GST vs SST in Malaysia: Which Tax System Is Better? Research, Data & Global Comparison

Malaysia used GST for three years before it was abolished and replaced with SST in 2018. This decision sparked an intense debate that continues to this day. Some argue GST is more efficient and transparent, while others believe SST is more people-friendly and easier to implement.

In this article, we take an in-depth look at the real differences between GST and SST, what researchers and international bodies say, and how neighboring countries handle their consumption taxes. All of this is examined from a 2026 perspective - with real data, not assumptions.

What Are GST and SST?

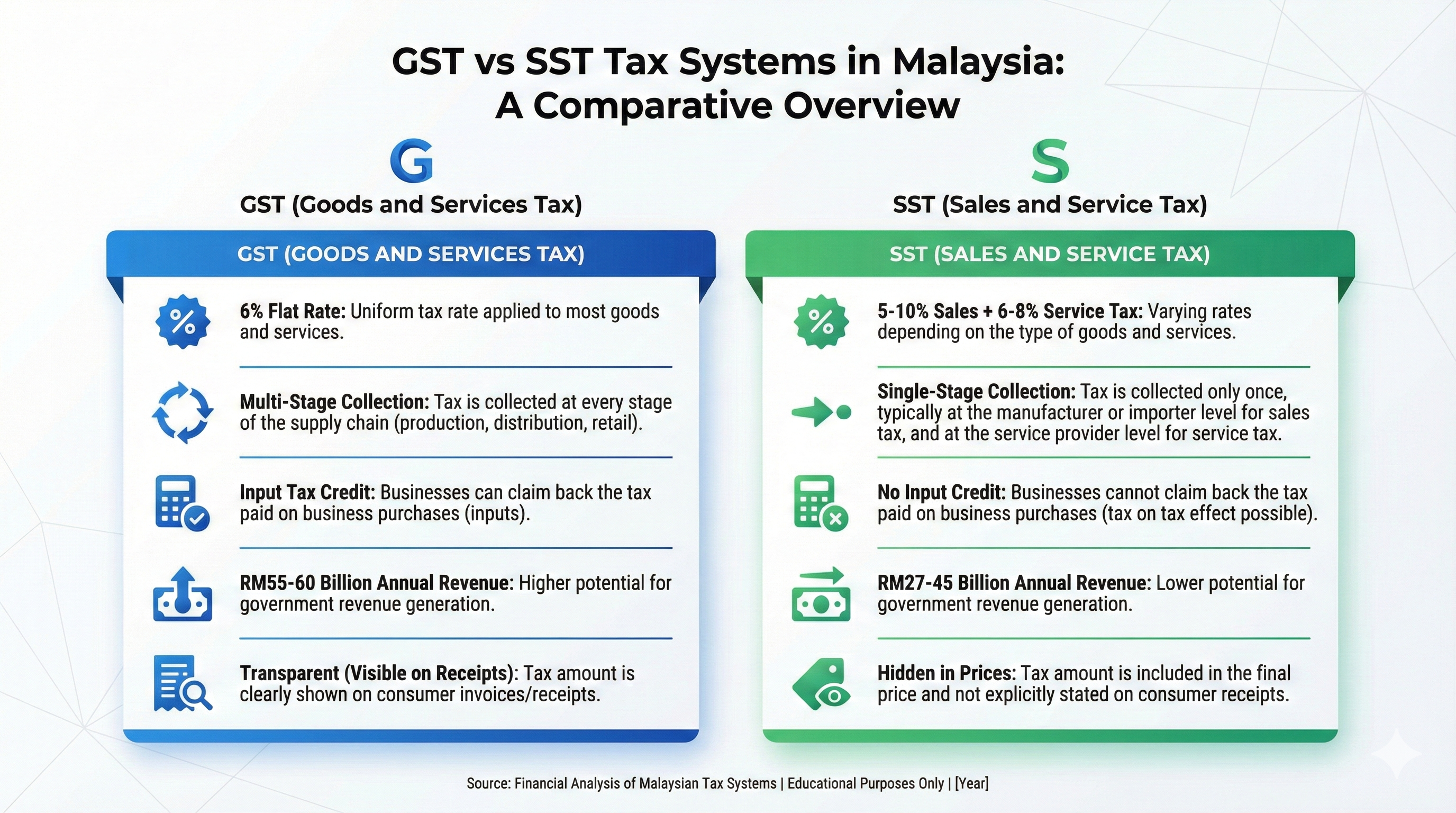

GST (Goods and Services Tax)

GST, or Goods and Services Tax, is a multi-stage consumption tax. It is levied at every stage of the supply chain - from manufacturers, wholesalers, and retailers, all the way to the end consumer.

