300, insurance RM400)

- Wants: RM1,800 (dining out RM500, entertainment RM400, travel fund RM400, gym RM200, miscellaneous RM300)

- Savings: RM1,200 (ASB RM500, stocks RM400, emergency fund RM300)

The Reality in Malaysia

Admittedly, for those living in Kuala Lumpur or Penang, rent alone can sometimes exceed 40% of income. In such cases, you may need to adjust to a 60/20/20 or 70/20/10 split temporarily, while working on increasing your income or finding lower-cost alternatives.

What matters is not hitting the exact percentages, but saving consistently — even if it is only RM100 a month.

Step 3: Build an Emergency Fund

An emergency fund is the most important financial safety cushion in personal financial management. AKPK (Credit Counselling and Debt Management Agency) recommends that every individual have an emergency fund equal to 3 to 6 months of monthly expenses.

Why Is an Emergency Fund Important?

- Sudden job loss

- Medical emergencies not covered by insurance

- Vehicle or home repairs

- Avoiding the need to take out personal loans (the leading cause of bankruptcy!)

How Much Should You Save?

| Monthly Expenses | Emergency Fund (3 months) | Emergency Fund (6 months) |

|---|---|---|

| RM2,000 | RM6,000 | RM12,000 |

| RM3,500 | RM10,500 | RM21,000 |

| RM5,000 | RM15,000 | RM30,000 |

Where Should You Keep Your Emergency Fund?

An emergency fund should be easily accessible but not so easy to reach that you are tempted to dip into it. Best options:

- ASB — dividend returns of 5–6%, withdrawable at any time

- Tabung Haji — for Muslims, hibah returns of 3–4%, easily accessible

- High-yield savings accounts — such as digital bank accounts (e.g., GX Bank, Boost Bank)

For a detailed comparison of savings instruments, read Tabung Haji vs ASB: Which Is More Profitable for Long-Term Savings?

Step 4: Manage and Reduce Debt

If you have debt beyond your mortgage and car loan, this step is critical. High-interest debt such as credit cards (15–18% per year) and personal loans (6–12%) can destroy your savings efforts.

Two Popular Strategies to Eliminate Debt

1. Snowball Method (Smallest to largest)

- Pay off the smallest debt first, then redirect payments to the next one

- Advantage: psychological motivation — you see progress quickly

- Example: Credit card RM500 → Personal loan RM5,000 → Car RM30,000

2. Avalanche Method (Highest interest to lowest)

- Pay off the debt with the highest interest rate first

- Advantage: saves more money mathematically

- Example: Credit card 18% → Personal loan 8% → Car 3.5%

Debt Service Ratio (DSR)

Bank Negara Malaysia uses the Debt Service Ratio to measure your debt burden. Your DSR is calculated as:

DSR = (Total monthly debt payments / Gross monthly income) × 100%

- DSR below 40%: Healthy

- DSR 40–60%: Caution

- DSR above 60%: Dangerous — you may need AKPK assistance

AKPK Assistance — It Is Free!

If you are facing serious debt problems, AKPK provides free services including:

- One-on-one financial counselling

- Debt Management Programme (DMP) — restructuring repayments with banks

- Financial education workshops

Contact AKPK at 03-2616 7766 or visit www.akpk.org.my.

Step 5: Protect Yourself with Insurance and Takaful

Many people jump straight into investing without having adequate protection. This is like building a house without a roof — when it rains (disaster strikes), everything is destroyed.

Minimum Protection You Need

- Medical Takaful/Insurance (Medical Card) — The MOST important. A single ICU treatment can cost RM50,000–RM100,000.

- Life Takaful — Protection for your family in the event of death or total permanent disability.

- Personal Accident (PA) Coverage — More affordable and covers you against accidents.

How Much Should You Allocate?

Allocate 5–10% of your salary for protection. For a monthly income of RM4,000, this means RM200–RM400 for takaful/insurance premiums.

Make sure you have adequate protection before you start investing. The logic is simple — investments can lose value, but if you fall ill without protection, you not only lose your investments but may also be forced into debt.

Step 6: Start Investing for the Future

Once you have a controlled budget, a sufficient emergency fund, manageable debt, and adequate protection — only then is it time to grow your money through investments.

