Tawarruq in Islamic Finance: What Is Permissible & What Is Not

Have you ever applied for Islamic personal financing and noticed the term “Commodity Murabahah” or “Tawarruq” in your agreement documents? You’re not alone — many Islamic banking users in Malaysia don’t truly understand how their money is processed through the tawarruq mechanism. More concerning, many also don’t know that there are forms of tawarruq that are permissible and forms that are disputed by scholars.

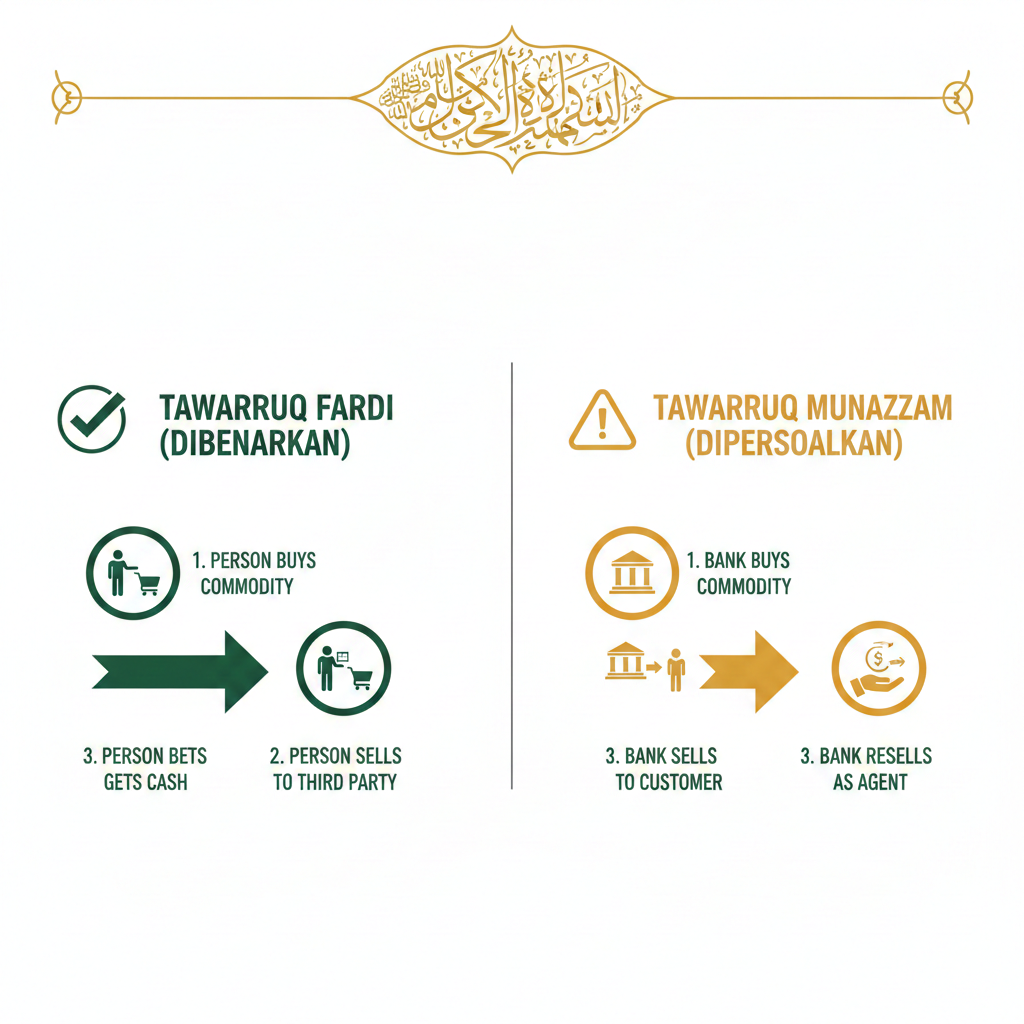

Quick answer: Tawarruq fardi (individual) — where you personally buy a commodity on credit and sell it to a third party for cash — is permitted by the majority of scholars. Tawarruq munazzam (organized) — where the bank arranges the entire process including the resale — was ruled impermissible by the OIC Fiqh Academy but is permitted in Malaysia by Bank Negara Malaysia’s (BNM) Shariah Advisory Council under strict conditions.

What Is Tawarruq?

Tawarruq comes from the Arabic word “wariq” meaning silver coins — broadly referring to money in any form. In the context of modern Islamic finance, tawarruq is a financing mechanism where a person in need of cash (mutawarriq) purchases a commodity on deferred payment (at a marked-up price) and then sells that commodity to a third party for immediate cash.

In simple terms, you “buy goods first, sell goods, get cash.” The commodities commonly used include crude palm oil (CPO), metals, and plastic resin — all traded through the Bursa Suq Al-Sila’ platform launched by Bursa Malaysia in 2009.

How Does Tawarruq Work? Step by Step

Here is the organized tawarruq (tawarruq munazzam) process as practiced in Malaysian Islamic banking:

- You apply for financing at an Islamic bank — for example, RM50,000 personal financing.

