Islamic Will (Wasiat) in Malaysia: How to Write & Register Before It Is Too Late

Every time a Muslim passes away without a will, a long process begins. Assets get frozen, the courts must intervene, and family members sometimes feud for years. In Malaysia, thousands of estate cases are pending in the Syariah Courts and at Amanah Raya at any given time - most of them avoidable if the deceased had spent just a few hours writing a will.

But here is the irony: wasiat (Islamic will) is treated as trivial because it concerns death. A topic many avoid thinking about - until it is too late.

This article explains what wasiat is in Islam, why it differs from hibah and faraid, who should write one (the answer: nearly every adult), how much it costs, and the practical steps to register with Amanah Raya, As-Salihin, or banks in Malaysia.

What Is Wasiat in Islam?

Wasiat (from the Arabic wasiyya) is an instruction or directive made by a Muslim during their lifetime to be carried out after their death. It involves the distribution of part of one's estate to specific individuals or institutions, or special instructions such as the appointment of a wasi (executor) and a guardian for children.

Contrary to common perception, wasiat in Islam is not about distributing all of your wealth - that is the role of faraid (which takes effect automatically upon death). Wasiat only fills certain "gaps" that faraid cannot cover.

The ruling on wasiat in Islam is permissible (harus) and in certain situations becomes obligatory - for example, if you have debts that must be settled after death, or if you wish to leave something for a party not protected by faraid.

Why Wasiat Matters: A Reality Many Overlook

Without a will, your assets are distributed strictly according to faraid. This can cause several problems:

1. Assets get frozen

Bank accounts, CDS shares, real estate - all frozen until the estate process is complete. For small estates (under RM2 million), the Amanah Raya route can take 6 months to 2 years. For larger ones via the High Court, it can take many years.

2. Faraid does not cover non-heirs

Adopted children, an apostate spouse, close friends, or children born out of wedlock - all receive nothing under faraid. Wasiat lets you give up to 1/3 of your estate to them.

3. Waqf and outstanding debts hang in limbo

Debts owed by you must be paid first, and debts owed to you must be claimed. Without a will, family members may not know these even exist.

4. Guardianship of minor children

If you and your spouse die simultaneously (e.g. a road accident), who cares for the children? Without a will, the court decides - sometimes differently from your wishes.

5. Family conflict

Anecdotal data suggests more than half of Malaysian estate cases end in family disputes. A written will reduces ambiguity about the deceased's intentions.

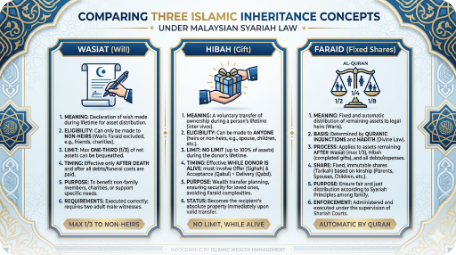

Wasiat vs Hibah vs Faraid

These three concepts are often conflated. Here are the basic differences:

| Aspect | Wasiat | Hibah | Faraid |

|---|---|---|---|

| When it takes effect | After death | While alive | After death |

| Limit | Maximum 1/3 of estate | No limit | Fixed shares |

| Recipients | Non-heirs only | Anyone | Faraid heirs only |

| Revocable | Yes, anytime before death | No (once ownership transfers) | Not applicable |

| Witnesses required | Yes (4 Muslim witnesses) | Yes (2 witnesses) | None |

| Tax/zakat | Subject to faraid before distribution | None | Yes, before distribution |

An easy way to think about it: Hibah = give while alive. Faraid = automatic distribution. Wasiat = additional instructions for special cases.

For a deeper understanding of faraid and hibah, read Hibah & Faraid: Islamic Estate Inheritance in Malaysia.

The 1/3 Rule: Maximum Wasiat Limit in Islam

This is the most important rule in Islamic wasiat. You cannot bequeath more than 1/3 of your net estate to non-heirs.

What is the net estate? According to the JAWHAR Manual on Islamic Wasiat Management, net estate is calculated after deducting:

- Funeral management costs

- Debts of the deceased (to Allah such as zakat, and to people)

- Conjugal property of the spouse

The 1/3 limit is then applied after these deductions.

Example:

- Gross estate: RM900,000

- Less debts: RM100,000

- Less spouse's conjugal property: RM200,000

- Net estate: RM600,000

- Wasiat limit (1/3): RM200,000

A wasiat exceeding 1/3 requires consent from all heirs after the testator's death. Otherwise, the excess is returned to faraid distribution.

