What Is PRS? The Private Retirement Scheme Most Malaysians Overlook

Ask 100 Malaysians where they save for retirement, and 95 will say "EPF". Ask the same group whether they know what PRS is, and most will furrow their brows and reply "never heard of it".

This is a curious reality. PRS (Private Retirement Scheme) has existed in Malaysia since 2012. It is regulated directly by the Securities Commission (SC) Malaysia, administered by an official body (PPA), and offers personal tax relief of up to RM3,000 per year. Yet 14 years after its launch, most Malaysians still assume EPF alone is enough for retirement.

The truth: EPF alone is not enough for the majority of Malaysians. According to EPF's own data, more than 50% of members aged 54 have savings of less than RM10,000. PRS was designed to close this gap.

This article explains what PRS is, how it differs from EPF, the tax benefits you receive, and whether it is suitable for you.

Quick Answer: What Is PRS?

PRS (Private Retirement Scheme) is a voluntary long-term retirement savings scheme approved by the Securities Commission Malaysia. It allows you to add to your retirement savings on top of EPF, with fund choices based on your risk profile and tax relief of up to RM3,000 per year.

In simple terms: EPF is mandatory and chosen by your employer. PRS is voluntary and entirely under your control.

A Brief History: Why Was PRS Introduced?

In 2012, the Malaysian government identified a major problem - most workers would not have enough money to retire. Even though all private sector employees contribute to EPF, the accumulated amount typically only lasts 3-5 years post-retirement, while Malaysia's average life expectancy is around 75 years.

This means if you retire at 60, you need enough money for another 15 years. For most Malaysians, EPF savings run out within 5 years, after which they must rely on their children or government assistance.

That is why PRS was introduced - as the third pillar of Malaysia's retirement system:

- Pillar 1: Government pension (for civil servants) or JKM (for poor senior citizens)

- Pillar 2: EPF (mandatory for all private sector employees)

- Pillar 3: PRS (voluntary, for retirement top-up)

PRS is administered by Private Pension Administrator Malaysia (PPA) - a body specifically established to oversee the scheme.

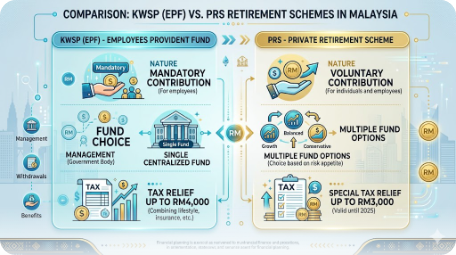

PRS vs EPF: What Are the Real Differences?

Many people confuse PRS and EPF since both are for retirement. But there are 5 key differences:

| Factor | EPF | PRS |

|---|---|---|

| Contribution | Mandatory (11% employee + 13% employer) | Voluntary (you decide) |

| Fund Choice | 1 fund only (same for all members) | Choose between aggressive/moderate/conservative |

| Min Contribution | Depends on salary | RM100 only |

| Withdrawal Before 55 | Very limited (health, housing, education) | Sub-Account B can be withdrawn (8% tax penalty) |

| Tax Relief | RM4,000 (combined with life insurance) | RM3,000 separately |

The most important point: PRS is NOT a replacement for EPF. It is an ADDITION. The right way to think about it - EPF is the foundation, PRS is the top-up.

According to The Edge Malaysia, several PRS funds actually outperform EPF over the long term, although with higher volatility.

9 SC-Approved PRS Providers in Malaysia

According to PPA, there are 9 PRS provider companies approved by the Securities Commission Malaysia:

- AHAM Capital (formerly Affin Hwang Asset Management)

- AIA Pension and Asset Management

- AmInvestment Management (AmPRS)

- Hong Leong Asset Management

- Kenanga Investors

- Manulife Investment Management

- Principal Asset Management (formerly CIMB-Principal)

- Public Mutual

- RHB Asset Management

Each provider offers several funds - aggressive (more equity), moderate (mixed), and conservative (more bonds and fixed income instruments). You can join multiple providers if you want, but combined contributions cannot exceed the tax relief limit (RM3,000 per year).

Provider selection criteria: historical fund performance, management fees, service quality, and whether shariah-compliant PRS is available (for Muslim investors).

