ChatGPT, Claude & Gemini Are Losing Billions - What Is the Real Endgame of AI Companies?

OpenAI is projected to lose $14 billion in 2026 alone. Anthropic remains cash-flow negative despite hitting $19 billion in annualized revenue. Google plans to spend nearly $185 billion on AI infrastructure. The question is simple - why are these tech giants willing to burn billions without turning a profit?

The short answer: they're betting that whoever controls AI today will control the digital economy of the future. This isn't just about chatbot products - it's a race to become the foundational platform for virtually every industry on earth.

In this article, we'll break down exactly how much they're losing, where the money goes, what their long-term strategies are, and most importantly - what all of this means for you as an investor.

How Much Are AI Companies Actually Losing?

Before we discuss strategy, we need to understand the scale of losses happening right now. These aren't speculations - they come from financial reports and the companies' own internal projections.

OpenAI (ChatGPT)

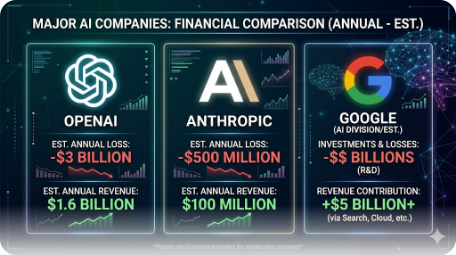

OpenAI is the poster child for massive losses in the AI industry. According to The Information, the company is projected to lose $14 billion in 2026 - nearly triple the early estimates for 2025. Cumulatively from 2023 through end of 2028, OpenAI itself projects total losses of $44 billion.

Strikingly, only 5% of ChatGPT's 800 million users actually pay for a subscription. That means 95% of users access the service for free - while OpenAI bears the compute cost for every single query.

OpenAI's annual revenue is impressive, reaching $20 billion ARR (Annual Recurring Revenue) in 2025. But it still falls far short when infrastructure, research, and model training costs keep skyrocketing.

Anthropic (Claude)

Anthropic, the company behind Claude, sits in a slightly different position. According to Sacra and Reuters, their annualized revenue hit $19 billion as of March 2026, with projections of $26 billion for full-year 2026. That's 10x annual growth sustained for three consecutive years.

However, Anthropic remains cash-flow negative. Their 2026 spending is estimated at $12 billion for model training and $7 billion for inference (running models for users) - totaling $19 billion in expenditure against roughly equal revenue. The company expects to reach positive cash flow by 2027.

Google (Gemini)

Google is playing an entirely different game. Parent company Alphabet plans to spend between $175 billion and $185 billion in capital expenditure (capex) in 2026 - nearly double the $91.4 billion spent in 2025.

The difference from OpenAI and Anthropic? Google Cloud is already profitable. Google Cloud's operating income surged 154% year-over-year to $5.3 billion, with a 30% segment margin. Google also managed to reduce Gemini serving costs by 78% throughout 2025 through model optimization.

In other words, Google isn't "losing" because their business model is broken - they're deliberately investing massively to dominate AI infrastructure for the future.

Where Does All This Money Go?

Many wonder - if you're losing $14 billion a year, where does all that money go? There are four main components.

1. Data Centers and Compute Infrastructure

This is the biggest cost. Training AI models requires tens of thousands of Nvidia H100 and H200 GPUs, each costing tens of thousands of dollars. OpenAI alone has committed to $1.4 trillion in infrastructure spending over the next eight years.

Industry-wide, AI companies are expected to spend $690 billion in capital expenditure in 2026 - an amount roughly equivalent to Thailand's entire GDP.

2. Research and Model Training

Every time a company trains a next-generation model (like GPT-5, Claude 4, or Gemini 3), costs can reach hundreds of millions to billions of dollars. This process requires intensive compute for weeks or months.

And it's not a one-off - each new generation needs to be trained from scratch, with more data and more complex architectures.

3. Researcher and Engineer Salaries

Competition for AI talent is among the fiercest in tech history. Annual compensation for senior AI researchers can reach $1 million to $5 million, including bonuses and equity. Even regular engineers at OpenAI are paid several times more than engineers at traditional tech companies.

Interestingly, engineers at OpenAI are eight times more likely to leave for Anthropic than the reverse - showing just how intense this talent war has become.

4. User Subsidies (Compute for Free Users)

Every time you ask ChatGPT, Claude, or Gemini a question for free, that company bears the compute cost. With hundreds of millions of active users, these costs accumulate to billions.

Analysis shows OpenAI spends roughly $3.30 for every $1.00 it generates - meaning they lose $2.30 every time even a paying user uses the service, let alone free users.