Investment Pyramid for Malaysians

Level 1: Foundation (Mandatory)

- KWSP/EPF — Mandatory contribution of 11% (employee) + 12–13% (employer). EPF recorded a dividend return of 6.30% for 2024 and manages RM1.37 trillion in assets for over 15 million members.

- Make sure you do not make unwise lump-sum withdrawals

Level 2: Structured Savings

- ASB — Returns of 5–6%, suitable for both Muslims and non-Muslims

- Tabung Haji — Hibah returns of 3–4%, exclusively for Muslims

- Read the full comparison: KWSP/EPF vs ASB vs Tabung Haji Dividend Comparison 2026

Level 3: Active Investing

- Bursa Malaysia stocks — Open a CDS account and start investing in equities

- Unit Trusts / ETFs — For those who want diversified investments without daily monitoring

- Global stocks — Diversify into US, Hong Kong, and other markets

To start investing in stocks, the first step is to open a CDS account through Mplus. You can also consider an ASB Financing strategy to leverage your savings.

Common Financial Management Mistakes You Must Avoid

Even if you already know the right steps, there are several traps that frequently ensnare Malaysians:

1. No Budget at All

Living without a budget means you are hoping your money will be enough — not planning for it to be enough. That is a huge difference.

2. Lifestyle Inflation

When your salary increases, your spending rises at the same rate (or higher). Every pay raise should increase your savings, not add new financial commitments.

3. No Emergency Fund

Without a financial cushion, a single unexpected event can force you to take out a personal loan — the leading cause of bankruptcy in Malaysia.

4. Investing Without Protection

Buying stocks before having a medical card is a costly mistake. Stocks can wait; your health cannot.

5. Falling for Fake Investment Schemes

Be wary of high returns with no risk offers on social media. Read our guide on non-existent investments on Facebook and Telegram in Malaysia to protect yourself.

6. Not Tracking Expenses

You cannot manage what you do not measure. Without tracking, every budgeting effort will fail.

FAQ: Personal Financial Management

What percentage of my salary should I save each month?

A minimum of 20% according to the 50/30/20 rule. However, if you are just starting out and have debt, begin with 10% and increase gradually. What matters most is consistency, not the amount.

What is the difference between savings and investments?

Savings (ASB, Tabung Haji, bank accounts) carry low risk and offer stable but limited returns. Investments (stocks, unit trusts, property) carry higher risk but offer greater return potential. Both are essential for balanced financial management.

How do I start if my salary is only RM2,000?

Start by tracking your expenses for a month. Identify 2–3 items you can cut back on. Set up automatic savings of even RM50 a month. Increase the amount gradually as your income grows.

What is AKPK and how can it help?

AKPK (Credit Counselling and Debt Management Agency) was established by Bank Negara Malaysia to help individuals facing financial difficulties. Their services are free, including financial counselling, the Debt Management Programme (DMP), and educational workshops.

How long does it take to build an emergency fund?

It depends on your income and expenses. If you save RM500 a month with a target of RM15,000, it takes 30 months (2.5 years). Start from where you are now — your first RM1,000 already makes a significant difference.

Should I pay off debt first or start investing?

If your debt carries a high interest rate (credit card 18%, personal loan 8%+), the priority is paying off debt because no investment consistently returns 18% per year. For low-interest debt (mortgage 3–4%, car 3%), you can invest in parallel.

Do I need to hire a financial planner?

To start with, you can learn on your own through free resources such as AKPK and KWSP/EPF. If your income exceeds RM10,000 or you have a complex financial situation (business, estate, large investments), a licensed financial planner can help optimise your strategy.

What is the Debt Service Ratio (DSR) and why does it matter?

DSR measures the percentage of your income used to repay debt. A DSR below 40% is considered healthy. If your DSR exceeds 60%, you are at high risk and should urgently reduce debt or increase your income.

Conclusion

Personal financial management is not about being stingy or denying yourself the enjoyment of life. It is about making conscious choices so that money works for you, not the other way around. With the 6 steps discussed — from tracking cash flow to starting investments — you now have a complete framework to take control of your finances in 2026 and beyond.

If you are ready to take the next step in your financial journey, start by building a solid investment portfolio. Open your CDS trading account through this link to begin investing on Bursa Malaysia — the first step towards financial freedom. Also download the Free Stock Market Basics Ebook to understand the fundamentals of stock investing before you begin.