Fund Choices: Aggressive vs Moderate vs Conservative

This is where PRS wins big over EPF. With EPF, everyone gets the same fund - no choice. With PRS, you can pick a fund based on your age and risk tolerance:

Aggressive Fund (Growth)

- 70-80% invested in equities (stocks)

- Suitable for: ages 20-40, with a long horizon to retirement

- Highest return potential but high volatility

- Examples: Principal PRS Plus Growth, AmPRS - Growth

Moderate Fund (Balanced)

- ~60% equity, 40% bonds

- Suitable for: ages 40-50, balancing growth and stability

- Moderate returns, moderate volatility

- Examples: Principal PRS Plus Moderate, AmPRS - Moderate

Conservative Fund (Cautious)

- Majority in bonds, sukuk, and fixed income instruments

- Suitable for: ages 50+, near retirement

- Lower returns but stable, low volatility

- Examples: AmPRS - Conservative

Default Option: If you do not choose, PRS will auto-allocate based on age:

- 18-39 years → Growth fund

- 40-49 years → Moderate fund

- 50+ years → Conservative fund

PRS Tax Relief: How Much Can You Save?

This is PRS's biggest incentive. You can claim personal tax relief of up to RM3,000 per year for PRS contributions, according to the PPA Tax Relief page. This incentive is valid until assessment year 2030.

How much do you actually save? It depends on your tax bracket:

| Annual Income | Marginal Tax Rate | Tax Saved (RM3,000 contribution) |

|---|---|---|

| RM35,000 - RM50,000 | 8% | RM240 |

| RM50,001 - RM70,000 | 13% | RM390 |

| RM70,001 - RM100,000 | 21% | RM630 |

| RM100,001 - RM400,000 | 24-25% | RM720-750 |

| RM400,001+ | 28-30% | RM840-900 |

So if your income is RM80,000 per year and you contribute RM3,000 to PRS, you save RM630 in tax. This means your RM3,000 contribution actually costs you only RM2,370 - the rest you would have paid to LHDN anyway.

Important: This relief is separate from the EPF + life insurance relief (RM7,000). So if you have already maxed out EPF + insurance, PRS adds another RM3,000.

Withdrawal Rules: Sub-Account A vs Sub-Account B

When you contribute to PRS, it auto-splits 70:30 into two sub-accounts:

Sub-Account A (70% of contribution)

- Locked until age 55

- Withdrawable when: retirement (age 55), death, or permanently leaving Malaysia

- Purpose: ensure retirement money truly accumulates

Sub-Account B (30% of contribution)

- Withdrawable ONCE per year

- Penalty: 8% tax deduction on the withdrawn amount

- Penalty exemption: withdrawal for first home or medical treatment

Example calculation: If you contribute RM3,000, RM2,100 goes to Sub-Account A (locked) and RM900 goes to Sub-Account B (withdrawable with penalty).

This rule is designed to balance flexibility and discipline - you have access to part of the money for emergencies, but the majority remains secured for retirement.

PRS Youth Incentive: Extra RM500 for Young Savers

To encourage younger generations to start saving early, the government offers the PRS Youth Incentive - a one-off contribution of RM500 into the PRS account of eligible youth.

Eligibility criteria (according to the PPA Youth page):

- Malaysian citizen

- Aged between 20-30 years

- Accumulated contribution of at least RM1,000 within the specified period

The RM500 incentive is credited directly to Sub-Account A by PPA after you qualify. So for an RM1,000 contribution, you receive an additional RM500 = RM1,500 in your account. That is an instant 50% return before the fund even starts investing.

However, check the latest updates on the PPA website as this program has specific periods and budgets - it is not permanent.

Who Should Consider PRS?

PRS is not for everyone. It is most suitable for:

- Workers who have maxed out EPF + insurance relief and still have spare income

- Self-employed/freelancers who do not have mandatory EPF

- Those worried EPF will not be enough (statistics show the majority indeed will not be)

- Investors aged 30+ who want to top up retirement with forced discipline

- Tax relief seekers who want to reduce their LHDN burden

PRS is less suitable for:

- You still do not have enough money for an emergency fund (3-6 months of expenses)

- You have high-interest debt (credit cards, personal loans) - pay debt first

- You need money for short-term goals (under 5 years)

- You are in the 0% tax bracket (income < RM35,000) - tax benefit does not apply

How to Start PRS: Step-by-Step

According to information from Principal Malaysia:

- Register PPA Account - Visit ppa.my and register a free PPA account. This is the central account that tracks all your PRS holdings.

- Choose PRS Provider - Compare the 9 providers above. Key criteria: fund performance, annual fees (sales charge typically 1-3%, management fee 1-1.8% per year), service level, availability of shariah-compliant funds.