Why Accept Losses? 5 Endgame Strategies of AI Companies

With losses this massive, why do investors keep pouring money in? Why don't these companies just shut down? The answer lies in long-term strategies far bigger than chatbots.

1. The Platform Monopoly Race

The most obvious strategy is what's called the "platform play" - just as Windows dominated PCs, Android dominated phones, and AWS dominated cloud. Whoever becomes the primary AI platform will collect revenue from every company and individual using AI.

OpenAI is openly targeting monopoly status. Sam Altman has even partnered with former Apple designer Jony Ive in a $6.5 billion deal to build a physical AI device - as if trying to build an Apple-like ecosystem, but for AI.

As we previously explored in our article on AI Value Chain, the model and application layers are the parts of the chain with the greatest profit potential if they successfully dominate the market.

2. User and Enterprise Lock-in

When an organization builds internal systems on top of ChatGPT or Claude APIs, the cost of switching to another platform (switching cost) becomes extremely high. Data, workflows, and integrations are all tied together.

This strategy mirrors how Microsoft Office dominated offices for decades - not because it was cheapest, but because the cost of switching was too high.

OpenAI projects 50% of future revenue from ChatGPT, 20% from selling models to developers via APIs, and another 20% from other products. This combination creates an ecosystem that's hard to leave.

3. The Path to AGI (Artificial General Intelligence)

OpenAI explicitly positions AGI - AI that matches or exceeds human capability in virtually all intellectual tasks - as its primary goal. If AGI is achieved, its economic value would be almost impossible to calculate.

Imagine a system that could replace consultants, lawyers, doctors, software engineers, and financial analysts simultaneously. The company that owns such technology would possess economic power never before seen in history.

This isn't mere fantasy. OpenAI needs to either achieve AGI or conduct an IPO in 2026 as a condition of their $110 billion financing agreement.

4. Outcome-Based Pricing

The AI industry is shifting from fixed subscription models (like $20/month for ChatGPT Plus) to outcome-based pricing. This means AI companies will charge based on work completed, problems solved, and results delivered.

For example, if AI can replace a consultant charging $500 per hour, an AI company could charge $50 per hour for the same results - 10 times cheaper for the customer, but with far higher profit margins than a $20/month subscription.

This transition is expected to fully materialize by 2027-2028, as the era of free and heavily subsidized AI services comes to an end.

5. Vertical Industry Domination

Beyond horizontal platforms (general chatbots), AI companies are also targeting vertical industries - healthcare, law, finance, education, and manufacturing. Each of these industries is worth trillions of dollars.

Google has a unique advantage here because they already have a complete ecosystem - Search, YouTube, Android, Gmail, Google Cloud, Google Maps. Gemini can be integrated into all these platforms, making AI part of daily life without users needing to "go to a chatbot."

Who Will Win? Comparing Strategic Positions

Not all AI companies are in the same position. Let's compare their survival odds.

OpenAI - Highest Risk But Most Aggressive

Strengths: Strongest brand recognition, largest user base (800 million), first-mover advantage.

Weaknesses: Largest losses ($14B/year), no other business to support operations, 100% dependent on investor funding. ChatGPT's web traffic share dropped from 86.7% in January 2025 to 64.5% in January 2026. Top employees leaving the company, including CTO Mira Murati.

Risk: If revenue doesn't grow as projected, OpenAI could run out of cash by mid-2027.

Anthropic (Claude) - Most Balanced

Strengths: Fastest revenue growth (10x/year), focus on AI safety attracting enterprise customers, positive cash flow expected by 2027.

Weaknesses: Still dependent on external funding (Amazon, Google as major investors), geopolitical issues (labeled a "supply chain risk" by the US Pentagon).

Risk: Tensions with the US government could reduce revenue by billions of dollars.

Google (Gemini) - Safest But Slowest

Strengths: Strongest cash flow from existing businesses (Search, YouTube, Cloud), Google Cloud already profitable, Gemini serving costs reduced by 78%. Gemini's market share grew from 5.7% to 21.5% in just one year.

Weaknesses: Big company bureaucracy can slow innovation, history of killing its own products (Google+, Stadia, etc.).

Risk: Lowest among the three - Google can survive even if AI isn't profitable because their core business remains extremely strong.

Is This an AI Bubble? Lessons from the Dot-Com Era

Many analysts compare the current situation with the dot-com bubble of 2000. An MIT report from August 2025 revealed that despite $30 to $40 billion invested by enterprises into GenAI, 95% of organizations received zero return.

Deutsche Bank estimates OpenAI's cumulative losses alone could reach $140 billion between 2024 and 2029. Meanwhile, analysts project "it's going to cost 5x the energy and money to make these models 2x better" - meaning diminishing returns ahead.

