Medical Card vs Life Takaful: Which Should You Buy First in Malaysia?

You just started working, earning RM3,500 a month. After paying rent, your PTPTN loan, and daily essentials, you have only RM200-300 left for protection. The takaful agent says "get life takaful first, it secures your family". The clinic doctor says "medical card is more important, hospital bills are expensive these days". Your parents say "just take both at once". But you know - with RM200 left, you can only afford one first. Which one?

This is a question many Malaysians face, and the answer usually depends on your life situation - not a one-size-fits-all answer. Many end up choosing wrong: buying life takaful first while still single with no dependents, or buying expensive medical card while having young children who would starve if they died tomorrow.

This article helps you understand the actual differences, the cost for your age, and a practical framework to choose what is essential first based on your life stage - single, married without children, or with dependents.

Quick Answer

If you are SINGLE without dependents: Buy a medical card first. The risk of hospitalisation is higher than the risk of death. A hospital bill of RM20,000-80,000 can wipe out your savings overnight.

If you are MARRIED with children / have major debts: Buy life takaful first (at least cheap term takaful). If you die tomorrow, your spouse/children will be saddled with debt and lose your income. Then add medical card later.

If your budget is RM200/month: You can afford both with affordable options - term life takaful RM30-50 + basic medical card RM50-100 = total ~RM150 for reasonable basic protection.

What Is a Medical Card and What Does It Cover?

A medical card (also known as Hospital & Surgical insurance/takaful) is a policy that pays your hospital bill when you are hospitalised, undergo surgery, or have certain medical procedures.

What is covered:

- Room & board charges in hospital

- Surgery costs

- ICU / High Dependency Unit

- Medications and treatments during hospitalisation

- Chemotherapy, radiotherapy (cancer)

- Heart surgery, transplants

- Pre and post-hospitalisation outpatient care (limited)

- Cashless admission at panel hospitals

What is NOT covered (typically):

- Routine outpatient treatment (unless special rider added)

- Over-the-counter medications

- Cosmetic surgery

- Maternity (unless special rider)

- Pre-existing conditions not declared

- Workplace accidents (covered by SOCSO)

According to the official industry pricing data reported by Malay Mail, typical Malaysian hospital bills range from RM3,100 to RM33,400 depending on the procedure. Major surgeries like coronary bypass can hit RM80,000+.

What Is Life Takaful and What Does It Cover?

Life takaful (takaful hayat) is a policy that pays a sum assured to your nominee when you die or suffer Total Permanent Disability (TPD).

3 Types of Life Takaful:

1. Term Takaful (cheapest)

- Fixed term (10, 20, 30 years)

- No cash value - if the term expires, the policy ends with no return

- Low premium, high sum assured (e.g. RM50/month for RM500,000 cover)

- Suitable for: time-bound responsibilities (young children, mortgage not yet paid off)

2. Whole Life Takaful

- Lifetime coverage

- Has cash value (cash surrender value)

- More expensive premium

- Suitable for: estate planning, long-term planning

3. Investment-Linked Takaful (ILT)

- Combines protection + investment

- Premium split between protection and investment fund

- Flexible - can change sum assured or premium

- Suitable for: those who want one all-in-one policy

What is covered:

- Death benefit

- TPD (permanent disability from accident/illness)

- Critical illness (additional rider)

- Permanent total disability from accident

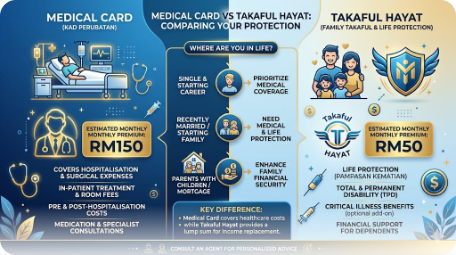

The Real Difference: Medical Card vs Life Takaful

These are two different types of protection serving different purposes. A common misconception: many people think they are similar or interchangeable - they are not.

| Aspect | Medical Card | Life Takaful |

|---|---|---|

| Main purpose | Pay hospital bills | Pay sum assured on death / TPD |

| When to claim | When hospitalised | On death / permanent disability |

| Recipient | Hospital (cashless) or you | Designated nominee |

| Claim frequency | Multiple claims allowed | One-time only (death/TPD) |

| Premium cost | RM40-200/month typical | RM30-150/month (term) or RM200+ (ILT) |

| Risk covered | Illness risk | Death / disability risk |

| Essential at what stage | Essential when low savings & hospital risk | Essential when financial dependents (children, debt) |

Remember: Your risk of hospitalisation this year is far higher than your risk of dying. But if you die, the financial impact on your family is far greater than hospitalisation.

For a complete understanding of takaful basics, read What Is Takaful? Differences vs Conventional Insurance.

