What Is Takaful? Differences With Conventional Insurance & Basic Strategies

Many Malaysians are still confused — what exactly is takaful, and why is it different from conventional insurance? This question frequently arises, especially among those who want to ensure their family''s financial protection aligns with Shariah principles.

The reality is, Malaysia''s takaful industry has recorded assets worth RM62.54 billion as of mid-2025, with a market penetration rate of approximately 19.54%. However, the Malaysian Takaful Association (MTA) is targeting penetration of up to 40% by 2028 — indicating that many Malaysians remain unprotected.

This article will answer fundamental questions about takaful, explain the key differences with conventional insurance, and share basic strategies you can use to protect yourself and your family.

Quick Answer

Takaful is a financial protection system based on the principles of ta''awun (mutual assistance) and tabarru'' (contribution/donation) among participants. Unlike conventional insurance which operates on the principle of transferring risk to the company, takaful operates on risk-sharing among participants — making it Shariah-compliant as it is free from elements of riba (interest), gharar (uncertainty), and maisir (gambling).

What Is Takaful? Definition & Core Concepts

The word "takaful" originates from the Arabic word kafala, meaning mutual guarantee. According to Bank Negara Malaysia (BNM), takaful is an arrangement where a group of participants agree to mutually help and guarantee each other in the event of misfortune.

Core Principles of Takaful

Takaful is built upon several fundamental principles:

- Ta''awun (Cooperation & Mutual Assistance) — Participants cooperate to protect one another. This aligns with the Islamic concept that encourages the community to help each other.

- Tabarru'' (Contribution/Donation) — Each participant donates a portion of their contribution into a common fund (tabarru'' pool). This fund is used to help any participant who experiences misfortune.

- Free from Riba, Gharar & Maisir — All takaful operations must be Shariah-compliant, supervised by the Shariah Advisory Council of each takaful operator.

- Risk-Sharing — Unlike conventional insurance which transfers risk to the company, takaful shares risk among participants.

Brief History of Takaful in Malaysia

Malaysia is among the earliest countries to systematically develop the takaful industry. The first takaful company in Malaysia — Syarikat Takaful Malaysia Berhad — was established in 1984, making Malaysia a pioneer in this industry globally.

Today, the takaful industry is regulated under the Islamic Financial Services Act 2013 (IFSA) and closely supervised by BNM.

How Does Takaful Work?

To understand takaful, you need to know how participant contributions are managed. There are two main models:

Wakalah Model (Agency)

In this model, the takaful operator acts as an agent (wakil) on behalf of participants. The operator charges a wakalah fee (agency fee) from participants'' contributions to manage the fund and operations. The remaining contribution goes into the tabarru'' fund and investment fund.

Mudharabah Model (Profit-Sharing)

In this model, the takaful operator acts as a fund manager (mudharib). Investment profits are shared according to a pre-agreed ratio between participants and the operator. In case of losses, the loss is borne by participants (capital owners).

Takaful Fund Flow

In summary, here is how money flows in takaful:

- Participants pay contributions — not "premiums" as in insurance.

- Part of the contribution goes into the tabarru'' fund (for claims) and part into the investment fund.

- Funds are invested only in Shariah-compliant instruments.

- If a participant experiences misfortune, claims are paid from the tabarru'' fund.

- If there is a surplus in the tabarru'' fund at the end of the year, it can be redistributed to participants — this is what significantly differentiates takaful.

