Prospect Theory: Why You Cut Winners Short but Let Losers Run

You buy a stock at RM1.00. It climbs to RM1.20 and your heart races. "I'm up RM2,000 already, better sell before it disappears." You sell, relieved. Meanwhile another stock you bought at RM1.00 drops to RM0.70, and you hold. RM0.50, still holding. RM0.30, "never mind, it'll bounce back." Eventually it becomes a permanent bagholder position.

If that scenario feels uncomfortably familiar, you are not alone. Almost every investor and trader on Bursa Malaysia runs through the same cycle: cut profits quickly, hold losses forever. What is fascinating is that this is not purely a discipline problem. It is a product of how the human brain is wired to evaluate gains and losses. The concept that explains it is called Prospect Theory, and it won the Nobel Prize in Economics.

Quick Answer: Why Do We Cut Winners but Hold Losers?

We cut profits quickly and hold losses too long because the human brain does not evaluate gains and losses symmetrically. According to Prospect Theory, introduced by Daniel Kahneman and Amos Tversky, the pain of losing RM1,000 is felt roughly twice as strongly as the pleasure of gaining RM1,000. As a result, when we are winning we become risk-averse (quick to lock in), but when we are losing we become risk-seeking (willing to "gamble" on a recovery). This pattern is known in behavioral finance as the disposition effect.

What Is Prospect Theory?

Prospect Theory is a theory of decision-making under uncertainty, formulated by psychologists Daniel Kahneman and Amos Tversky in 1979 in the journal Econometrica. This work later earned Kahneman the Nobel Prize in Economics in 2002 (Tversky had passed away before then).

Before this theory existed, classical economics assumed humans were rational agents who made decisions based on final wealth levels. In that idealized world, it should not matter whether your stock rose from RM1.00 or fell from RM1.50 - all that matters is its value now. But Kahneman and Tversky proved that humans do not think that way. We evaluate things based on changes from a reference point, not absolute value. And we react to gains and losses in dramatically different ways.

The Three Pillars of Prospect Theory

To understand why your portfolio becomes a victim, we need to grasp three core ideas:

- Reference point - We do not evaluate a stock price in absolute terms. We compare it to our purchase price. A stock at RM1.20 feels like a "gain" if you bought at RM1.00, but feels like a "painful loss" if you bought at RM2.00. Same price, opposite feelings.

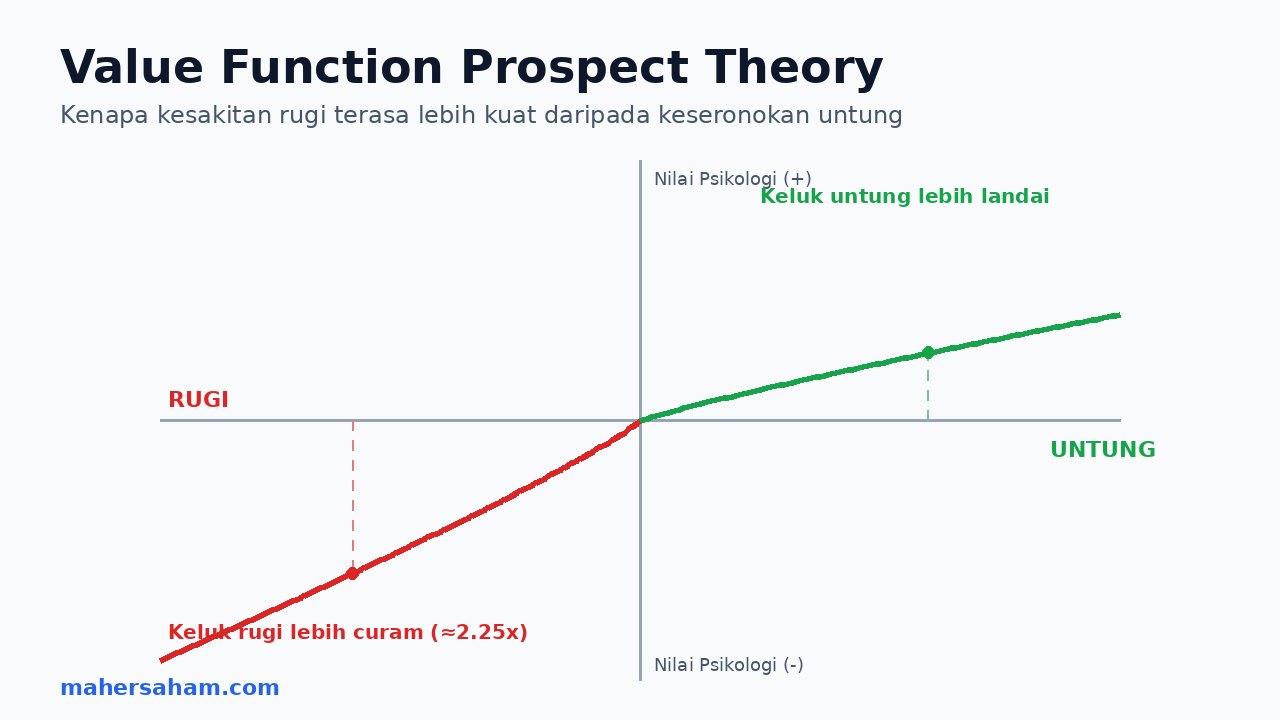

- Loss aversion - This is the most important pillar. Empirical studies estimate the loss aversion parameter at roughly 2.25, meaning the pain of a loss is felt about 2.25 times more intensely than the pleasure of an equivalent gain.

