Kelly Criterion: The Formula for How Much Capital to Put Into a Single Stock

Every stock investor has faced the same question: "How much money should I put into this stock?" Many answer by guessing - RM1,000 because that is what is in the account, or going "all-in" because they feel confident the stock will rise. The problem is that a wrong position-sizing decision can wreck your portfolio even when your stock pick is correct.

This is where the Kelly Criterion comes in. It is a mathematical formula that tells you the optimal percentage of capital to allocate to a single position, based on the edge you have. This article explains the formula, shows you how to calculate it step by step, and most importantly, covers the limitations you must understand before applying it on Bursa Malaysia.

What Is the Kelly Criterion?

The Kelly Criterion (also known as the Kelly Formula or Kelly Strategy) is a formula for determining the optimal bet or position size to maximise long-term capital growth. It was created by John Larry Kelly Jr., a researcher at Bell Labs, in 1956. It was originally developed for a telecommunications signal problem, but was later adapted by professional investors and gamblers for money management.

The core idea of the Kelly Criterion is simple: do not bet too little (you fail to maximise profit) and do not bet too much (one loss can wipe out your capital). The formula finds the balance point that maximises the geometric growth rate of your capital over time. According to Wikipedia, mathematically it maximises the expected value of the logarithm of wealth - which is equivalent to maximising long-term growth.

Famous investors such as Warren Buffett and Bill Gross are reported to use principles similar to Kelly when making their position-sizing decisions. This is not merely an academic formula - it is used in the real world.

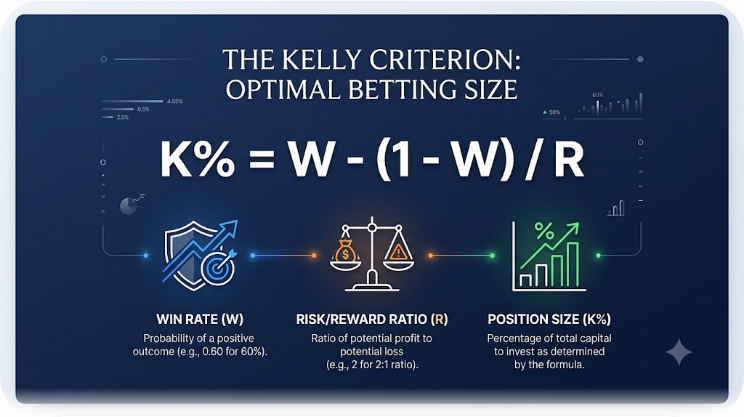

The Kelly Criterion Formula

The most commonly used version of the Kelly formula for stocks is:

K% = W - [(1 - W) / R]

Where:

- K% = the percentage of capital you should allocate to the position

- W = your win rate, the percentage of profitable trades out of total trades

- R = the risk/reward ratio (average win divided by average loss)

The formula is sometimes also written as K% = bp - q / b, where p is the probability of winning, q is the probability of losing (1 - p), and b is the reward-to-risk ratio. According to Investopedia, both versions give the same answer - only the notation differs.

The key thing to understand: the Kelly Criterion requires TWO inputs - how often you win (W), and how big your wins are relative to your losses (R). Without both data points, the formula cannot be used accurately.

A Step-by-Step Worked Example

Let us use a practical example for an investor on Bursa Malaysia. Suppose you reviewed your last 100 trades and found:

- You won 60 out of 100 trades (win rate = 60%, so W = 0.60)

- Average profit per winning trade = RM1,500

- Average loss per losing trade = RM1,000

- So the risk/reward ratio R = 1,500 / 1,000 = 1.5

Plug into the formula:

K% = 0.60 - [(1 - 0.60) / 1.5]

K% = 0.60 - [0.40 / 1.5]

K% = 0.60 - 0.267

K% = 0.333 or 33.3%

The result: the Kelly Criterion suggests you allocate 33.3% of your capital to that position. If your capital is RM50,000, this means roughly RM16,650 for a single position.