Wasiat Cannot Be Given to Heirs (Without Consent)

This is the second most important point that many do not realise. According to the hadith of the Prophet Muhammad SAW: "There is no wasiat for an heir."

This means you cannot bequeath to:

- Children (sons or daughters)

- Spouse

- Parents

- Siblings (in certain situations)

The reason? They already receive their share through faraid. A wasiat to an heir is considered "double dipping" and unfair to the other heirs.

Exception: If ALL other heirs consent after the testator's death, a wasiat to an heir can be carried out. But this is rare given the difficulty.

So who CAN receive a wasiat?

- Adopted children (not biological)

- Stepchildren

- An apostate spouse

- Children born out of wedlock

- Close relatives who are not faraid heirs (e.g. grandsons, if the deceased's sons are still alive)

- Close friends / caregivers

- Institutions (mosques, schools, NGOs, orphanages)

- Waqf

When You Should Seriously Consider a Wasiat Now

Not everyone has an urgent need to write a wasiat. But if any of the situations below apply, the sooner the better:

1. You have adopted children

Adopted children do not receive faraid. Without a wasiat, they receive nothing from your estate.

2. You have children born out of wedlock you wish to provide for

Same principle - they are not faraid heirs and need a wasiat to receive any share.

3. You have undisclosed debts

Debts must be settled before faraid. A wasiat lets you document them clearly.

4. Your spouse is an apostate or non-Muslim

A non-Muslim spouse does not inherit from a Muslim under faraid. Wasiat can give them up to 1/3.

5. You wish to make waqf

Waqf for mosques, religious schools, or da'wah projects can be done through wasiat (within the 1/3 limit).

6. You wish to appoint a specific wasi

A wasi (executor) administers the wasiat. Without an appointment, the court decides - which can be slow.

7. You have minor children

To appoint a guardian you trust, you must state it in the wasiat.

8. Assets overseas

US shares, Singapore property, UK accounts - cross-border estate planning is more complex. A wasiat helps.

How to Write a Wasiat: 4 Provider Options in Malaysia

You have four main options to formally prepare a wasiat in Malaysia:

1. Amanah Raya Berhad (ARB)

A trustee company 99.9% government-owned, established in 1921. It is the most mainstream and affordable option.

- Basic Wasiat: ~RM350-400 (depending on channel)

- Comprehensive Wasiat: ~RM950

- Channels: ARB branches, Hong Leong Bank / Hong Leong Islamic Bank, online via HLB Connect

- Services: Drafting + custody + execution

Suitable for: medium estates (RM200K - RM2 million), basic needs without special complexity.

2. As-Salihin Trustee Berhad

A shariah-compliant trustee company with 21+ years of experience, per official information.

- Wasiat fees: ~RM1,500 and above (depending on complexity)

- Add-ons: Hibah Amanah, Waqf, Trust planning

- Services: 1-on-1 consultation, comprehensive estate planning

Suitable for: large estates (RM1 million+), complex estate plans, professional Islamic advice required.

3. Islamic Banks (Bank Islam, Bank Muamalat, BSN)

Local banks offer wasiat writing services as part of their wealth management.

- BSN: Offers conventional and Islamic wasiat

- Bank Muamalat: Service via partnership with ARB

- Bank Islam: Separate service for Wealth customers

- Fees: Roughly RM500 - RM2,000 depending on type and bank

- Channels: Bank branches, by appointment

Suitable for: existing customers of those banks, looking for a one-stop shop for wealth + estate.

4. State Islamic Religious Councils (MAIS, MAIWP, etc.)

Each state has an Islamic Religious Council offering wasiat services. Selangor through MAIS is among the most active.

- Fees: Cheaper, sometimes free for asnaf

- Channels: Mufti / MAIS / Baitulmal offices in each state

- Services: Drafting + custody + execution within the religious ecosystem

Suitable for: those who want an official state-backed source, or B40 individuals needing affordable services.

Steps to Register a Wasiat (Example: Amanah Raya)

Here is the basic process to register a wasiat with ARB - it is broadly similar with other providers:

1. Schedule an appointment

Visit the nearest ARB or Hong Leong Bank branch, or use HLB Connect online.

2. Bring basic documents

- Copy of NRIC (yours and 4 witnesses)

- List of assets (bank accounts, CDS shares, property, vehicles, takaful policies)

- Information on hibah/wasiat beneficiaries (name, NRIC, relationship)

3. Discuss with the service provider

They will ask detailed questions about:

- Assets and values

- Debts and liabilities

- Wasi (executor) appointment

- Guardianship of children

- Distribution to non-heirs (within the 1/3 limit)

4. Wasiat draft preparation

The provider prepares a written draft. You review and request changes if needed.