- The bank purchases a commodity (e.g., crude palm oil) from Broker A on a cash basis.

- The bank sells the commodity to you on a Murabahah basis — cost + profit, payable in installments. Example: RM50,000 + RM10,000 profit = RM60,000 over 5 years.

- The bank (acting as your agent) sells the commodity to Broker B for cash. You receive RM50,000 in cash.

- You repay the bank RM60,000 in monthly installments.

Critical condition: Broker A and Broker B must be different parties — the commodity cannot return to the original seller. This is what distinguishes tawarruq from bai’ al-inah.

Two Types of Tawarruq

1. Tawarruq Fardi (Individual / Classical)

This is the original form of tawarruq discussed by classical jurists:

- You personally buy a commodity on credit from a seller.

- You independently find a third party to sell the commodity for cash.

- The original seller has no involvement in the resale.

- You receive cash directly from the third-party buyer.

Status: Permitted by the majority of scholars from the Hanbali, Shafi’i, and Hanafi schools.

2. Tawarruq Munazzam (Organized)

This is the modern form used in Islamic banking:

- The bank arranges the entire process on your behalf.

- The bank acts as your agent (wakil) to sell the commodity to a third party.

- You receive cash from the bank, not directly from the third party.

- Involves 3-4 parties and 3 Islamic contracts (Wakalah, Murabahah, Musawamah).

Status: Disputed internationally — the OIC Fiqh Academy ruled it impermissible, but BNM Malaysia permits it.

Permissible Tawarruq — Conditions & Requirements

Based on BNM Policy Document BNM/RH/PD 028 issued on 28 December 2018, tawarruq is permitted in Malaysia subject to the following conditions:

Structural Conditions

- Two genuine sale contracts — first sale (deferred) and second sale (cash/spot).

- Correct sequence — the first sale must be completed before the second sale begins.

- Third-party buyer — the seller in the first sale CANNOT be the buyer in the second sale.

- No interconditionality — the two sales cannot be contractually linked.

Commodity Conditions

- The commodity must physically exist and be identifiable (mu’ayyan bi al-zat) — specific location, quantity, and quality.

- Real ownership transfer at each stage, evidenced by documentation.

- The buyer must have the right to take delivery of the commodity.

- Prohibited commodities: Gold, silver, currencies, assets under construction, and debt instruments.

Operational Conditions

- Time gap between the two sales — exposing parties to genuine price risk.

- Shariah audit required at every stage of the transaction.

- Adequate and transparent disclosure to customers.

Disputed Tawarruq — Why Some Scholars Prohibit It

OIC Fiqh Academy Resolution (2009)

At its 19th session in Sharjah (26-30 April 2009), the OIC International Fiqh Academy issued Resolution No. 179 stating:

- Classical tawarruq (fardi): PERMISSIBLE — provided it complies with sale transaction requirements.

- Organized tawarruq (munazzam): NOT PERMISSIBLE — contains elements of riba.

- Reverse tawarruq (aksi): NOT PERMISSIBLE.

Reasons for prohibiting organized tawarruq:

- Simultaneous, pre-arranged transactions between financier and customer.

- The commodity merely “circulates on paper” without genuine economic activity.

- Considered a stratagem (hilah) to achieve riba — money now in exchange for more money later.

Views of Ibn Taymiyyah & Ibn al-Qayyim

Both scholars took an even stricter position — prohibiting all forms of tawarruq including the classical form:

- True intention: The buyer does not intend to own the commodity but only wants cash — the commodity is merely an intermediary.

- Riba connection: Caliph Umar ibn Abd al-Aziz stated: “Indeed, tawarruq is the origin of riba.”

- Worse than riba: Ibn al-Qayyim argued that tawarruq causes higher costs and greater losses than direct riba.

AAOIFI Position

Shariah Standard No. 30 (AAOIFI) on monetization/tawarruq aligns with the OIC position — organized tawarruq is prohibited, while classical tawarruq is permitted with strict conditions.

Why Malaysia Differs: BNM vs Global Consensus

Malaysia takes a position that differs from the international consensus — permitting organized tawarruq in Islamic banking. This is not a decision made lightly.

BNM’s Shariah Advisory Council permits it based on strict operational safeguards:

- Dedicated Policy Document — BNM/RH/PD 028 outlines comprehensive Shariah and operational requirements.

- Bursa Suq Al-Sila’ Platform — all 15 Islamic banks in Malaysia use this Shariah-compliant commodity trading platform, ensuring commodity transactions are real.

- Mandatory Shariah Audit — every stage of the transaction is reviewed.

- 199th SAC Meeting (November 2019) approved tawarruq via Straight-Through Processing (STP) with additional conditions.

Tawarruq Statistics in Malaysia

Tawarruq is not just a niche product — it dominates the national Islamic finance landscape:

- 57% of total Islamic financing in Malaysia uses tawarruq (BNM 2018 data).

- 80% of Islamic banks use tawarruq for personal financing.

- All 15 Islamic banks subscribe to Bursa Suq Al-Sila’.

- Malaysia’s Islamic banking market now represents over 40% of total banking assets.

