Hire Purchase Amendment Act 2026: What Changes and How It Affects You

The Hire Purchase (Amendment) Act 2026 will take effect on 1 June 2026 - marking the biggest overhaul of Malaysia's hire purchase law in over 50 years. If you are currently paying car or motorcycle instalments, or planning to buy a vehicle, this amendment will directly impact your finances.

The amendment abolishes outdated interest calculation methods that disadvantage consumers and introduces a fairer, more transparent system. In this article, we explain all the key changes, their impact on you as a consumer, and what you need to do.

What Is the Hire Purchase (Amendment) Act 2026?

The Hire Purchase (Amendment) Act 2026 is an amendment to the Hire Purchase Act 1967 (Act 212) - the law governing hire purchase agreements in Malaysia. This represents the most significant reform since the original act was enacted.

The bill was passed by Dewan Rakyat on 8 October 2025 and Dewan Negara on 3 December 2025, before being gazetted on 30 January 2026. It will officially come into force on 1 June 2026.

The main objectives of this amendment are to:

- Abolish the Rule of 78 and flat rate interest calculation methods

- Introduce the fairer reducing balance method

- Mandate Effective Interest Rate (EIR) disclosure in all agreements

- Allow digital transactions including electronic signatures

- Establish maximum interest rate caps

Timeline of the Hire Purchase Amendment

The amendment process took several months from tabling to enforcement:

| Event | Date |

|---|---|

| Passed by Dewan Rakyat | 8 October 2025 |

| Passed by Dewan Negara | 3 December 2025 |

| Gazetted (Royal Assent) | 30 January 2026 |

| Takes effect | 1 June 2026 |

| Full prohibition of Rule of 78 & flat rate | 1 January 2027 |

| Goodwill discount programme ends | ~2035 (up to 9 years) |

Financial institutions are given an 18-month transition period from the gazette date to upgrade their systems and processes.

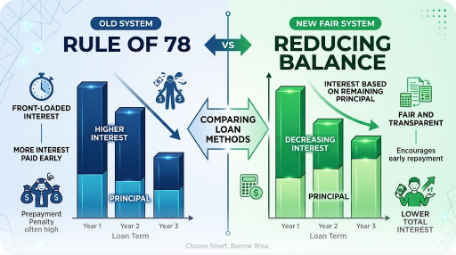

What Is the Rule of 78 and Why Was It Abolished?

The Rule of 78 is an interest calculation method that has been used in hire purchase agreements in Malaysia for decades. It front-loads interest charges to the early portion of the loan - meaning most of the interest is paid in the first few years.

The result? If you want to settle your loan early, your savings are minimal because most of the interest has already been paid.

Practical example:

Say you take a car loan of RM80,000 over 9 years at a nominal rate of 3%. Under the Rule of 78, the actual effective interest rate is approximately 5.5% - nearly double what you would expect.

According to The Edge Malaysia, this is the primary reason why the amendment is considered critical for protecting credit consumers in Malaysia.

The flat rate method calculates interest on the full original loan amount throughout the entire tenure, regardless of how much principal has been repaid. Both methods are now abolished and replaced with a fairer approach.

Reducing Balance Method: The Fairer New System

Replacing the Rule of 78 and flat rate, the amendment introduces the reducing balance method. Under this system:

- Monthly interest is calculated on the remaining loan balance, not the original amount

- Every extra payment directly reduces your principal

- The earlier you settle the loan, the more you save

This means that if you make additional payments, the interest charged will decrease accordingly. This system is the same one used for housing loans, and will now be applied to hire purchase as well.

Additionally, all lenders must now disclose the Effective Interest Rate (EIR) in all marketing materials and loan agreements. This allows consumers to make "apple-to-apple" comparisons between different offers from various banks.

New Interest Rate Caps

The amendment also establishes ceiling interest rates to protect consumers:

| Loan Type | Maximum Rate |

|---|---|

| Loans up to 5 years | 17% per annum |

| Loans exceeding 5 years | 16% per annum |

| Variable rate loans | 17% per annum |

These caps ensure no financier can impose excessively high interest rates, particularly on those with limited financial literacy.

Digital Transformation in Hire Purchase Agreements

Another important change is the permission to use digital signatures and electronic documents in hire purchase agreements. Previously, the process required physical documents and in-person signing.

With the amendment:

- Agreement documents can be sent and signed digitally

- The process is faster and reduces the need for physical attendance

- The term "base lending rate" is replaced with "reference rate" to align with current financial industry standards

Impact on Car and Motorcycle Buyers

If you are paying car instalments or planning to buy a vehicle, here are the direct impacts of this amendment:

Significant Savings on Early Settlement

Under the old system, settling your car loan early was barely worthwhile because most of the interest had already been paid in the early stages. Now, you only pay interest up to your actual settlement date.

Greater Transparency

With mandatory EIR disclosure, you can easily compare the true cost of financing between banks. No more "low rates" that actually hide high interest costs.