Real Costs in Malaysia (Age 25-35)

Medical Card (age 25-35, non-smoker)

| Type | Monthly Premium | Sum Assured / Annual Limit |

|---|---|---|

| Online standalone (Takaful myClick MediCare) | RM40-60 | RM50K-150K |

| Agent-sold standard (Etiqa, Great Eastern, AIA) | RM80-150 | RM100K-300K |

| Premium plan with riders | RM200-400 | RM500K-unlimited |

| Government hospital tiered access | RM30-50 | Government hospitals only |

Source: data from Ringgit Plus medical card comparison.

Life Takaful (age 25-35, non-smoker)

| Type | Monthly Premium | Sum Assured |

|---|---|---|

| 20-year Term Takaful | RM30-60 | RM250K-500K |

| Term Takaful + CI rider | RM60-120 | RM250K death + RM100K critical illness |

| Whole Life Takaful | RM150-300 | RM200K + cash value |

| Investment-Linked Takaful | RM200-500 | RM300K + investment fund |

Factors that increase premium:

- Active smoker: +50% premium

- Female: -10% premium vs male (longer life expectancy)

- Income: high income means you can sustain higher premiums

- Riders: critical illness, hospital cash, disability add RM30-100/month

Framework: Which Comes First Based on Your Life Stage

Life Stage 1: Single, No Dependents, No Major Debt

Pick: Medical Card FIRST

Reason: Your risk of hospitalisation in the next 30 years is far higher than your risk of death. Insurance industry stats show someone aged 25-35 has a 60-70% probability of being hospitalised at least once before age 50. Your risk of dying in the same period is only 5-10%.

Even if you die, no one will starve - you have no children, spouse, or parents fully dependent on you. Your parents may grieve, but they can still support themselves without you.

RM150 budget: Medical card RM100 + save RM50 for emergency fund.

Life Stage 2: Single, No Dependents, But Major Debt (PTPTN, Personal Loan, Mortgage)

Pick: Term Takaful + Medical Card

Reason: Your debt becomes a burden on your family (guarantors) if you die. PTPTN technically is not inherited but mortgage, car loan, credit cards ARE inherited by the estate and can squeeze the family.

Strategy: Get cheap term takaful RM30-50/month to cover your debt (sum assured = total debt). Plus basic medical card RM50-100. Total RM100-150.

Life Stage 3: Married, No Children Yet, Spouse Working

Pick: Medical Card for both, plus small term takaful

Reason: Your spouse can sustain themselves. But medical bills will still be a joint burden. A small term takaful (RM200-300K) covers wedding loans, house deposit, or makes a meaningful saving if one of you dies.

Life Stage 4: Married with Children (THE CRITICAL ONE)

Pick: Term Takaful FIRST with high sum assured (10x annual income), THEN Medical Card

Reason: If you are the family's primary earner and you die, your spouse and children lose their income source. Insurance/life takaful sum assured of 10x annual income is the global standard - if you earn RM60K/year, sum assured should be RM600K (enough to replace income for 10 years).

20-30-year term takaful is the cheapest option. RM50-80/month can secure a sum assured of RM500K for age 30-35 non-smokers.

After that, think about medical card. If your budget allows another RM100-150/month, a medical card protects the family so hospital bills do not destroy savings.

Life Stage 5: Retired / Children Already Independent

Pick: Medical Card is the priority

Reason: Children are independent - no need to replace income. But the risk of illness and hospitalisation at age 50+ rises dramatically. Medical card premiums for older age are indeed expensive (RM300-500/month), but hospital bills for cancer, diabetes, heart disease at this age can hit RM100K-500K.

Term takaful can be allowed to expire if debts are paid off and children are independent.

Practical Scenario: RM200/Month Budget

Let us break it down for Aiman, 28 years old, salary RM4,500, single, with PTPTN debt of RM30,000.

Option A: All-in on expensive medical card

- Medical card premium: RM200/month, sum assured RM500K

- No life takaful

- Risk: if he dies, PTPTN is written off but no savings for family farewell expenses

Option B: Split

- 20-year term takaful: RM50/month, sum assured RM250K (covers PTPTN + extra)

- Online medical card: RM80/month, sum assured RM150K

- Emergency fund: RM70/month into savings

- Total: RM200, complete protection + emergency fund growing

Option C: Investment-Linked Takaful

- ILT: RM200/month, sum assured RM200K + investment fund

- No separate medical card

- Risk: investment is not guaranteed return, and medical coverage is usually basic

Recommendation for Aiman: Option B is the most balanced. Cheap term takaful covers debt + family. Medical card covers hospital risk. Savings build emergency fund.