However, there's an important difference between the dot-com bubble and the current situation:

Dot-com: Companies like Pets.com had no viable business model and no real product.

AI today: Companies like Google and Microsoft already have extremely profitable businesses. They can support AI losses from existing business profits. But companies that are 100% dependent on AI (like OpenAI) are in a more precarious position.

The analyst consensus is that an AI market correction will likely happen gradually over 2026-2027, rather than a sudden crash. AI companies with unique data "moats" and hardware integration are more likely to survive, while AI startups without distinctive advantages may not.

If you're an investor, understanding the mathematics behind losses is crucial before making investment decisions in a sector still burning cash.

What Does All This Mean for You?

As a regular user in Malaysia, there are several practical implications.

First, take advantage of the free era while you can. Free access to ChatGPT, Claude, and Gemini won't last forever. Analysts expect stricter paywalls and higher subscription prices by 2027.

Second, don't depend on a single platform. Diversifying your AI tools is important because any company could change pricing, limit features, or in the worst case scenario, shut down.

Third, for investors, understand that the AI sector is still in a heavy investment phase. This means it's highly volatile. Don't rush to invest in AI company stocks without understanding how long they can survive before reaching profitability.

Fourth, watch the infrastructure providers. Companies like Nvidia, AMD, and data center providers may be in a better position because they get paid regardless of who wins the AI race - much like jeans sellers during the Gold Rush.

FAQ - Frequently Asked Questions

Will ChatGPT shut down because it's losing too much money?

The likelihood is low in the short term. OpenAI just received $110 billion in financing and has a financial runway until at least mid-2027. However, if revenue growth doesn't meet targets, this risk increases after that period.

Why is Google willing to spend $185 billion on AI?

Google sees AI not as a standalone product but as the foundational layer for all their services - Search, Gmail, YouTube, Cloud. This investment is about maintaining dominance in the digital ecosystem, not just selling a chatbot.

Will AI subscription prices go up?

Most likely, yes. The era of free and cheap AI services is expected to end by 2026-2027. AI companies need to raise prices or shift to usage-based pricing models to achieve profitability.

Who is most likely to go bankrupt - OpenAI, Anthropic, or Google?

Google is virtually impossible to bankrupt as it has an extremely profitable existing business. Anthropic is in the middle with rapid revenue growth. OpenAI is most at risk because it depends entirely on investor funding and has the largest losses.

What is AGI and why does it matter?

AGI (Artificial General Intelligence) is AI that matches humans in all intellectual tasks. If achieved, its value is measured in trillions of dollars because it could replace professional labor across virtually every industry. This is OpenAI's stated primary goal.

How does the AI race affect Malaysia?

Malaysia is indirectly affected through global tech stock prices, job opportunities in the AI sector, and access to AI tools for productivity. Malaysian investors holding stocks like Nvidia, Microsoft, or Alphabet are directly impacted by these competitive dynamics.

Is investing in AI company stocks safe right now?

This depends on your investment horizon. Short-term is very volatile as the sector is still burning cash. Long-term, AI companies that successfully dominate the platform and achieve profitability could become among the most valuable companies in the world. The key is choosing companies with sufficient financial runway and viable business models.

What's the difference between ChatGPT, Claude, and Gemini from a business perspective?

ChatGPT (OpenAI) focuses on general consumers and APIs, Claude (Anthropic) focuses on AI safety and enterprise customers, while Gemini (Google) is integrated into Google's existing ecosystem. Each has a different monetization strategy even though their core products are similar.

Conclusion

The AI race between ChatGPT, Claude, and Gemini isn't just about chatbots - it's a multi-billion dollar bet to control the foundational platform of the future digital economy. Companies willing to lose money today believe the rewards ahead far outweigh current costs, with industry AI revenue projected to reach $1 trillion by 2028.

If you're interested in starting your investment journey and learning more about how these tech giants operate, the first step is understanding stock market fundamentals.

Open a CDS trading account through mahersaham.com/akauncds to start investing on Bursa Malaysia as well as international stocks including US and Hong Kong markets - home to AI tech giants like Nvidia, Microsoft, and Alphabet.

Download the free Stock Market Basics ebook to understand fundamental concepts before making your first investment decision.

Further Reading

- AI Value Chain: 5 Layers Every Investor Must Understand

- Lose 50%, Need 100% to Recover - The Mathematics of Loss Every Investor Must Know

- Rise & Fall of World Powers: What Malaysian Investors Need to Know

- Ponzi Schemes: How They Work & Why Many Still Fall for Them

- AI Trading Experiment Failed: Bot Wiped Out Investor's Crypto Portfolio