- Diminishing sensitivity - The difference between losing RM0 and RM1,000 feels huge, but the difference between losing RM9,000 and RM10,000 feels small. This is what makes people willing to "add more" to a losing position.

The combination of these three elements produces an S-shaped graph called the value function - concave in the gains region and convex in the losses region. This shape is the root of everything.

Why Do You Cut Profits Early?

When your stock rises, you are in the "gains" region of the value function. In this region the curve is concave - meaning each additional ringgit of profit delivers diminishing satisfaction. The first RM1,000 of profit feels great, but the next RM1,000 feels less sweet.

The effect is that your brain becomes risk-averse when ahead. You prefer the "certainty" of locking in RM2,000 now over the "risk" of waiting for it to become RM4,000 but possibly returning to zero. In financial mathematics, this move is usually a mistake - you are cutting a winner that should have been left to run. But emotionally, it feels smart and safe.

This is why the old trader's adage "cut your losses, let your profits run" is so hard to practice. It fights the brain's natural tendency. Our instinct does the opposite - cut profits, let losses run.

Why Do You Hold Losses Forever?

Now imagine your stock falls. You are in the "losses" region of the graph. Here the curve is convex, and this completely flips how you assess risk. You become risk-seeking when losing.

Why? Because selling at a loss means you turn that loss into reality. As long as you hold, it is only a "paper loss" and your brain can still hope. The choice between "a certain RM3,000 loss now" and "a possible RM0 loss if it recovers" pushes the brain to gamble - even when, objectively, the stock may never recover.

On top of that, because of loss aversion, the pain of realizing that loss feels twice as sharp. So your brain makes the easy call: avoid the pain, do not sell, just hope. This is not laziness or stupidity. It is an automatic psychological defense. Unfortunately, it is also the fastest way to turn a small loss into a big one.

The Disposition Effect: Scientific Evidence from Real Data

This theory is not just an idea on paper. In 1998, finance professor Terrance Odean analyzed the trading records of 10,000 investor accounts at a discount brokerage. His study, "Are Investors Reluctant to Realize Their Losses?", became one of the strongest pieces of evidence for this phenomenon.

Odean found that investors showed a strong tendency to sell winning stocks faster than losing stocks. This is what is called the disposition effect. The most striking part: the stocks they sold for a gain actually outperformed the stocks they held at a loss by roughly 3.4% over the following year.

In other words, the average investor's instinct is backwards. They sell the stocks they should hold, and hold the stocks they should sell. This is not bad luck - it is a consistent pattern across thousands of accounts, driven by the same psychology that Prospect Theory describes.

A Real Example on Bursa Malaysia

Imagine Encik Azman, an ordinary retail investor. He owns two stocks:

- Stock A: bought at RM1.00, rises to RM1.15. He sells for a 15% gain. "Thank goodness, better than losing it." Three months later Stock A is at RM1.80.

- Stock B: bought at RM2.00, falls to RM1.60. "I haven't sold, so I haven't lost." It drops to RM1.20, he averages down and buys more. It falls to RM0.80. Eventually he is stuck for three years.

Encik Azman is not stupid. He is a victim of his own brain. He locked in a small winner (Stock A) and defended a big loser (Stock B). This is the disposition effect in action, and it happens every day in CDS accounts across Malaysia. The same pattern is discussed in our article on the 7 mental biases that make investors lose money on Bursa Malaysia.

The Real Cost to Your Portfolio

Why is this pattern so damaging? A few reasons:

- The mathematical asymmetry of losses: a stock that falls 50% needs to rise 100% just to break even. The longer you hold a loss, the more impossible recovery becomes. This is why the risk management and psychological discipline that many traders ignore matters so much.

- Dead capital: money trapped in a losing stock cannot work for you. It is a large opportunity cost.

- Winners cut too early: true multibaggers - stocks that rise 5x or 10x - are impossible to capture if you sell every time you are up 15%.

- An exhausting emotional cycle: holding a long-running loss erodes confidence and can lead to desperate decisions (panic selling at the absolute bottom).

Why Even Experienced Traders Are Not Immune

Many people assume loss aversion only attacks beginners. The reality is that it is an automatic feature of the brain - not a knowledge gap. Institutional traders and professional fund managers are exposed too; they simply usually have systems and discipline that force them to act against instinct. That is the difference: it is not that they feel no pain cutting a loss, but that they have rules they obey without negotiation.