- Select Fund - Based on age and risk tolerance (Growth/Moderate/Conservative). Or pick the default option based on age.

- First Contribution - Min RM100. Can be one-time or set up monthly auto-debit.

- Claim Tax Relief - When filing LHDN e-Filing next year, enter the PRS contribution amount in the "Private Retirement Scheme Relief" section (up to RM3,000).

- Track Performance - Log into your PPA account or provider's app to check fund value each quarter.

Risks & Caveats You Must Know

PRS is not without risks. Before joining, understand these:

1. Not capital guaranteed - Unlike EPF which has a minimum 2.5% guarantee, PRS can lose principal especially in aggressive funds heavily invested in equities.

2. Real fees are high vs ETFs - Total cost (sales charge + management fee + trustee fee) can hit 2-3% per year. Compared to direct ETF investing (0.1-0.5%), this is expensive.

3. Limited liquidity - The bulk (Sub A 70%) is locked until 55. Even if you retire early, accessing it is difficult.

4. Performance depends on provider & fund - Not all PRS funds perform. Do proper research or use PPA Fund Performance data to compare.

5. Tax relief is not return - Many misunderstand this. The RM3,000 tax saved is a one-time saving - not the annual return from the PRS investment itself.

Practical Scenario: PRS for a 30-Year-Old Investor

Ahmad, 30 years old, earns RM80,000 per year (21% tax bracket). He decides to start PRS.

Plan: Contribute RM250 per month = RM3,000 per year to a Growth fund (Principal PRS Plus Growth).

Year 1 outcome:

- Contribution: RM3,000

- Tax saved: RM630 (21% of RM3,000)

- Net cost: RM2,370

After 25 years (until age 55) - assuming average return of 6% per year:

- Total contribution: RM75,000 (RM3,000 x 25)

- Total tax saved: RM15,750 (RM630 x 25)

- Fund value (compound 6%): ~RM164,000

- Net wealth from PRS: ~RM179,750 with out-of-pocket cost of RM59,250

For an RM250/month commitment, Ahmad adds ~RM164k to his retirement pot alongside EPF. That is a game-changer for a more comfortable retirement.

FAQs

What is the difference between PRS and EPF?

EPF is mandatory (deducted from salary), with no fund choice and limited withdrawals. PRS is voluntary, offers fund choices according to your risk profile, and provides tax relief of up to RM3,000 per year.

Can I withdraw PRS money before age 55?

Yes, but limited. Sub-Account B (30%) can be withdrawn once a year with an 8% tax penalty. Withdrawals for first home purchase or medical purposes are exempt from the penalty. Sub-Account A (70%) is locked until 55.

What is the minimum contribution required?

The minimum first contribution is RM100. After that, you can contribute as much as you want whenever you want - no fixed commitment.

Is PRS guaranteed by the government?

No. PRS is an investment, so values can go up or down. Unlike EPF which has a guaranteed minimum 2.5% dividend.

How much tax relief do I actually get?

Tax relief of up to RM3,000 per year. The actual saving depends on your tax bracket - typically RM240 (8%) to RM840 (28%).

Are there shariah-compliant PRS options?

Yes, most providers offer shariah-compliant PRS funds. Examples: AmPRS Tactical Bond - I Class, Principal Islamic PRS Growth, RHB Islamic PRS Growth.

Can I have both EPF and PRS at the same time?

Yes, and it is recommended. PRS is an ADDITION, not a replacement for EPF. Most financial planners recommend a combination of both.

What happens to PRS if I change jobs or become self-employed?

Nothing - PRS is an individual account, not tied to your employer. It follows you for life.

Conclusion

PRS is not a magic bullet for retirement, but it is one of the most underutilised instruments by Malaysians. With tax relief of up to RM3,000 per year, fund choices based on risk profile, and forced discipline for long-term saving, it complements EPF which is often insufficient.

The key: understand the mechanics first (Sub A vs Sub B, fund choices, fees), then commit. A properly chosen PRS can add hundreds of thousands to your retirement pot over 20-30 years.

While building your retirement pot via PRS, do not forget to diversify into other investment instruments such as direct stocks on Bursa Malaysia and overseas stocks to maximise long-term growth.

Open a CDS trading account today to start investing in Bursa Malaysia as well as overseas markets including US and Hong Kong stocks through one platform.

Download our free stock market basics ebook to understand investment fundamentals before taking the next step.