Key features of GST:

- A uniform rate of 6% applied to nearly all goods and services

- An input tax credit mechanism - businesses can claim back GST paid at previous stages

- No cascading effect because each stage only pays tax on the value added

- Essential goods were exempted (zero-rated) such as rice, sugar, cooking oil, and flour

GST was implemented in Malaysia starting 1 April 2015 and abolished on 1 June 2018.

SST (Sales and Services Tax)

SST, or Sales and Services Tax, is a single-stage tax. Sales tax is imposed at the manufacturing or import level, while services tax is charged on specific service providers.

Key features of SST:

- Sales tax: 5% or 10% depending on the type of goods

- Services tax: 6% to 8% (most services are now 8% after the 2025 revision)

- A narrower scope - only selected goods and services are taxed

- No input tax credit mechanism - businesses cannot claim back taxes paid

- Simpler administration compared to GST

SST was reintroduced on 1 September 2018 following the abolition of GST.

Key Differences: GST vs SST

| Aspect | GST | SST |

|---|---|---|

| Tax type | Multi-stage | Single-stage |

| Rate | Uniform 6% | 5-10% (sales), 6-8% (services) |

| Coverage | Nearly all goods & services | Selected goods & services only |

| Input tax credit | Yes - businesses can claim back | None |

| Cascading effect | None (tax on value added only) | Yes - taxes can stack up |

| Transparency | High - consumers see tax on every receipt | Low - tax is hidden in prices |

| Administrative burden | Higher (strict documentation) | Lower (simpler administration) |

| Exports | Zero-rated (no tax) | Limited exemptions |

How Much Does the Government Collect? Actual Revenue Data

This is the most important part that many people overlook - the difference in revenue collection between GST and SST is substantial.

GST Revenue Collection (2015-2018)

According to data from the Ministry of Finance Malaysia, GST collection from April 2015 to May 2018 totaled RM184.8 billion:

- 2015: RM37.7 billion (only 9 months, starting April)

- 2016: RM55.7 billion

- 2017: RM60.5 billion

- 2018: RM30.9 billion (only 5 months, until May)

On average, GST generated approximately RM55-60 billion per year at full rate.

SST Revenue Collection (2018-2025)

After SST was reintroduced, collection dropped significantly according to BERNAMA:

- 2018: RM5.4 billion (4 months, starting September)

- 2019: RM27.6 billion

- 2020: RM25.2 billion (affected by COVID-19)

- 2021: RM25.5 billion

- 2022: RM31.3 billion

- 2023: RM35.4 billion

- 2024: RM44.7 billion (exceeding the RM41.3 billion target)

Although SST has shown improvement, the average annual collection remains significantly lower than GST - especially in the early years before the scope expansion.

Revenue Gap: RM20-25 Billion Per Year

This difference means the government lost an estimated RM20-25 billion per year in consumption tax revenue after switching from GST to SST. This is a substantial amount - it could fund various development programs, subsidies, and infrastructure projects.

However, the government is working to close this gap. According to the Ministry of Finance, the SST scope expansion effective 1 July 2025 is expected to generate an additional RM5 billion in 2025 and RM10 billion in 2026.

What Researchers and International Bodies Say

The GST vs SST debate is not just public opinion - it is backed by serious academic studies and reports from international bodies.

IMF (International Monetary Fund)

In its Article IV Consultation 2025 report, the IMF recommended that Malaysia strengthen domestic revenue through a tax system that is broader-based and more efficient. The IMF noted that Malaysia's tax-to-GDP ratio had declined to 12.3% in 2024 - among the lowest in ASEAN. IMF analysis shows Malaysia could potentially collect an additional 3% of GDP through proper tax reforms, including the reintroduction of GST.

World Bank

The World Bank in its Malaysia Economic Monitor also emphasized the need to broaden the tax base. In discussions with the Malaysian Institute of Economic Research (MIER), World Bank economists including Dr. Apurva Sanghi emphasized that broad-based consumption taxes like GST are more efficient instruments compared to single-stage taxes.

MIT Press Study - "The Untimely Demise of GST"

An important study published in Asian Economic Papers by MIT Press examined in depth why GST was abolished and what should have been done. The study found:

- GST was implemented too hastily to cover the government's deficit and debt

- Lack of preparation to address the impact on price levels caused public dissatisfaction

- Technically, Malaysia achieved a good C-efficiency score during GST (2015-2017), indicating effective tax administration

- The abolition of GST was a decision more political than economic in nature

MIER (Malaysian Institute of Economic Research)

MIER published an analysis titled "The Invisible Cost of SST" which revealed the hidden costs of SST to the public. According to MIER, SST's "tax-on-tax" structure causes the prices of everyday goods to increase without consumers realizing it - even though essential goods are exempted, the stacked tax costs along the supply chain still raise the prices of food and other necessities. MIER also collaborated with the World Bank in reviewing Malaysia's fiscal position.

