The End of Cheap EV Imports: Malaysia's New MITI Policy from 1 July 2026 & Its Implications

On 6 May 2026, Malaysia's Ministry of Investment, Trade and Industry (MITI) announced a policy shift that will reshape the country's electric vehicle (EV) market. Effective 1 July 2026, all CBU (Completely Built-Up) EV imports must meet two key conditions:

- Minimum CIF (Cost, Insurance, Freight) value of RM200,000 per unit

- Minimum motor power of 180 kilowatts (kW) and above (down from the previous 200kW threshold)

At first glance, these two conditions look technical. But the implications are wide-ranging: this is the end of the cheap EV import era for Malaysian consumers, and the start of a new era where CKD (Completely Knock-Down, local assembly) becomes the only viable path for foreign EV players entering the Malaysian market.

This article is a policy analysis that breaks down: - How the new mechanism works - Background and original objectives of the 2022-2025 exemption - Estimated actual costs that consumers will bear - Implications for industry players and local strategy - Trade-offs between industry protection and consumer burden - Comparison with Indonesia and Thailand's approaches

Background: Why Was There an Original Exemption?

In 2022, the Malaysian government introduced a special exemption for EV imports under the franchise approved permit (AP) scheme. The original goals:

- Accelerate EV adoption in the local market

- Open competition in the automotive industry (previously dominated by ICE - internal combustion engines)

- Reduce EV prices for middle-class consumers

- Attract global players to sell in Malaysia

The original scheme set a minimum CIF of RM100,000 and was considered relatively liberal. The result: Malaysia's EV market grew rapidly. EV registrations grew 105% YoY in 2025, with 44,813 units sold, and the upward trend continued into 2026.

But the 4-year special exemption period expired on 31 December 2025. This means since January 2026, the policy reverted to standard requirements - normal duties and SST for CBU. However, formal strict enforcement only begins on 1 July 2026 to give importers a transition period.

What Changes from 1 July 2026?

Condition #1: Minimum CIF of RM200,000

CIF is the actual import price paid by the seller to a foreign supplier - before adding duties and margin. RM200,000 CIF means the car is already expensive at origin - not a cheap budget EV from China.

Previously: CIF minimum RM100,000 (under the 4-year scheme) Now: CIF minimum RM200,000 (back to standard, even stricter)

Implication: budget EV models like BYD Dolphin (CIF ~RM80-100K), BYD Atto 3 (base version), Chery Omoda E5, and many others won't qualify for CBU import.

Condition #2: Minimum Motor Power of 180kW (~245 PS)

Previously: 200kW minimum (for the exemption scheme) Now: 180kW minimum (lower, but a separate condition from CIF)

While the 180kW threshold seems lower than the previous 200kW, in the context of this new policy it's combined with the CIF RM200K requirement - so both must be met.

180kW = ~245 PS (Pferdestärke, metric power unit) - equivalent to a mid-tier sports car. Meaning: only high-performance EVs qualify.

