PIDM Malaysia: Is Your Money in the Bank Actually Safe? RM250,000 Limit Explained

When you open a savings account at Maybank, CIMB, or any Malaysian bank, there is a guarantee most people never notice: your money is protected up to RM250,000 by a statutory body called PIDM. Yet ask your friend "what is PIDM?" and most will say "never heard of it" or mistakenly assume it is part of Bank Negara Malaysia.

This is a problem. Without understanding PIDM, you may be putting money in places you think are safe - when they are not protected at all. Crypto on Luno. Unit trusts at Public Mutual. Shares in your CDS account. Even gold held at a bank - none of these are covered by PIDM.

This article explains what PIDM is, what is actually covered and what is not, how the compensation scheme works if your bank fails, and the common misconceptions people have about this protection.

Quick Answer

PIDM (Perbadanan Insurans Deposit Malaysia / Malaysia Deposit Insurance Corporation) is a statutory body that protects deposits at member banks up to RM250,000 per depositor per member bank. It also covers insurance policies and takaful certificates in Malaysia through its TIPS system. This protection is automatic and free - no registration required. But it does NOT cover unit trusts, stocks, gold, or cryptocurrency even if those products are sold through a bank.

What Is PIDM?

Perbadanan Insurans Deposit Malaysia (PIDM) is a statutory body established in 2005 under the PIDM Act. It is a separate entity from Bank Negara Malaysia (BNM), though the two work closely together.

PIDM operates two main protection systems:

- Deposit Insurance System (DIS) - protects deposits at member banks

- Takaful and Insurance Benefits Protection System (TIPS) - protects insurance and takaful policies

PIDM's funding comes from premiums paid by member banks and insurance/takaful member companies - not from taxpayer money. This is an important fact. The public pays nothing for this protection - the cost is fully borne by the industry.

PIDM's objective is not just to pay out when a bank fails. It also plays a role in maintaining confidence in the financial system - if people know their money is safe, they will not trigger bank runs on rumours, and the financial system remains stable.

RM250,000 Coverage: What It Actually Means

The protection limit is RM250,000 per depositor per member bank. According to PIDM's official FAQ, this limit fully protects 97% of depositors in Malaysia.

Understanding "per depositor per bank" is crucial:

Example 1: RM400,000 all in one bank

- Savings RM200,000 + FD RM200,000 = RM400,000 total at Maybank

- Protected: RM250,000 only

- Not protected: RM150,000

Example 2: RM400,000 split across two banks

- RM200,000 at Maybank + RM200,000 at CIMB

- Protected: RM200,000 at each bank (under the RM250K limit)

- Total protected: RM400,000 fully

Example 3: Joint account

- RM400,000 in a joint account at one bank

- Each depositor is protected separately up to RM250,000

- Total protected: RM500,000

Is it smart to split money across many banks to maximise protection? Technically yes, but in reality if a bank in Malaysia fails, the systemic impact usually involves multiple banks - so this strategy is not entirely risk-free.

Separate Protection: Conventional vs Islamic Deposits

This is something many people do not know. PIDM provides a separate RM250,000 limit for conventional and Islamic deposits at the same bank.

So if you hold:

- Maybank (conventional): RM200,000 → fully protected

- Maybank Islamic (shariah): RM200,000 → fully protected separately

- Total protected at Maybank group: RM400,000

This is a good strategy for people with large savings - use both conventional and Islamic accounts at the same bank. PIDM FAQ explains this in detail.

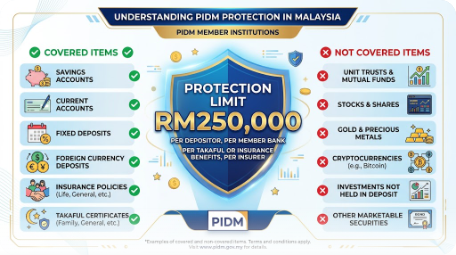

What Types of Accounts Are Covered?