Universiti Malaya - SWRC Working Paper

A working paper from the Social Wellbeing Research Centre (SWRC), Universiti Malaya titled "Resurrecting Goods and Services Tax (GST): The Case for A Comeback" argued that GST should be reintroduced with improvements:

- A lower rate at the initial implementation stage

- Direct compensation for the B40 group

- A longer transition period

- A better e-invoicing system to reduce compliance burden

Prof. Yeah Kim Leng (Sunway University)

Prof. Yeah Kim Leng, former member of Bank Negara Malaysia's Monetary Policy Committee and currently Professor of Economics at Sunway University, is among the most vocal supporters of GST. He stated that transitioning back to GST "would not be too costly or difficult" as long as the previous implementation weaknesses are addressed. According to him, Malaysia's continuously declining tax-to-GDP ratio proves that SST is insufficient to fund the nation's needs.

Center for Market Education (CME)

The Center for Market Education, led by Carmelo Ferlito, also warned that excessive reliance on non-transparent indirect taxes like SST could fuel illicit trade and smuggling. CME supports a value-added tax (VAT) system that is more rational, simpler, and predictable.

Comparison with ASEAN Countries

Malaysia is currently among the few ASEAN countries that do not use a broad-based consumption tax system (like VAT/GST). Here is a comparison of consumption tax rates in the region according to ASEAN Briefing:

| Country | Tax Type | Standard Rate | Year Started |

|---|---|---|---|

| Singapore | GST | 9% | 1994 |

| Thailand | VAT | 7% | 1992 |

| Indonesia | PPN (VAT) | 12% | 1984 |

| Philippines | VAT | 12% | 1988 |

| Vietnam | VAT | 10% (temporarily reduced to 8%) | 1999 |

| Cambodia | VAT | 10% | 1999 |

| Laos | VAT | 10% | 2009 |

| Myanmar | Commercial Tax | 5% | - |

| Malaysia | SST | 5-10% (sales), 6-8% (services) | 2018 (reintroduced) |

What Can We Learn?

Singapore - the most successful model in ASEAN. GST was introduced at a low rate of 3% in 1994, then gradually raised to 9% by 2024. Each increase was accompanied by substantial offset assistance packages for lower-income citizens. The result? Public acceptance, strong government revenue, and a competitive economy.

Indonesia - just raised its PPN from 11% to 12% in January 2025. Despite some resistance, the Indonesian government sees broad-based consumption tax as a non-negotiable revenue foundation for development funding.

Thailand - maintains VAT at 7% (lower than the standard 10% rate) to encourage domestic consumption. Thailand's model shows that a low rate but broad base can generate stable revenue.

The key lesson: nearly all developed and developing nations use a multi-stage consumption tax system (VAT/GST). Malaysia is a rare exception - a country that once had GST but abolished it.

Malaysian Government Stance in 2026

As of February 2026, the government's position is clear - SST will be maintained, at least for the near term.

According to the Ministry of Finance, Second Finance Minister Datuk Seri Amir Hamzah stated that the expanded SST is designed to be more progressive and fairer. The government chose to stick with SST because:

- SST is already understood by the public and businesses - no transition costs

- Faster fiscal impact - no need for 2 years of preparation like GST

- Tax burden is concentrated on those who can afford it (non-essential and luxury goods)

- People's income is still low - the Ministry of Finance stated it is not the right time for GST

However, a report by VATCalc suggests that GST may be reconsidered after 2029, which is after the next general election that must be held before February 2028.

SST Scope Expansion 2025-2026

As a middle ground, the government has expanded the SST scope starting 1 July 2025 to include:

- Sales tax: Non-essential and luxury goods that were previously exempted

- Services tax: More than 30 new service categories including rentals, construction, education, financial services, and healthcare

This move is expected to generate an additional RM15 billion by 2026 - helping to close part of the revenue gap that has existed since the abolition of GST.

So, Which One Is Actually Better?