Notice one important thing - 33.3% is a very high and aggressive number. This is exactly why many professional investors do not use full Kelly, but rather a more conservative version as discussed below.

Half Kelly: Why Professionals Use Half

One of the biggest problems with full Kelly is that it produces very high volatility. Putting 33% of your capital into a single stock means that if that stock crashes, you could lose a large chunk of your portfolio in one blow.

That is why most professional traders use Fractional Kelly - usually Half Kelly (half of the Kelly percentage). In the example above, Half Kelly means you allocate only 16.65% instead of 33.3%.

Why half? According to analysis at Zerodha Varsity, Half Kelly captures roughly 75% of the optimal growth rate but significantly reduces drawdown. You sacrifice a little upside for far better capital protection - a worthwhile trade-off for most investors.

Advantages of the Kelly Criterion

Why is this formula popular among serious investors and traders?

- Objective, not emotional: Position size is calculated from data, not from feelings of "confidence" or "fear". This reduces the emotional decisions that often damage portfolios.

- Maximises long-term growth: Mathematically, following Kelly produces the highest wealth over the long run compared to fixed-size strategies.

- Avoids ruin: As long as you do not exceed the Kelly percentage, the probability of losing your entire capital is very low.

- Scales with your edge: The bigger your edge (high win rate + high R), the bigger the suggested position. This is logical - bet more when the odds are better.

Risks and Limitations You Must Know

This is the part most often ignored but most important. The Kelly Criterion is NOT a magic formula. It has serious limitations:

1. Garbage in, garbage out. The formula is only as good as the win rate (W) and ratio R you feed it. The problem is that the stock market is not like a dice game - your probability of winning fluctuates and is hard to estimate accurately. If you overestimate your win rate, Kelly will suggest a position that is too large and dangerous.

2. Past performance is no guarantee of future results. A 60% win rate based on 100 past trades does not mean you will stay at 60% going forward. Market conditions change.

3. High volatility. As discussed, full Kelly can cause portfolio swings that are psychologically hard to bear. Many investors "panic sell" during large drawdowns.

4. It does not account for correlation. If you hold several stocks in the same sector (for example, all bank stocks), calculating Kelly separately for each can leave you overexposed to a single risk. Also consider the right number of stocks in your portfolio.

5. It requires emotional discipline. Kelly only works if you follow it consistently. Mental biases such as overconfidence can corrupt your calculations - something we discuss in our article on the 7 mental biases of Bursa Malaysia investors.

How to Apply It for Bursa Malaysia Investors

So how do you use the Kelly Criterion practically and safely? Here is a step-by-step guide:

- Step 1 - Gather your real data. Record at least 30-50 past trades. Calculate your win rate (W) and your average win versus average loss (R). Without this data, do not use Kelly.

- Step 2 - Calculate full Kelly. Use the formula K% = W - [(1 - W) / R].

- Step 3 - Use Half Kelly or Quarter Kelly. Divide the result by 2 (or 4 for more conservative sizing). This is your actual position size.

- Step 4 - Set a maximum cap. Even if Kelly suggests 20%, many investors cap it at 5-10% per stock for diversification. Do not let one stock dominate your portfolio.

- Step 5 - Combine with a stop loss. Kelly determines position SIZE, but you still need a stop loss to protect your capital if the trade does not work out.

For long-term (buy and hold) investors who do not trade often, the Kelly Criterion is less suitable because you do not have a clear win-rate dataset. For them, a simpler position-sizing strategy and diversification may be more practical.

Kelly vs Traditional Position Sizing

Most beginner investors use simple methods such as "equal weighting" (for example, 10% each for 10 stocks) or the 2% rule (never risk more than 2% of capital per trade). How does Kelly differ?

- Fixed rules (2%, equal weight): Simple, safe, no data required. Suitable for beginners. But not optimal - it does not account for your actual edge.