PIDM covers various types of deposits at member banks:

Covered:

- Savings accounts

- Current accounts

- Fixed deposits (FD)

- Foreign currency deposits (USD, SGD, EUR - converted to MYR at prevailing rate upon bank failure)

- Islamic accounts (savings-i, current-i, FD-i) - separate RM250K limit

- Cashier's orders and bank drafts

NOT Covered (this is critical for investors):

- Unit trusts - even if sold through a bank counter

- Stocks / shares - including those in CDS accounts

- Gold investment - for example Gold Investment Account (GIA), Gold Saving Account at Maybank/CIMB

- Cryptocurrency - all platforms including Luno, Tokenize, MX Global

- Bonds - including MGS retail bonds

- Investment-linked insurance products (the unit/investment portion)

- Derivatives - warrants, options, futures

- Safe deposit box contents - the bank only holds them, does not own them

This is the most common misconception. Many people assume "money in the bank = safe". Not quite - it depends on the ACCOUNT TYPE. Gold at Public Gold? Not covered. Maybank GIA? Not covered. Public Mutual unit trusts even at a bank counter? Not covered.

Which Banks Are PIDM Members?

All licensed commercial banks in Malaysia are mandatory members of PIDM under the PIDM Act 2011. This includes:

Local banks:

- Maybank, CIMB, Public Bank, RHB, Hong Leong Bank, AmBank, Alliance Bank, Affin Bank, Bank Islam, Bank Muamalat, Bank Rakyat

Foreign banks (locally incorporated subsidiaries):

- HSBC Malaysia, Standard Chartered Malaysia, OCBC Bank, UOB Malaysia, Citibank Malaysia, Bank of China Malaysia, Deutsche Bank Malaysia

Dedicated Islamic banks:

- Bank Islam, Bank Muamalat, Hong Leong Islamic Bank, Maybank Islamic, CIMB Islamic, etc.

New digital banks (since 2024-2025):

- GX Bank (Grab), AEON Bank, Ryt Bank (KAF), Boost Bank (AmBank-Boost), YTL-Sea Bank

Every member bank must display the PIDM logo at the counter and on its website. If you see the PIDM logo - you are protected.

What Happens If a Bank Fails?

This is a scenario most people never think about - but it has happened in other countries (e.g. Silicon Valley Bank in the US, 2023). In Malaysia, no major failure has occurred during the PIDM era (2005-2026), but the process is already prepared.

A simplified process if a member bank fails:

Day 1-3: BNM announces the bank is closed. Depositors' accounts are temporarily frozen.

Week 1-2: PIDM takes over. Depositors are contacted or given access to an official portal to make claims.

Week 2-4: Compensation is paid up to RM250,000 per depositor per bank. Typically automatic - no lawyer needed.

Amounts above RM250,000: Depositors must claim through the liquidator - there is no guarantee of 100% recovery. Typically you get partial (50-80%) depending on the bank's remaining sellable assets.

This timeline is based on international standards - PIDM itself is stress-tested regularly to ensure it has enough funds. PIDM publishes annual reports showing its funding remains sufficient for protection.

TIPS: Insurance & Takaful Protection

In addition to DIS for deposits, PIDM also operates TIPS (Takaful and Insurance Benefits Protection System) which protects life insurance, general insurance, family takaful, and general takaful policies.

According to the official TIPS FAQ:

Protected under TIPS:

- Life insurance policies (death, disability, medical)

- Family takaful (death, TPD, critical illness)

- General insurance (motor, home, fire, liability)

- General takaful

- All policies issued in Malaysia and denominated in MYR

- Automatic protection - no application required

NOT Covered:

- Policies issued outside Malaysia

- Non-MYR policies (e.g. USD policies)

- Unit portion of investment-linked insurance (maturity & surrender benefits) - BUT death benefits from the unit portion ARE covered

Key differences between DIS (deposits) and TIPS (insurance):

- DIS: RM250,000 limit per depositor per bank

- TIPS: more complex limits based on benefit type. For life insurance, general limits are RM500,000 per policy for death benefits and RM500,000 for living benefits.

5 Common Misconceptions About PIDM

1. "My money in the bank = 100% safe"

Not true. Only up to RM250,000 per depositor per bank. The excess depends on the bank's asset liquidation.

2. "Crypto on Luno is PIDM-protected because Luno is SC-registered"

Not true. PIDM protects member banks only - Luno is a Digital Asset Exchange (DAX) registered with SC, not a bank. If Luno fails, your crypto is not PIDM-protected.

3. "Gold I bought through Maybank's Gold Investment Account (GIA) is protected"

Not true. GIA is an investment product, not a deposit. If the bank fails, GIA holders must claim as creditors.

4. "My unit trusts at Public Mutual through a bank counter are protected"

Not true. Unit trusts are investment products - not under PIDM. They fall under a separate scheme (Securities Commission with the Capital Market Compensation Fund for specific situations).