Protection for Lower-Income Groups

According to the National Consumer Protection Advisory Council (MPPN), the amendment ensures consumers "no longer bear excessive interest charges" - positively impacting middle and lower-income groups in particular.

Goodwill Discount Programme for Existing Loans

For those who already have existing hire purchase loans, there is good news. The Association of Banks in Malaysia (ABM) together with AIBIM and ADFIM has announced a Goodwill Discount Programme for early settlement.

Who is eligible?

- Individuals and micro/small businesses with existing fixed-rate hire purchase agreements

- Account not in arrears exceeding 90 days

- Not under legal action or repossession order

- Not undergoing restructuring or formal debt management programmes

How long will the programme run?

The goodwill discount programme will remain available until all existing hire purchase agreements mature or are settled early - estimated to be up to 9 years from the effective date.

If you have an existing hire purchase loan and wish to settle early, contact your bank after 1 June 2026 for information about the goodwill discounts offered.

Impact on Banks and the Financial Industry

While the amendment greatly benefits consumers, the impact on banks is expected to be minimal. According to analysis by The Edge Malaysia, fixed-rate hire purchase loans only comprise approximately 10% of the total loan portfolio of public banks.

Bank exposure to hire purchase loans:

| Bank | Portfolio Percentage |

|---|---|

| Affin Bank | 22.5% |

| Public Bank | 18.5% |

| Maybank | 13.1% |

| Hong Leong Bank | 11.5% |

Interestingly, banks have actually been using EIR calculations internally since adopting MFRS 9 in January 2018. This change is more about transparency and disclosure to consumers rather than a major operational shift.

Impact on the Used Car Market

One interesting indirect effect - the amendment could increase the supply of used cars in the market. With lower early settlement penalties, more car owners may choose to upgrade their vehicles sooner.

Comparison: Before vs After the Amendment

| Aspect | Before Amendment | After Amendment |

|---|---|---|

| Interest calculation | Rule of 78 / Flat rate | Reducing balance |

| Early settlement | Minimal savings | Significant savings |

| Rate transparency | Nominal rate only | EIR disclosure mandatory |

| Documentation | Physical only | Digital permitted |

| Interest caps | No clear caps | Maximum 16-17% per annum |

| Rate reference | Base lending rate | Reference rate |

Frequently Asked Questions (FAQ)

Does this amendment affect my existing hire purchase loan?

Not directly. If you continue paying instalments as usual until maturity, no changes are needed. However, if you wish to settle your loan early after 1 June 2026, you can benefit from the Goodwill Discount Programme.

When does the Hire Purchase (Amendment) Act 2026 take effect?

The Act takes effect on 1 June 2026. The full prohibition on the Rule of 78 and flat rate for new agreements will be enforced from 1 January 2027.

What is the difference between flat rate and reducing balance?

Flat rate calculates interest on the full original loan amount throughout the tenure. Reducing balance calculates interest on the remaining balance - meaning every payment you make reduces the interest charged subsequently.

Will my monthly payments change?

For existing loans, your monthly payments remain the same. Changes only apply to new hire purchase agreements signed after the Act takes effect.

Who benefits most from this amendment?

Consumers planning to settle their loans early will benefit the most. Middle and lower-income groups are also protected by the maximum interest rate caps.

Does this amendment cover personal loans and credit cards?

No. This amendment is specifically for hire purchase agreements only - typically involving vehicles, machinery, and consumer goods. Personal loans and credit cards are governed by separate legislation.

How do I get the goodwill discount for my existing loan?

Contact your bank directly after 1 June 2026. Each bank participating in the ABM/AIBIM/ADFIM programme will have their own process and terms for goodwill discounts.

Is Islamic hire purchase also affected?

Yes. The amendment applies to all forms of hire purchase agreements, including Islamic financing that uses hire purchase structures.

Conclusion

The Hire Purchase (Amendment) Act 2026 is a major step towards a fairer and more transparent financing system in Malaysia. The abolishment of the Rule of 78 and the introduction of the reducing balance method means consumers now enjoy better protection - especially those who wish to settle their loans early.

If you are planning to buy a car or vehicle in the near future, consider waiting until after 1 June 2026 to take advantage of the new system. And if you already have a hire purchase loan, check with your bank about the Goodwill Discount Programme offered.

Understanding financial legislation like this amendment is crucial for making smart financial decisions. If you are looking to build an investment portfolio beyond vehicle ownership, the first step is opening the right account.

Open a CDS trading account to start investing in Bursa Malaysia as well as international stocks including US and Hong Kong markets through this link.

Download the free Stock Market Basics Ebook to understand the fundamentals before you start investing here.

Further Reading

- Housing Loan Monthly Instalments - Understand how monthly instalment calculations work for housing loans

- What Is Inflation? - Understanding inflation and how it affects your finances

- Personal Financial Management - A comprehensive guide to managing your personal finances

- Ponzi Schemes in Malaysia - Recognise and avoid investment scams

- Targeted Subsidies in Malaysia - Understanding the government's targeted subsidy system