5. Sign with witnesses

The wasiat MUST be signed by:

- You (testator)

- 4 adult Muslim witnesses (male or female, baligh, sound of mind)

- Witnesses must NOT be beneficiaries or close family members of the heirs

6. Official custody

ARB stores the original document in a secure vault. You receive a copy and a registration certificate.

7. Update when needed

You may amend or revoke the wasiat anytime before death. Each amendment usually incurs an additional fee.

What Happens If You Die Without a Wasiat?

This is the reality many do not want to hear. If you die intestate (without a will) in Malaysia, several processes kick in:

For SMALL estates (under RM2 million):

- Application to Amanah Raya Berhad or the Land Office

- Duration: 6 months - 2 years

- Fee: 5% of estate value (capped)

For LARGE estates (RM2 million+):

- Application to the High Court

- Lawyer required (RM5,000 - RM50,000+)

- Duration: 1-5 years

For Muslims, part of the process involves the Syariah Court:

- Faraid certificate from the state Syariah Court

- Heir testimony and registration required

Throughout this period:

- Bank accounts are frozen

- Shares cannot be sold

- Real estate cannot be transferred

- The family may struggle financially even though the estate is sizeable

This is the main reason wasiat matters - it speeds up and simplifies the process for your family.

Common Mistakes in Wasiat Writing

Avoid these pitfalls:

1. Wrong choice of witnesses

Witnesses MUST be adult Muslims, NOT beneficiaries, and NOT close family of the heirs. Witnesses violating these rules can invalidate the wasiat.

2. Wasiat exceeding 1/3 without planning for heir consent

The excess will revert to faraid - which can spark conflict after death.

3. Wasiat to heirs without planning

Not automatically valid unless other heirs consent.

4. Assuming KWSP/Tabung Haji nominees are enough

Nominees are merely administrators - the funds still return to the estate and are distributed by faraid.

5. Not updating after major life events

After marriage, divorce, having a new child, or buying major assets - the wasiat MUST be updated.

6. Storing the wasiat in a hard-to-find place

It has happened before - the wasiat is prepared but not found until years after death. Always store with an official institution (ARB, As-Salihin) or in a safe deposit box with clear access.

7. Not including instructions for digital accounts

Trading accounts, e-wallets, crypto, password managers - in the digital age, these need to be addressed.

FAQs

How much does it actually cost to write a wasiat in Malaysia?

Depends on provider: Amanah Raya RM350-950, As-Salihin RM1,500+, MAIS cheaper or free for asnaf, Islamic banks RM500-2,000.

Is a handwritten wasiat valid?

Valid under shariah law if it meets the requirements (4 Muslim witnesses, adults, not beneficiaries). But execution will be difficult since no institution holds the original. Better to register with ARB/As-Salihin.

Can I bequeath my KWSP money?

Not directly. The KWSP nominee is only an administrator - funds revert to the estate and are distributed by faraid. To give to non-heirs, it must come from the 1/3 wasiat portion.

Do I need to update my wasiat every year?

No. Update only when there are major changes - marriage, divorce, having a child, buying/selling major assets, beneficiary changes, death of a witness or wasi.

What is the difference between a wasi (executor) and a beneficiary?

A wasi is the person who carries out the wasiat - manages distribution, settles debts, files documents. A beneficiary is the person who receives the assets.

Can I include CDS shares from Bursa Malaysia in a wasiat?

Yes. CDS shares are personal assets that can be included in a wasiat (for the 1/3 non-heir portion) or distributed under faraid (for heirs).

What happens to my debts after death?

Your debts must be paid first from the estate before the remainder is distributed under faraid/wasiat. If debts exceed assets, heirs are not personally liable (except for joint debts).

Can my apostate spouse receive from a wasiat?

Yes. An apostate spouse does not inherit under faraid but can be a wasiat beneficiary within the 1/3 limit.

Conclusion

A wasiat is not merely about money - it is about trust and final responsibility to your family. In Islam, it is a way to complete what faraid cannot do: provide for loved ones who are not heirs, appoint a trusted wasi, and simplify the process for your family.

The lowest cost is just RM350 with Amanah Raya, and the time required is less than an hour of discussion. Compared to the burden your family bears if you die intestate - years of process, thousands in lawyer fees, frozen assets - it is one of the most worthwhile investments people often delay.

While you sort out your estate plan, do not forget that long-term investment is also part of your family's financial legacy - what you build today is what they inherit tomorrow.

Open a CDS trading account today to start investing in Bursa Malaysia as well as overseas markets including US and Hong Kong stocks through one platform.

Download our free stock market basics ebook to understand investment fundamentals before taking the next step.