5. "My PIDM protection is reduced because I'm the one paying the premium"

Not true. PIDM protection is free for depositors and policy holders. Premiums are paid by banks/insurers, not you.

Practical Strategies for Large Savings

If you have savings above RM250,000, here are strategies to maximise your protection:

1. Split across different member banks

RM500,000? Put RM250K at Maybank, RM250K at CIMB. Both fully protected.

2. Use conventional + Islamic combination at the same bank

RM500,000? Put RM250K at CIMB (conventional) + RM250K at CIMB Islamic. Separate limits, both fully protected.

3. Strategic use of joint accounts

Joint accounts with a spouse count as separate depositors - each depositor gets the RM250,000 limit.

4. Diversify beyond banks

Part of your savings can go into investments (not PIDM-protected) such as EPF (with dividends & low risk), ASB, or a diversified stock/ETF portfolio. But remember - investments are NOT savings; they carry risk.

5. Check the member bank list

Make sure the bank you use is indeed a PIDM member. Check on the PIDM website.

PIDM vs Similar Schemes in Other Countries

Malaysia is not alone in having a deposit insurance scheme - most developed countries have their own versions. A quick comparison:

| Country | Scheme | Limit |

|---|---|---|

| Malaysia | PIDM | RM250,000 |

| Singapore | SDIC | SGD100,000 (~RM350,000) |

| United States | FDIC | USD250,000 (~RM1.2 million) |

| United Kingdom | FSCS | GBP85,000 (~RM500,000) |

| Indonesia | LPS | IDR2 billion (~RM570,000) |

Malaysia's PIDM limit is moderate by global standards. For ultra-high-net-worth depositors, the bank-splitting strategy is a must.

FAQs

What is PIDM and who is protected?

PIDM is Perbadanan Insurans Deposit Malaysia, a statutory body that protects deposits at member banks up to RM250,000 per depositor per bank, as well as insurance and takaful policies in Malaysia. All depositors and policyholders at PIDM member institutions are automatically protected - no registration required.

Do I need to pay anything for PIDM protection?

No. PIDM protection is free for you. Premiums are paid by member banks/insurance companies. You will never be charged for this protection.

What if I have more than RM250,000 at one bank?

Amounts above RM250,000 are not protected by PIDM. If the bank fails, you must claim the excess through the bank's liquidation process - the outcome is not guaranteed. It is recommended to split across banks or use a combination of conventional and Islamic accounts.

Are foreign currency deposits protected?

Yes. USD, SGD, EUR deposits at member banks are protected. If the bank fails, your deposits will be converted to MYR at the prevailing exchange rate, then aggregated with other deposits for the RM250,000 limit calculation.

Are my unit trusts at Public Mutual PIDM-protected?

No. Unit trusts are investment products, not deposits. They are not covered by PIDM. Unit trusts are regulated by the Securities Commission (SC) under different rules.

Are shares in my Bursa CDS account protected?

No. Shares are protected by a different mechanism - Bursa Malaysia Depository (BMD) as central depository, and the Capital Market Compensation Fund for certain situations (such as broker fraud). PIDM is strictly for bank deposits.

Is my crypto on Luno protected?

No. Crypto is not protected by PIDM even if the platform (Luno, Tokenize, MX Global) is registered with SC as a Digital Asset Exchange. Crypto holders are investors, not depositors.

How long do I have to wait for compensation if a bank fails?

Based on PIDM standards, compensation is paid within 2-4 weeks after PIDM takes over the bank. This process is automatic for most depositors - no lawyer or complicated application required.

Conclusion

PIDM is an important safety net for Malaysians, but it is not a blanket protection for all types of financial products. The RM250,000 limit per bank is enough for 97% of depositors, and the automatic + free protection is a benefit many countries also offer. The key to maximising protection: understand which products are covered (deposits, insurance, takaful) and which are not (unit trusts, stocks, gold, crypto).

For large depositors, diversification strategies across member banks or conventional-Islamic combinations are essential. For investors, PIDM is a reminder that savings and investments are different categories - each has its own protection scheme and risk profile.

Now that you understand what is covered and what is not, you can plan your financial portfolio with more confidence - savings for your emergency fund (PIDM-protected) + investments for long-term growth (regulated by different authorities but with higher potential returns).

Open a CDS trading account today to start investing in Bursa Malaysia as well as overseas markets including US and Hong Kong stocks through one platform.

Download our free stock market basics ebook to understand investment fundamentals before taking the next step.