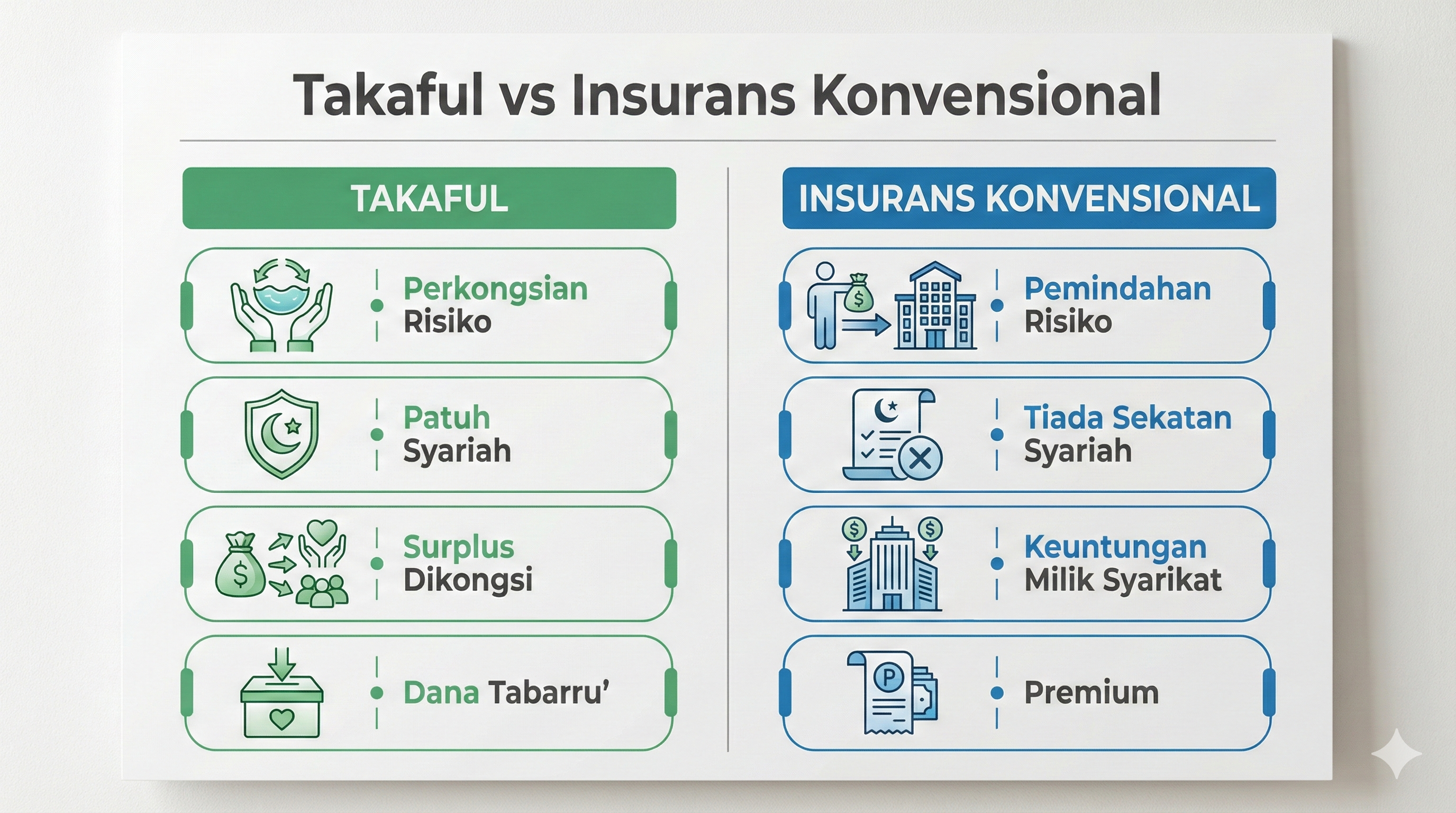

Takaful vs Conventional Insurance

This is the most popular question. Here is a comparison table to help you understand:

| Aspect | Takaful | Conventional Insurance |

|---|---|---|

| Basis | Risk-sharing (ta''awun) | Risk transfer |

| Contract | Tabarru'' (donation) + Wakalah/Mudharabah | Sale and purchase (seller-buyer) |

| Payment | Contribution | Premium |

| Investment | Shariah-compliant instruments only | No Shariah restrictions |

| Profits | Shared between participants & operator | Fully owned by insurance company |

| Surplus Fund | Redistributed to participants | No surplus sharing concept |

| Supervision | Shariah Advisory Council + BNM | BNM only |

| Prohibited Elements | Free from riba, gharar, maisir | No restrictions |

The Most Significant Difference

The most important difference that many don''t realise is the concept of surplus sharing. In takaful, if the tabarru'' fund has a surplus after paying all claims in a year, that surplus can be distributed to participants. In conventional insurance, all profits belong to the company.