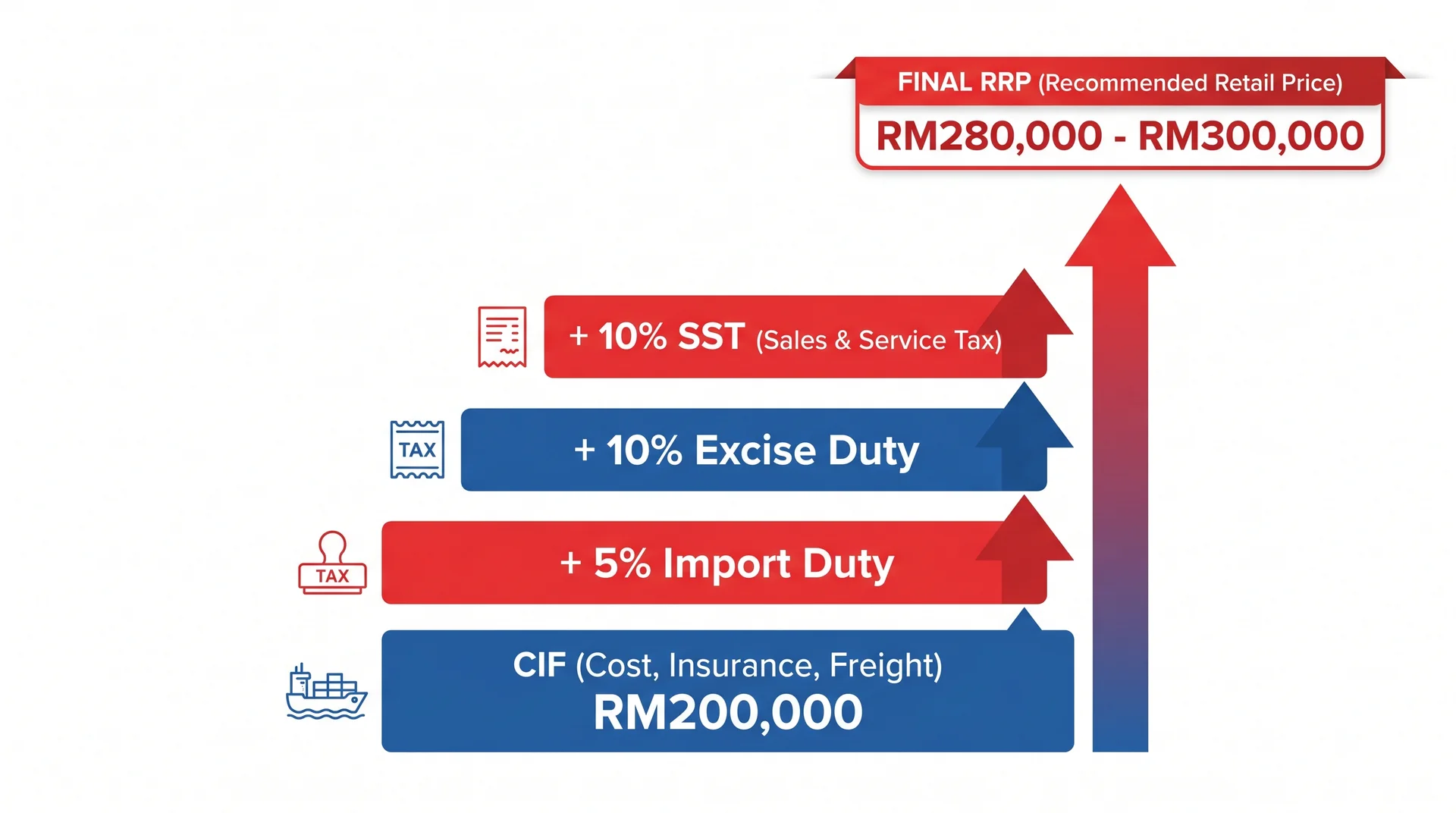

Sequential Tax Stack (Without Exemption)

Without the exemption, the CBU EV tax structure is highly aggressive: 1. Import duty (previously 0% with exemption, now 30% standard - though with FTA/MFN, some get 5%) 2. Excise duty 10% (on CIF + import duty) 3. Sales & Service Tax (SST) 10% (on CIF + import duty + excise duty)

These are applied sequentially - not just on the original value. Each tax layer is added on top of the cumulative total, so the effective tax rate can reach 30%+ on the original CIF.

Estimating Actual Cost to Consumers

Let's calculate concretely. Assume a CBU EV with CIF RM200,000 from China (5% FTA import duty):

| Component | Calculation | Value |

|---|---|---|

| CIF | - | RM200,000 |

| + Import duty 5% | RM200,000 × 5% | RM10,000 |

| Subtotal 1 | - | RM210,000 |

| + Excise duty 10% | RM210,000 × 10% | RM21,000 |

| Subtotal 2 | - | RM231,000 |

| + SST 10% | RM231,000 × 10% | RM23,100 |

| Total taxes | - | ~RM254,100 |

| + Distributor/dealer margin 10% | RM254,100 × 10% | RM25,410 |

| Estimated RRP | - | ~RM280,000-300,000 |

Calculation source: paultan.org analysis of new CBU EV policy

Translation: every CBU EV imported after 1 July 2026 will retail starting RM280K-300K minimum for consumers - even if the original CIF is just RM200K.