5 Common Mistakes About Medical Card & Life Takaful

1. "I do not need it because I am healthy"

Wrong. Insurance/takaful is for risks you cannot predict. Today's healthy person can have an accident tomorrow or be diagnosed with cancer next month. Premiums are also far cheaper while you are young and healthy.

2. "Pre-existing conditions will be covered later"

Wrong. Pre-existing conditions (illnesses you already had before buying the policy) are usually not covered or have a 1-2 year waiting period. That is why buying young and healthy matters.

3. "Insurance/takaful as an investment"

Wrong. Insurance and takaful are protection, NOT investment. ILT that combines insurance with investment is usually less efficient than buying term takaful + investing yourself in ETFs/stocks.

4. "Buy the cheapest to save money"

Not always right. Medical cards that are too cheap usually have low limits (RM30K/year covers only minor bills) or many exclusions. Make sure sum assured is enough for cancer/heart surgery costs (minimum RM150K).

5. "Nominee in takaful = direct receipt"

For Muslims, nominees are typically only administrators - the funds revert to the estate and are managed under faraid (unless a hibah amanah is established). To control who receives, you need a valid wasiat and/or hibah. Read Islamic Will (Wasiat): How to Write & Register to understand the mechanism.

Tips for Buying Medical Card / Life Takaful Smartly

1. Compare online before meeting an agent

Online quotations on sites like Ringgit Plus or Policy Street give a realistic picture. Online plans are typically 20-30% cheaper than agent-sold because there are no agent commissions.

2. Buy before age 30

Premiums rise dramatically every decade after 30. A 20-year term takaful at age 25 might be RM40/month, but at 35 it becomes RM80/month for the same sum assured.

3. Choose realistic sum assured

For medical card: minimum RM150K/year. For life takaful: minimum 10x annual income.

4. Add critical illness rider

For an additional RM30-50/month, you get a lump sum payout (RM100-200K) when diagnosed with cancer, stroke, heart attack, etc. This is separate from the death benefit.

5. Review your policy every 3-5 years

Your income will rise. Dependents will change (marriage, children, mortgage). A policy that suited age 25 may not be enough at age 35.

6. Choose a wide hospital panel

Make sure your medical card is accepted at hospitals you usually use - do not find out only when sick that the hospital is not on the panel.

FAQs

What is the difference between takaful medical card and conventional insurance?

Takaful medical card uses tabarru' (donation) structure and wakalah contract - it is shariah-compliant. Conventional medical card uses standard insurance contracts. Coverage and pricing are typically the same. For Muslim investors, takaful is the more suitable choice.

What is the cheapest medical card premium in Malaysia?

Online plans like Takaful myClick MediCare offer premiums as low as RM40/month for ages 25-30. But sum assured is usually low (RM50K-100K). For substantial protection, estimate RM80-150/month for that age.

Do I need a medical card if my employer already provides insurance?

Recommended yes. Company insurance typically covers you while employed - if you resign or are terminated, coverage ends. Plus, company insurance may have limited coverage. A personal medical card is a long-term safety net.

Can I buy life takaful for my children?

Yes, you can. But this is usually not the priority - children have no financial dependents. It is better to buy a medical card for children (covers paediatric hospital bills) than life takaful.

Term takaful expires - what happens to the premiums I have paid?

Nothing. Term takaful has no cash value - if you live to the end of the term, the policy ends with no return. That is why the premium is cheap. Think of it like paying rent for protection - when the term ends, no more protection BUT you were protected throughout that period.

Do I need a medical examination before approval?

Depends on the sum assured and age. For low premiums and young age, self-declaration is usually enough. For high sum assured (>RM500K) or age >40, a full medical examination may be required.

Can I claim medical card and life takaful at the same time?

For different benefits - yes. Medical card for hospital bills, life takaful for death/TPD. But you cannot "double claim" for the same event. If for the same hospital admission, only one policy is relevant.

What if I cannot afford both?

Choose one based on your life stage (see framework above). Single → medical card. Have children → term takaful. Meanwhile, save 3-6 months of expenses as an emergency fund as self-insurance for minor issues.

Conclusion

Medical card and life takaful are not "either/or" choices - both are important but protect different risks. Medical card for illness risk (frequent, moderate-to-high cost). Life takaful for death risk (rare, big financial impact on family). The priority depends on your life stage and who would be financially affected if something happened to you.

Most importantly: do not delay. Premiums rise every year, and pre-existing conditions can void claims. Buy something you can afford now, then upgrade when income rises.

While you build personal protection, remember that building wealth is also long-term protection. Consistent stock investment can be an additional safety net for retirement and family dependents.

Open a CDS trading account today to start investing in Bursa Malaysia as well as overseas markets including US and Hong Kong stocks through one platform.

Download our free stock market basics ebook to understand investment fundamentals before taking the next step.