The answer depends on the priorities we set:

Arguments for GST

- Higher and more stable revenue - data shows GST generated nearly double compared to SST

- More transparent - consumers see exactly how much tax they pay

- No cascading effect - taxes do not stack up, making goods cheaper along long supply chains

- Broader base - the shadow economy is also subject to tax because all transactions are taxed

- International standard - over 170 countries use VAT/GST systems

- More competitive exports - exports are fully exempted (zero-rated)

Arguments for SST

- Lower administrative burden - especially for SMEs (Small and Medium Enterprises)

- Lower direct price impact - not all goods are taxed

- Public familiarity - no transition costs or social resistance

- More flexible - the government can choose what to tax and what to exempt

- Protection of essential goods - basic necessities are clearly exempted

A Balanced Perspective

Technically and economically, the majority of researchers and international bodies agree that GST is more efficient as a tax system. But efficiency alone is not enough - implementation, timing, and public acceptance are equally important.

Malaysia's biggest mistake was not GST itself, but how it was implemented:

- The 6% rate was introduced all at once without phasing

- Compensation to the public (BR1M) was insufficient and poorly targeted

- Government communication about GST was very weak

- Traders took advantage by raising prices in the name of GST

- There was no adequate transition period

What Should Be Done?

Based on research and the experience of other countries, here are the most practical recommendations:

1. Low-Rate GST with Phasing

Follow Singapore's model - start GST at a low rate (e.g., 4%) and increase it gradually every 2-3 years. This gives people and businesses time to adjust.

2. Direct Compensation for B40

Every GST increase must be accompanied by direct cash compensation to the B40 group. Singapore does this through its GST Voucher Scheme - Malaysia could adopt a similar model through existing assistance systems like STR (Sumbangan Tunai Rahmah).

3. A Wider Exemption List

Daily essential goods (rice, vegetables, meat, fish, milk, basic medicine) should remain zero-rated or fully exempted. This ensures the impact of GST on the cost of living is minimized.

4. E-Invoicing First, GST Later

Malaysia has already begun phased implementation of e-invoicing. This is a smart move because e-invoicing creates the compliance infrastructure needed before GST is reintroduced. Once all businesses are compatible with e-invoicing, the transition to GST will be much smoother.

5. Communication and Public Education

The biggest failure of the previous GST was a failure of communication. The public needs to understand:

- How much they actually pay in tax (hidden SST vs visible GST)

- How GST revenue is used to fund public services

- That essential goods remain exempted

Frequently Asked Questions (FAQ)

Will GST be reintroduced in Malaysia?

As of 2026, the government has no plans to reintroduce GST. However, some political leaders and economists suggest it may be reconsidered after 2029, following the next general election.

Why did prices rise during the previous GST?

Prices did not rise entirely because of GST - a large part was due to traders who took advantage by raising prices in the name of GST, even though their goods were exempted or zero-rated. Weak enforcement worsened the situation.

Is SST cheaper for consumers than GST?

Not necessarily. Although SST is not applied to all goods, the hidden SST taxes embedded in prices (without input claims) can cause a cascading effect. This means some goods are actually more expensive under SST than they would be under GST.

How much revenue did the government lose after abolishing GST?

The government lost an estimated RM20-25 billion per year in consumption tax revenue. This amount is being reduced through the SST scope expansion, which is expected to generate an additional RM10 billion by 2026.

Which country has most successfully implemented GST?

Singapore is often cited as the benchmark. They started GST at a low rate of 3% (1994), gradually raised it to 9% (2024), and each increase was accompanied by offset assistance packages for lower-income citizens.

Does GST cause inflation?

Studies show GST causes a one-off price increase in the first year of implementation, not sustained inflation. Malaysia's inflation rate was actually stable in 2016-2017 while GST was in effect.

Why do almost all countries use VAT/GST?

Over 170 countries use VAT/GST because it is more efficient, transparent, and generates stable revenue. This system also reduces the shadow economy because every stage of the supply chain must report taxes.

What is the difference between VAT and GST?

Technically, VAT (Value Added Tax) and GST (Goods and Services Tax) are the same system - a multi-stage consumption tax with an input tax credit mechanism. The difference is only in the name used by different countries. For example: Singapore, Australia, and India call it GST; while the EU, Thailand, and Indonesia call it VAT/PPN.

Conclusion

The GST vs SST debate is not merely a technical tax question - it is closely tied to the nation's fiscal stability, economic competitiveness, and public welfare. Data shows GST generated nearly double the revenue compared to SST, and the majority of international researchers agree it is more efficient. However, the hasty implementation in 2015 and the failure in communication left negative effects that are still felt today.

The most realistic way forward is to learn from past mistakes and the experience of neighboring countries - if GST returns, it needs to come with a low rate, gradual phasing, and direct compensation for those who need it most.

Understanding the nation's tax system is an important part of financial literacy for every investor and individual in Malaysia.

If you are interested in starting to invest on Bursa Malaysia, the first step is to open a CDS Trading Account through a registered broker.

Also download the Free Stock Market Basics Ebook to learn the fundamentals of stock investing from scratch.