Loss aversion is also rooted in evolution. Our ancestors who were more sensitive to danger and loss were more likely to survive. The same brain that once protected us from predators now makes it hard to press the "sell at a loss" button. Understanding that this is natural wiring, not a personal weakness, helps you stop blaming yourself and start building a system. The same concept is highlighted in our piece on the 13 emotional traps that can destroy a portfolio - nearly all of them stem from how the brain values gains and losses.

How to Fight Prospect Theory in Investing

You cannot "delete" loss aversion from your brain - it is part of being human. But you can build a system that protects you from yourself. Here are six practical strategies:

1. Set a Stop Loss Before You Buy

Decide your exit level (for example -8% or -15%) before you enter, while your emotions are still neutral. When it triggers, exit without negotiating with yourself. A stop loss takes the decision out of the hands of your emotional brain.

2. Write Rules, Don't Rely on Feelings

"I will sell if the fundamentals break or the price drops below my stop loss" is far stronger than "I feel like I should wait a bit." Written rules are not subject to momentary loss aversion.

3. Reframe Your Reference Point

Stop treating your purchase price as the reference point. Ask yourself daily: "If I did not own this stock today, would I buy it at the current price?" If the answer is no, why are you still holding? This question breaks the emotional bond with your purchase price.

4. Get Position Sizing Right

Loss aversion becomes most vicious when a position is too large relative to the portfolio. If a single stock is only 3-5% of your portfolio, its loss will not trigger paralyzing panic. Sensible position sizing softens the emotional reaction.

5. Keep a Trading Journal

Record every buy and sell decision along with the reason. After a few months, you will see your own patterns in black and white - how often you cut profits early, how often you held losses too long. Awareness is the first step to change.

6. Automate What You Can

Use good-till-cancelled orders or price alerts so that exit decisions happen mechanically, rather than depending on your courage at the critical moment. The less the emotional brain is involved, the better. This discipline is closely tied to how you change the way you think, not just your technique.

Agencies such as InvestSmart by the Securities Commission Malaysia also emphasize emotional discipline and risk management as the foundation of healthy investing.

Frequently Asked Questions (FAQ)

What is Prospect Theory in simple terms?

Prospect Theory is a behavioral finance theory explaining that humans evaluate gains and losses asymmetrically - the pain of a loss feels stronger than the pleasure of an equivalent gain. It was introduced by Kahneman and Tversky in 1979 and won the Nobel Prize.

What is the difference between Prospect Theory and loss aversion?

Loss aversion is one component of Prospect Theory. Loss aversion refers specifically to the fact that losses feel more painful than equivalent gains. Prospect Theory is the broader framework that includes loss aversion, the reference point, and diminishing sensitivity.

Why do I feel more pain when I lose than joy when I win?

Because the human brain is wired with loss aversion. Studies estimate we feel the pain of a loss roughly 2 to 2.25 times more strongly than the pleasure of an equivalent gain. This is an evolutionary trait - ancestors who feared danger more were more likely to survive.

How do I avoid cutting profits too early?

Use a trailing stop (a stop loss that moves up with the price) so winners are allowed to run while the uptrend holds, but you stay protected if it reverses. Avoid selling just because you are "in profit" without a technical or fundamental reason.

Is holding a loss always wrong?

Not necessarily. If the company's fundamentals are still strong and your investment thesis still holds, holding a temporarily declining stock can be reasonable. What is wrong is holding solely because you do not want to admit a loss - without re-checking whether the original thesis is still true.

What is the disposition effect?

The disposition effect is the tendency of investors to sell winning stocks too quickly and hold losing stocks too long. It is the practical manifestation of Prospect Theory in stock markets, empirically demonstrated by Terrance Odean's 1998 study.

Can I truly overcome loss aversion?

You cannot erase it entirely, but you can manage it. With systems (stop losses, written rules, position sizing, journaling), you remove key decisions from the grip of momentary emotion. The goal is not to become a feelingless robot, but to stop letting feelings make your trading decisions for you.

Conclusion

Your tendency to cut profits early and hold losses forever is not a personal flaw - it is the result of how the human brain is wired to hate losses more than it loves gains. Prospect Theory gives a name and a structure to the feeling you experience every time your hand trembles over the sell button. Understanding the theory is the first step; building a system that fights this instinct is what separates successful investors from chronic bagholders.

To invest with discipline, you need a platform that lets you act on your system, not your emotions.

Open a CDS account with us to start investing in Bursa Malaysia as well as foreign markets such as the US and Hong Kong, with full access to professional trading tools.

Also grab our free Stock Market Basics Ebook to build a solid investing foundation before you go further.

Further Reading

- Investor Psychology: 7 Mental Biases That Make You Lose Money on Bursa Malaysia

- Investing Psychology: 13 Emotional Traps That Can Destroy Your Portfolio

- Trader Psychology: The Secret Weapon Many Intraday Traders Ignore

- It's Not Your Technique That's Wrong, It's the Way You Think

- Reminiscences of a Stock Operator: Jesse Livermore's Lessons in the Psychology of Speculation