Additionally, takaful requires all investments in Shariah-compliant instruments — meaning your money will not be invested in companies involved in alcohol, gambling, or non-halal activities.

Types of Takaful in Malaysia

There are several main types of takaful available:

1. Family Takaful

Provides long-term protection for individuals and families. This includes:

- Life protection plans — Provides benefits in the event of death or total permanent disability

- Savings & education plans — For children''s education or retirement purposes

- Medical & health plans — Covers hospitalisation and surgery costs

- Investment-linked takaful — Combines protection with Shariah-compliant investment

As of mid-2025, the family takaful segment recorded 6.69 million active certificates with annual contributions exceeding RM9.87 billion.

2. General Takaful

Provides short-term protection (usually one year) for assets and liabilities:

- Motor takaful — Vehicle protection

- Fire/home takaful — Property protection

- Travel takaful — Protection while travelling

- Personal accident takaful — Protection in case of accidents

3. Investment-Linked Takaful

This plan combines protection with investment elements. Part of the contribution is used for takaful protection, while the rest is invested in Shariah-compliant funds of the participant''s choice.

Licensed Takaful Operators in Malaysia

All takaful operators in Malaysia must be licensed by BNM. Major operators include:

Family Takaful:

- Syarikat Takaful Malaysia Keluarga Berhad

- Prudential BSN Takaful Berhad

- AIA PUBLIC Takaful Bhd

- Great Eastern Takaful Berhad

- Etiqa Family Takaful Berhad

- Hong Leong MSIG Takaful Berhad

- Sun Life Malaysia Takaful Berhad

- Takaful Ikhlas Family Berhad

- Zurich Takaful Malaysia Berhad

- FWD Takaful Berhad

General Takaful:

- Syarikat Takaful Malaysia Am Berhad

- Etiqa General Takaful Berhad

- Takaful Ikhlas General Berhad

- Zurich General Takaful Malaysia Berhad

For the latest and most detailed list, you can check directly on the official BNM website.

Basic Takaful Strategies for Consumers

Choosing the right takaful plan requires planning. Here are some basic strategies:

1. Prioritise Medical Coverage First

Before thinking about savings or investment plans, ensure you and your family have adequate medical coverage (medical card). Private hospital treatment costs in Malaysia can reach tens of thousands of ringgit per episode — without protection, it can burden your finances.

2. Follow the 10-15% Income Formula

General financial rules suggest allocating 10% to 15% of your monthly income for protection (takaful/insurance). If your income is RM5,000, this means around RM500-RM750 per month for all protection plans.

3. Start Early, Pay Less

The younger you take up takaful, the lower your contribution rate. A 25-year-old will pay significantly lower contributions compared to a 40-year-old for the same coverage. Don''t delay — time is your greatest advantage.

4. Check Coverage Scope Carefully

Don''t just look at the price — check the coverage scope including:

- Annual and lifetime limits

- Panel hospital list

- Waiting period

- Exclusions

- Additional benefits (riders)

5. Diversify Your Protection

Don''t rely on a single plan. Combine several types of protection:

- Medical card — for hospital costs

- Life takaful — for family dependents in case of death

- Critical illness — for critical diseases (cancer, heart attack, stroke)

- Personal accident takaful — additional protection in case of accidents

6. Maximise Tax Relief

Family takaful contributions qualify for LHDN tax relief of up to RM3,000 per year (under life insurance/family takaful category). For medical & education plans, additional relief of up to RM3,000 is also available. This means you can reduce your income tax while protecting your family.