For non-China sources (like EU, US), import duty can reach 30% - making the final price even higher.

Policy Analysis: 3 Strategic Intents

Why did the government make this decision? Three strategic intents:

Intent #1: Protect Local Automotive Industry

Proton and Perodua are two pillars of Malaysia's automotive industry. With cheap EV imports tax-free, both face serious competitive pressure:

- Proton e.MAS 7 (CKD - locally assembled): now Proton's main EV product, dominating 50% of the EV registration market in Q1 2026 with 7,455 YTD units

- Perodua QV-E (expected 2026): Perodua's first EV entering the budget market

Without an import barrier like this, cheap EV imports from China could continue dominating the budget RM100K-150K segment and disrupting the local CKD strategy. The RM200K minimum CBU barrier is a protective buffer for Proton/Perodua to stabilise their operations.

Intent #2: Push Localisation (CKD Strategy)

Global EV players wanting to sell in Malaysia now have two main options:

Option A: Bring in as CBU at premium pricing (>RM280K retail) - Only for the luxury segment (BMW, Mercedes-Benz, Audi, Porsche EV) - Less competitive for mass-market

Option B: Set up CKD assembly facility in Malaysia - BYD with Sime Motors has committed to a major facility in Tanjong Malim, expected production H2 2026 - Chery is also considering localisation - Geely (Proton's parent) already has a channel via e.MAS

This strategy attracts foreign direct investment (FDI) in manufacturing, creates jobs, and builds a local supply chain ecosystem - not just selling finished imports.

Intent #3: Reduce Current Account Pressure

Every CBU EV imported is ringgit outflow - payment to foreign manufacturers in foreign currency (USD/CNY). When the EV market grows rapidly, cumulative outflows for CBU can become significant pressure on Malaysia's current account.

By shifting to CKD: - A portion of value (assembly, distribution, marketing, dealer network) stays in the local economy - Components still imported are cheaper (not finished cars) - Local jobs in assembly and distribution

EV Models Affected: Affected vs Surviving List

Below are EV models most affected by the new policy (must localise or exit the Malaysian market):

Models No Longer Eligible (Without CKD)

BYD lineup (most don't meet 180kW + RM200K CIF): - BYD Dolphin - BYD Atto 2 (base version) - BYD Atto 3 (standard version) - BYD M6 - BYD Seal 6

Other Chinese brands: - Chery Omoda E5, Tiggo (EV versions) - Zeekr lower-end models (depending on spec) - Smart #1, #3 (depending on configuration) - iCaur lower-end models

Models Still Eligible (Meet 180kW + RM200K CIF)

BYD high-performance: - BYD Seal (motor 180-230kW, CIF typically >RM200K) - BYD Sealion 7 (motor 230kW)

Premium imports: - Tesla Model 3 Performance, Model Y Long Range/Performance - BMW iX, i4, i5, i7 - Mercedes EQE, EQS - Porsche Taycan - Audi e-tron series

Chinese premium: - Zeekr higher-spec (Zeekr 001, 009, X)

CKD Strategy That Will Save Chinese Brands

- BYD via Sime Motors: Tanjong Malim facility H2 2026 - will assemble Atto, Dolphin, M6 as CKD to avoid CBU restriction

- Proton e.MAS 7: already CKD (Proton Tanjung Malim plant)

- Chery: planning CKD partnership with local players

Impact on Malaysia's EV Market

For Consumers

Negative impact: - Fewer budget EV options (RM100-200K) for several months/years until CKD players bring models to market - Surviving CBU EV prices rise 30-50% (Tesla Model Y, BYD Seal, etc.) - Latest tech delays - global players may be slow to bring new models if localisation is required

Positive impact: - Strong local industry = more jobs + more ecosystem - CKD quality can typically be better controlled - Long-term price stability as it's less forex-sensitive

For EV Distributors / Importers

Players like Sime Motors (BYD), Stellantis Malaysia (Peugeot, Citroen), Bermaz Auto (Mazda), and other distributors must pivot strategy:

- Strategy 1: Localise via CKD partnership

- Strategy 2: Focus on premium models still CBU-eligible

- Strategy 3: Exit the budget EV market

For Bursa-Listed Auto Players (Brief Context)

While this article isn't a stock analysis, the policy generally:

- Positive for Proton-related plays: Although Proton isn't listed, Proton's supply chain (vendor program) provides recurring orders to auto parts players on Bursa

- Tan Chong Motor Holdings (4405), UMW Holdings (4588 - now privatised), Bermaz Auto (5248): implications mixed - depending on each player's EV strategy

- MBM Resources (5983): auto components player, may benefit from CKD localisation

- Sime Darby (4197 / SIMEPROP 5288 separately): Sime Motors is a Sime Darby Bhd subsidiary, so the BYD CKD strategy provides a catalyst

For broader context on the EV industry and related stocks, see Belajar Tentang Kereta Elektrik Untuk Untung Saham.

Trade-off Analysis: Industry Protection vs Consumer Burden

Every protectionist policy has trade-offs. Let's weigh them:

Pro-Policy Arguments

- Industrialisation: Malaysia can't be an import broker forever. Building a CKD ecosystem = building national manufacturing capability

- Jobs: Each CKD plant creates thousands of direct jobs + tens of thousands of indirect ones

- FDI Magnet: BYD's Tanjong Malim commitment is RM5+ billion - significant FDI

- Strategic Autonomy: Reducing dependence on a single country (China) for EVs

- Supply Chain Buffer: Local components = buffer against geopolitical risk

Anti-Policy Arguments

- Tax on Consumers: High costs ultimately borne by consumers - regressive since EV affordability is already a challenge

- EV Adoption Slowdown: More expensive = less transition from ICE (contradicts climate commitments)

- Picking Winners: Government chooses who lives (Proton, BYD-CKD) versus a free market

- Quality Risk: CKD can have quality issues if the supply chain isn't mature

- Time Lag: New CKD players take 1-2 years to fully ramp - during which consumers have fewer choices

Comparison: Indonesia & Thailand

How are other ASEAN countries handling the same challenge?

Indonesia

Indonesia adopted the LCEV scheme (Low-Carbon Emission Vehicle): - Major tax incentives for EV/HEV - But requires localisation timelines: players must commit to assembly within 2-3 years - Result: BYD, Wuling, Hyundai, Tesla have all committed facilities - Indonesia EV market 2026: ~150,000 unit registrations, growing 2x faster than Malaysia

Thailand

Thailand adopted the EV3.5 program (2024-2027): - Cash subsidies for EV consumers (up to 100,000 baht ~RM12K) - 0% import duty incentives for players who commit to 2:1 or 3:1 production ratio (for every 1 EV imported, must produce 2-3 in Thailand) - Result: BYD, Great Wall, MG, Neta all have Thailand factories - Thailand has become ASEAN's EV hub with regional exports

Comparison with Malaysia

| Aspect | Indonesia | Thailand | Malaysia (new) |

|---|---|---|---|

| Approach | Localisation mandate + incentives | Consumer subsidies + production ratios | Price barrier + power threshold |

| Consumer Incentive | Low duty | RM12K subsidy | None directly |

| CKD Players | Many | Many | Few (BYD, Proton) |

| EV Adoption | Fast | Very Fast | Fast but possibly slowing |

Malaysia's approach appears more protectionist compared to Indonesia/Thailand which use carrot-and-stick approaches. This may be an advantage for local players in the short term, but risks slowing EV adoption if budget prices become inaccessible.

Unanswered Questions

Several policy questions still unclear:

1. When Will Perodua Launch Its EV? The Perodua QV-E has been expected but launch dates are still unconfirmed. This delay could affect EV transition momentum.

2. Can Local CKD Achieve Cost Parity with China? Massive scale production in China gives China cost advantages that are hard to match. Malaysian CKD may need government financing or incentives to compete.

3. What Are the Implications for Charging Infrastructure? EV adoption depends on a charging network. If EV prices rise (slow adoption), investment in charging may also slow - becoming a vicious cycle.