However, BNM’s Financial Sector Plan 2022-2026 recommends reducing reliance on tawarruq and encouraging non-commodity-based contracts such as wakalah and mudarabah.

Islamic Banking Products Using Tawarruq

| Product | Example Usage |

|---|---|

| Personal Financing-i | Cash for personal needs |

| Home Financing-i | Mortgage / property financing |

| Credit Card-i | Islamic credit card (replacing Bai’ al-Inah) |

| Vehicle Financing-i | Car financing |

| Business Financing | Working capital, revolving credit |

| Term Deposit-i | Replacing Mudarabah deposits |

| Islamic Overdraft | Overdraft facility |

| Ar-Rahnu (Pawn) | Islamic pawnbroking (approved by BNM SAC 2019) |

Tawarruq vs Bai’ al-Inah — Don’t Confuse Them!

Many confuse these two concepts. Key differences:

| Aspect | Tawarruq | Bai’ al-Inah |

|---|---|---|

| Parties involved | 3 or more parties | 2 parties only |

| Commodity flow | Sold to a third party | Sold back to the original seller |

| Global scholarly acceptance | Majority permissible (classical) | Majority impermissible |

| Status in Malaysia | Permitted | Being phased out |

5 Common Misconceptions About Tawarruq

1. “Tawarruq is the same as Bai’ al-Inah”

No — tawarruq involves a third party, while bai’ al-inah involves only two parties with the commodity sold back to the original seller.

2. “All forms of tawarruq are permissible”

Only classical/individual tawarruq has broad acceptance. Organized tawarruq is prohibited by the OIC and AAOIFI, although Malaysia permits it.

3. “The commodity transaction is just a formality”

For Shariah compliance, the commodity must physically exist, ownership must transfer, and the buyer must be able to take delivery. If commodity trading is merely on paper, the transaction collapses into riba.

4. “Tawarruq completely eliminates riba”

Critics argue organized tawarruq achieves the same economic outcome as an interest-bearing loan — money now exchanged for more money later — and the commodity merely serves as a “legal cover.”

5. “Malaysian scholars are wrong to permit organized tawarruq”

BNM SAC has imposed strict operational safeguards to address concerns that led to the OIC prohibition. This is a considered regulatory decision, not a disregard for Shariah.

FAQ: Frequently Asked Questions About Tawarruq

1. What is the difference between tawarruq and a conventional loan?

Tawarruq involves the actual buying and selling of a commodity as the basis of the transaction, while conventional loans involve direct lending of money with interest. However, critics argue the end economic outcome is similar.

2. Do I legally own the commodity?

Yes — legally and from a Shariah perspective, you own the commodity momentarily before it is resold. Ownership transfer documents are provided as evidence.

3. Can I refuse the resale and keep the commodity?

In theory, yes — you have the right to keep the commodity. However, in practice, most customers sign a wakalah (agency) agreement authorizing the bank to sell on their behalf.

4. Why does Malaysia permit organized tawarruq while the OIC prohibits it?

Malaysia argues that operational safeguards such as Bursa Suq Al-Sila’, mandatory Shariah audits, and BNM’s dedicated policy document address the concerns that led to the OIC prohibition.

5. Is tawarruq only used for personal financing?

No — tawarruq is used across nearly all Islamic banking products including home financing, credit cards, term deposits, overdrafts, and even Islamic pawnbroking.

6. What commodities are commonly used in tawarruq?

Crude palm oil (CPO) is the primary commodity traded through Bursa Suq Al-Sila’. Plastic resin and metals are also used.

7. Is tawarruq more expensive than a conventional loan?

The profit rate for tawarruq is typically comparable to or slightly higher than conventional interest rates, depending on the bank and the borrower’s risk profile.

8. What happens if I fail to pay tawarruq installments?

Similar to conventional financing — the bank will impose late payment charges (ta’widh) and may take legal action. However, late payment charges in Islamic banking have limits set by BNM.

Conclusion

Tawarruq is an important mechanism in Malaysian Islamic finance that allows Muslims to obtain cash financing without directly engaging in riba. However, it’s crucial to understand that not all forms of tawarruq are universally accepted — classical tawarruq (fardi) has broad acceptance, while organized tawarruq (munazzam) remains debated between those who permit it (like BNM Malaysia) and those who prohibit it (like the OIC and AAOIFI).

Start Investing in Shariah-Compliant Stocks

Understanding concepts like tawarruq is the first step to becoming a financially literate Muslim investor — the next step is building your own Shariah-compliant investment portfolio. Open a CDS Trading Account to start investing in Shariah-compliant stocks listed on Bursa Malaysia. Also download the Free Stock Market Basics Ebook to understand the fundamentals of stock investing from a Malaysian Muslim investor’s perspective.

Further Reading

- Why Is Forex Haram? 5 Key Reasons & What Malaysian Fatwa Says

- Gold Price Hits $5,000: How Malaysian Investors Can Profit via Shariah-Compliant Methods

- How to Calculate Zakat on ASB Investments (al-Mustaghallat)

- Complete Guide to Personal Financial Management 2026

- Financial Strategy 2026: Smart Ways to Manage Holiday Spending Without Debt