Malaysia''s Takaful Industry: Key Facts & Figures

Malaysia is one of the largest takaful markets in the world. Here are the key facts:

- Industry assets: RM62.54 billion as of mid-2025 (Bernama)

- Penetration rate: Approximately 19.54% — meaning over 80% of Malaysians are still not fully protected

- Active certificates (family takaful): 6.69 million certificates

- Annual contributions: Exceeding RM9.87 billion

- MTA target: 40% penetration rate by 2028 (The Edge Malaysia)

- Market leader: Takaful Malaysia commands 28% of the family takaful market and 23% of the general takaful market

These figures demonstrate significant growth potential, and also mean that many Malaysians still need to obtain takaful protection.

Frequently Asked Questions (FAQ)

Is takaful only for Muslims?

No. Although takaful is based on Shariah principles, it is open to all Malaysians regardless of religion. Many non-Muslims also choose takaful due to its operational transparency, surplus sharing concept, and ethical investment approach.

What is the difference between takaful contributions and insurance premiums?

Takaful contributions partly constitute a donation (tabarru'') into a common fund, while insurance premiums are full payments to the insurance company in exchange for coverage. In takaful, you still have rights to surplus funds.

Can I claim back my contributions if I never make a claim?

In takaful, if you have a plan with a savings element, you can recover your savings value. For the tabarru'' portion, that money is a donation and cannot be claimed back — however, you are eligible to receive a surplus share if there is a surplus.

What is the minimum takaful coverage I should get?

There is no fixed minimum amount, but financial experts recommend at least life coverage worth 10 times your annual income. If your salary is RM5,000 per month, the recommended minimum coverage is RM600,000.

What are riders in takaful?

Riders are additional benefits that can be added to your main takaful plan. Examples include critical illness coverage, personal accident, hospital & surgical, and contribution waiver in case of disability.

How do I choose the best takaful operator?

Consider these factors: the company''s reputation and financial stability, coverage scope offered, panel hospital list, contribution rates versus benefits, and claims payment track record (claim ratio). Also ensure the operator is licensed by BNM.

Does takaful cover pre-existing conditions?

Generally, most takaful plans do not cover pre-existing conditions initially. However, some operators offer a waiting period after which pre-existing conditions may be covered. It is important to disclose all health information during application.

What happens if a takaful operator goes bankrupt?

Malaysia''s takaful industry is protected by Perbadanan Insurans Deposit Malaysia (PIDM), which guarantees takaful benefits up to certain limits if a takaful operator fails. This provides additional assurance to participants.

Conclusion

Takaful is not merely "Islamic insurance" — it is a financial protection system that is transparent, ethical, and founded on the spirit of mutual assistance. By understanding the differences between takaful and conventional insurance, and knowing the basic strategies for choosing the right plan, you can make wiser decisions to protect yourself and your family.

The first step in planning your finances is ensuring you have adequate protection — and takaful offers an option that aligns with Shariah values and principles.

If you are interested in starting to invest on Bursa Malaysia and building your own portfolio, the first step is having a trading account.

Open your CDS account through our CDS account page to start investing on Bursa Malaysia.

Download our free Stock Market Basics Ebook to understand the fundamentals of stock investing before making financial decisions.

Further Reading

- Hibah dan Faraid: Apa Yang Orang Islam Perlu Tahu Tentang Pewarisan Harta Pusaka

- Urusniaga Tawarruk: Apa Yang Boleh & Tidak Boleh Dalam Kewangan Islam

- Takaful Ambil, Tapi Tak Tahu Ada Takaful di Bursa?

- Kenapa Forex Haram? 5 Sebab Utama & Apa Kata Fatwa Malaysia

- Pengurusan Kewangan Peribadi: Cara Bijak Urus Wang Untuk Masa Depan