4. Will Consumer Incentives Be Announced? Indonesia & Thailand offer subsidies or low road taxes. Malaysia needs to consider similar measures to balance affordability with localisation.

5. What About Used CBU EV Imports? The new policy focuses on new CBU. The used import market (rebuilt, parallel imports) isn't directly addressed in this announcement.

FAQ: Common Questions About the New Policy

1. When exactly does this new policy take effect?

1 July 2026. For EVs already in stock, at ports, or in transit at the time of implementation, companies can still sell them under previous exemption terms until stock is depleted.

2. Will consumers who bought EVs before July 2026 be affected?

Not directly. The policy applies to new imports after 1 July 2026. EVs you've already bought or are holding remain valid; only resale market values may change.

3. Will the Proton e.MAS 7 become more expensive?

No. Proton e.MAS 7 is CKD (assembled at Tanjung Malim), so it isn't affected by the CBU policy. In fact, this policy strengthens Proton's competitive position.

4. What happens to BYD Atto 3, Dolphin, and other budget models that have sold well?

Until in-country/transit stock is depleted, companies can continue selling at the same price (under previous exemption). After that, BYD-Sime Motors will pivot to CKD strategy at Tanjong Malim - new models will arrive as CKD, not CBU.

5. Can I personally import a CBU EV (parallel import)?

Only through registered franchise APs. Individual parallel imports for EVs are very difficult and subject to full tax without exemption.

6. Will luxury brands like Tesla, BMW, Porsche be affected?

Partially. Models like the Tesla Model Y Long Range / Performance, BMW iX, i7, Porsche Taycan - most meet 180kW + RM200K CIF, so they can still be imported as CBU. But without exemption, prices will rise per the sequential tax structure.

7. How do consumers benefit from this policy?

Indirect benefits: - Strong local industry = jobs + ecosystem - Local producers (Proton CKD, future Perodua, BYD CKD) provide options at more competitive prices - Charging infrastructure may be more government-promoted - Resale value of pre-2026 CBU EVs may rise (limited supply)

8. How does this compare to other ASEAN EV policies?

Indonesia & Thailand are more liberal on consumers but strict on localisation. They offer subsidies or low duties to consumers but with strict CKD ratio requirements for players. Malaysia is more protectionist - no direct consumer subsidies, but high entry barriers for CBU. Each approach has its own trade-offs.

Conclusion

MITI's new policy effective 1 July 2026 marks the end of the cheap EV import era in Malaysia. Tightening conditions to a minimum CIF of RM200,000 and motor power of 180kW will trigger structural transformation of the market - shifting from import-driven to CKD-localised. In the short term, consumers will face fewer budget EV options and higher prices for surviving CBU models. But in the long term, FDI investment in local assembly (BYD Tanjong Malim, Proton e.MAS, Perodua QV-E) has the potential to build a more complete manufacturing ecosystem.

The trade-off between local industry protection and consumer burden is a classic public policy question. The success of this policy ultimately depends on one condition: can CKD players deliver price, quality, and technology comparable to or better than the CBUs being shut out? If yes, this becomes a win-win. If no, it becomes a hidden tax on consumers bearing the cost of industrial transition.

Before deciding to buy an EV or invest in related auto stocks, ensure you have an active trading account and a strong grasp of investing fundamentals.

To start investing in Bursa Malaysia and overseas markets like the US and Hong Kong, you need a CDS account - register your CDS account with Mahersaham here.

For investing fundamentals including how to read financial statements, valuation, and thematic strategies, get our free stock investing basics ebook.

Further Reading

- Belajar Tentang Kereta Elektrik Untuk Untung Saham - Foundational guide to EV-themed investing

- Apa Itu Levi? Beza Dengan Cukai, Siapa Bayar & Ke Mana Duitnya? - Understanding Malaysia's tax and levy structures

- Saham Pembinaan: MRT3, Project Mega & Bila Construction Cycle Pulih - Other mega project sectors reshaping Malaysia

- Iklim Boleh Telan 8.3% KDNK Malaysia: Saham Bursa Mana Untung, Mana Rugi? - Climate context and energy transition

- Selain NVIDIA: 8 Syarikat Yang Untung Dari AI Boom - Other global industry exposure