- Kelly Criterion: More mathematically optimal, adjusts size to your edge. But it requires accurate data and high discipline. Suitable for experienced traders with a clear track record.

There is no single "right" answer for everyone. For most Malaysian investors, the best combination is to use Kelly as a guide, but cap position size with strict diversification rules.

Common Mistakes When Using the Kelly Criterion

Although the formula looks simple, many investors stumble when applying the Kelly Criterion. Here are the most common mistakes and how to avoid them:

- Overestimating win rate. This is the most dangerous mistake. Investors tend to remember wins and forget losses, so the win rate they enter is too high. As a result Kelly suggests an oversized position. Always use real records, not memory.

- Using full Kelly without fractional sizing. Putting 30% or more into a single stock is a recipe for extreme emotional swings. Always use Half Kelly or Quarter Kelly.

- Recalculating too often. Changing position size after every one or two trades leads to inconsistent decisions. Gather a large enough sample before updating W and R.

- Ignoring transaction costs. Brokerage, levy, and stamp duty on Bursa Malaysia reduce your real profit. The win rate and R you calculate should account for these costs, not just gross prices.

- Treating the market like a fixed-probability game. Unlike a coin flip, the probability of winning in stocks changes with market conditions. Kelly gives an estimate, not a guarantee.

Avoiding these mistakes means you use Kelly as a disciplined guide, not a blind formula followed without thought. Combine it with an understanding of the difference between investing, trading, and gambling so you stay on the right side.

Frequently Asked Questions (FAQ)

Is the Kelly Criterion suitable for long-term investors?

Less so. Kelly requires a clear win rate and ratio R, which usually only active traders have. Buy-and-hold investors are better served by diversification and simple position sizing.

What is Half Kelly and why is it popular?

Half Kelly is half of the full Kelly percentage. It captures roughly 75% of optimal growth but significantly reduces volatility and drawdown risk. Most professionals use it.

What if the Kelly Criterion gives a negative answer?

If K% is negative, it means you have NO edge on that trade - the probability of winning times the reward does not exceed the probability of losing times the risk. The recommendation: do not take that trade at all.

What percentage of capital is safe for a single stock?

There is no absolute number, but many advisors recommend not exceeding 5-10% of capital per stock for healthy diversification, even when Kelly suggests more.

Can I use Kelly for crypto or forex?

In theory yes, because the formula is the same. But crypto and forex are far more volatile, so estimating win rate is harder and risk is higher. Be careful.

Does Warren Buffett use the Kelly Criterion?

Buffett is reported to use Kelly-like principles - taking large positions when the edge is clear and small positions when uncertain - although he does not formally call it "Kelly".

Where can I calculate the Kelly Criterion?

You can calculate it manually with the formula K% = W - [(1 - W) / R], or use an online Kelly calculator. The important thing is that your inputs (W and R) come from your real trading records.

Conclusion

The Kelly Criterion is one of the most powerful money-management tools in investing - it transforms the question "how much should I put in?" from a guess into a mathematical calculation based on your real edge. The formula K% = W - [(1 - W) / R] gives you the optimal percentage, but remember: it is only as good as the data you feed it, and most professionals use Half Kelly to reduce risk.

Before you can apply a formula like the Kelly Criterion or any other money-management strategy, you need an account to invest and real trading records.

Open a CDS and trading account with us to start investing on Bursa Malaysia as well as foreign markets such as the United States and Hong Kong.

You can also download our free stock market basics ebook to understand the key concepts before you begin investing.

Further Reading

- Stop Loss & Position Sizing: How to Protect Your Capital Before Buying Stocks

- Why Position Sizing Is 80% of Your Trading Strategy

- How Many Stocks Should Be in One Portfolio? Optimal Size & Diworsification Risk

- Investor Psychology: 7 Mental Biases That Make You Lose on Bursa Malaysia

- Game Theory & Stock Trading: Why the Simplest Strategy Often Wins